Independent mortgage banks (IMBs) have been around for more than a century. but have taken on increased significance and power in the marketplace since the housing crisis. The Mortgage Bankers Association (MBA) says that several myths have grown up around this trend, coming from critics such as the Brookings Institution. It just published a White Paper discussing the current role of IMBs and addressing the myths.

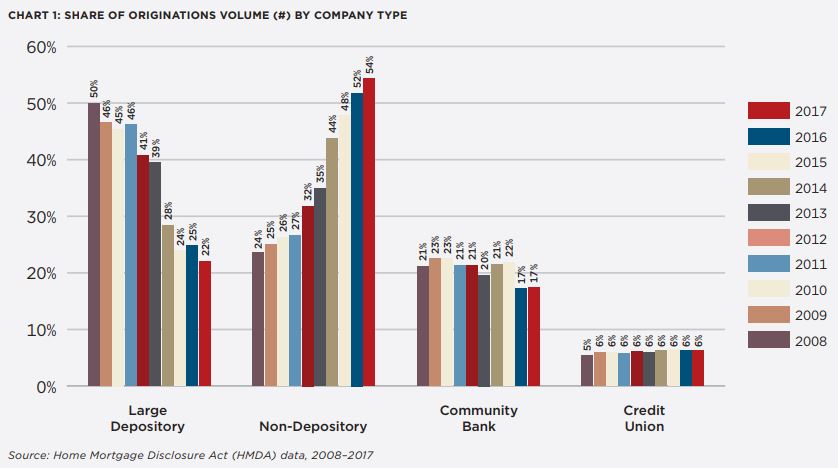

There were 900 IMBs in the US In 2017 according to Home Mortgage Disclosure Act (HMDA) data. They account for 16 percent of companies reporting data but originated 54 percent of single family (one to four unit) mortgages, up from 25 percent in 2008. MBA says this growth presents policy questions, but "it should be evaluated based on a solid understanding of the IMB role and importance to the housing finance system."

IMBs are non-depository institutions, typically monoline companies that focus on origination, servicing, and related services. Most are closely held private companies, but a few have grown large enough to attract backing from private equity firms, obtain larger commercial financing or go public.

IMB's typically fund mortgages with a combination of their own cash, usually 2 to 5 percent of the loan amount, and warehouse lines to fund individual mortgages. Warehouse lines are short term credit facilities secured by the funded loans until they are sold to an investor, typically in one to three weeks. The vast majority of IMB loans are sold to aggregators or directly to Fannie May or Freddie Mac (the GSEs) or are issued as securities guaranteed by Ginnie Mae. Aggregators include banks and other financial institutions that either hold the loans in portfolio or sell into the agency market. Some IMBs sell into private label securities (PLS) but that market is small since the crisis, accounting for less than 5% of the 1.6 trillion in home mortgages originated in 2018.

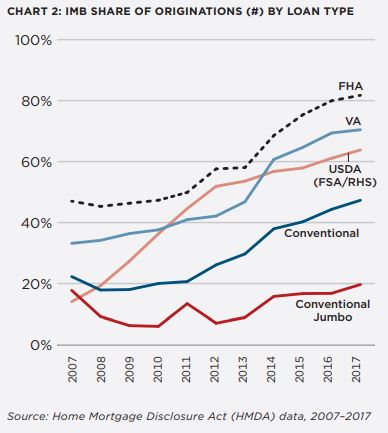

IMBs' share of home mortgage lending has ebbed and flowed with broader developments in the market. Historically they have focused on FHA and VA mortgage lending and have gained share when depositary lenders pulled back from the government mortgage sector. Since 2008 they have gained significant market share in every loan category, government, conventional, and even jumbo. In 2017 they accounted for more than 80% of FHA loans 70% of VA loans and 64% of RHA loans.

