Freddie Mac and Fannie Mae have long advocated for homebuyer education but as Freddie Mac points out in this month's edition of Insight and Outlook, it has been surprisingly difficult to determine how much it actually helps potential homebuyers. "There is widespread agreement in the industry that homebuyer counseling can help prevent some of the mistakes made during the