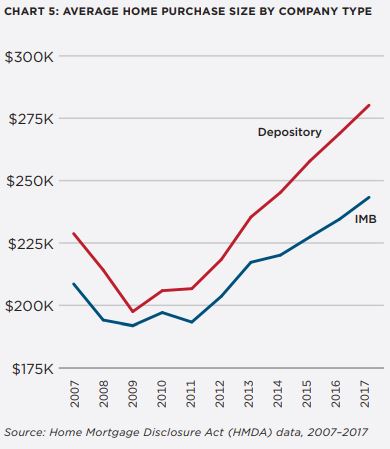

Given its focus, it's not surprising that more than 64 percent of minority and 59 percent of low- and moderate-income homebuyers obtained their financing from IMB in 2017. They also tend to serve borrowers needing smaller loans. The average loan balance for IMB home purchase originations in 2017 was $243,000 compared to $280,000 for federally insured depositories.

MBA says this expanded IMB presence has strengthened housing finance by bringing local market knowledge, diversifying risk across a larger number of lenders and servicers and fostering greater competition and innovation. This is particularly true in the government lending market. In 2011 the 5 largest Ginnie Mae issuers accounted for more than 3/4 of single family Ginnie Mae issuance and the top 2 lenders alone had 60 percent; today the top 5 lenders account for only 42 percent, meaning less concentration of risk, more diverse business models, and more innovation.

While the IMB role has grown significantly over the past decade so has the regulatory framework under which they operate. Prior to the crisis IMBs were licensed in some states registered in others, exempt from licensing in still others. Consumer protection was fragmented. Today they must comply with all of the same federal mortgage consumer protection rules as depositories and compliance is supervised by the Consumer Financial Protection Bureau. They are also now subject to licensing and supervision through the Conference of State Banking Supervisors (CSBS)

In addition to regulatory supervision by the states and the CFPB they receive significant counterparty oversight by FHA and the GSEs, with each establishing minimum net worth and liquidity requirements for lenders and servicers. These standards were increased substantially in 2015. Warehouse lenders also closely monitor IMBs for counterparty risk Finally, IMBs are the only mortgage lending business model where individual loan originators are licensed and subject to continued education requirements in each state which they operate.

MBA says any shift in market share generates policy concerns, especially in financial services. However, concerns over the IMBs expressed by academics, think tanks, and regulators over the past appear overblown.

Myth 1: The IMB share growth is new and unprecedented. As previously noted, IMBs' business model has been around for 140 years and their market share has shifted in response to other market developments, the share of government lending and the appetite of banks for mortgage risk. When banks step back from mortgage origination and servicing, it is monoline iambs that stand ready to fill the gap.

For example, their market share rose from 35 percent in 1990 to 56 percent as the depositary share fell from 65 percent to 44 percent. What is different from 1995 is today's higher environment of regulation and counterparty supervision.

Myth 2. Unregulated IMBs are part of the risky shadow financial system of non-banks taking market share from regulated institutions. As detailed above, IMBs are subject to the same regulations and oversight from state and federal agencies as other mortgage lenders and significant counterparty oversight. In addition, depositories continue to have some noteworthy advantages over IMB's such as federally insured deposits, access to the Federal Reserve discount window, access to Federal Home Loan Bank (FHLBank) advances and preemption of many state laws. In fact, much of the market share shift was ceded by banks which fell back due to a combination of factors such as heightened regulatory risk or overzealous consumer protection enforcement, excess reputational risk, uncertainty about the False Claims Act and GSE buyback demands, punitively high capital standards, and better opportunities from other business lines.

Policy reactions that seek to constrain IMB market share don't guarantee that banks will come back or serve the same market segments as IMBs. Further, MBA says, some concerns would be more rightly addressed to non-mortgage activity by hedge funds and other investment vehicles.

Myth 3: IMBs originate high-risk mortgages that threaten a return to pre-crisis lending. Because they focus on government programs, IMBs originate loans that on average have lower credit scores or higher loan-to-value or debt-to-income ratios than other lenders. Government programs are designed to serve populations that are foundational to middle-class home ownership and wealth building and the lender agencies control the credit box. There is little evidence of a return to the excessively layered pre-crisis risks.

Further, IMBs are subject to the same limits and restrictions on high risk mortgage products as depositary institutions and even greater restrictions in some states. The CFPB's ability to repay rule and qualified mortgage (QM) requirements apply as do anti-steering and fair lending/servicing requirements

Myth 4f: IMBs pose taxpayer and systemic risk to the economy and financial systems. IMBs do not pose taxpayer risk in the same manner as banks. They accept deposits subject to Federal Deposit Insurance Corporation (FDIC) insurance. In the event of a bank failure, FDIC pays back depositors, and should its fund run dry turns to the US Treasury for funds. IMBs on the other hand don't accept federally insured deposits and have no Treasury backing. In a failure their owners can lose their entire investment. Some counterparties, including governmental entities like Ginnie Mae face risk, but only in extreme cases of fraud or a severe economic crisis and only after layers of private capital are exhausted.

Systemic risk occurs when the failure of one institution cascades across the financial system. Even though banks provide warehouse financing to IMBs, it is unlikely that the failure of a warehouse customer could lead to such a widespread crisis. Even at the depth of the Great Recession well run warehouse bankers stayed in the market and provided sufficient liquidity. Again, there are far greater protections today.

The Financial Stability Oversight Council (FSOC) has not identified the IMB sector as a systemic risk even though they first noted their rising lending and servicing shares in their 2014 annual report. They recommended that state regulators work together with the CFPB & Federal Housing Finance Agency (FHFA) to ensure adequate oversight and have continued to monitor the sector. In 2018 FSOC highlighted that mortgage credit standards as measured by average credit scores and loan performance measured by 90-day plus delinquencies remain strong even in the face of three major hurricanes in 2017.

The size of IMBs also mitigates system risk. As noted, most are small and privately held. The largest, Quicken Loans originated an estimated $86 billion in mortgages in 2017 with a market share of less than 5 percent. The next five largest IMBs together account for an 8 percent share. In 2006 the three largest mortgage lenders, all banks, accounted for more than $950 Billion in mortgages and a 35 percent share. Similar trends exist for mortgage servicing; significant growth in the IMB share but much lower levels of market concentration than before the crisis when not only was servicing highly concentrated but included high volumes of very risky mortgage products. MBA says while IMBs' market share should be and is closely monitored, it does not present any systemic or taxpayer risk.

The systemic risk arguments from the Brookings study rest primarily on concerns about warehouse lending and their need for liquidity in a downturn to sustain serving advances as delinquencies rise. MBA says these are important issues and during the financial crisis warehouse lending contracted substantially, hurting some IMBs. In a future liquidity crisis, IMBs could again be casualties but are unlikely to be the cause.

MBA says there are some common-sense policy solutions that could add security and stability to the IMB sector at little cost to the taxpayer. Additional policy steps should also focus on making the origination and servicing of mortgages an attractive and stable market for any lender, bank or non-bank that wants to invest in supporting homeownership

- Ensure that QM, Ginnie Mae and GSE lending standards remain focused on creditworthy borrowers and safe products.

- Grant IMBs eligibility for the FHLBank system. Access to their advances collateralized by mortgage servicing rights (MRS) or servicing advances will strengthen IMBs' liquidity positions while maintaining the FHLBank mission of supporting institutions that are committed to housing finance.

- Provide FHA VA USDA and Ginnie Mae with the funding and resources needed to conduct thorough counterparty oversight as well as to identify and respond to emerging risks.

- Ensure the mortgage servicing compensation regimes of the GSEs and Ginnie Mae preserve and support a deep and liquid market for mortgage servicing rights for servicers of all sizes and business models.

- Improve the value and liquidity of Ginnie Mae MSRs by exploring options from Ginnie Mae's 2020 white paper.

- Standardize servicing requirements of the government guarantors and clarify the nature of the liability that participation in their program entails.

- Make the mortgage market more attractive to banking institutions by reducing the punitive treatment of MSRs under U.S. bank capital rules and fix FHA False Claims Act enforcement that has driven many banks from the FHA program.

MBA concludes that market share shifts are not uncommon and are driven by a number of complex factors. Regulatory arbitrage is not a primary driver here as the post crisis regulatory regime for IMBs has been robust and began in the states even before 2008. As policymakers assess the state of the housing finance system, they should avoid steps designed to force market share away from IMBs and focus instead on measures that will make origination and servicing attractive and stable markets for any bank or non-bank lender that wants to invest in supporting stable homeownership.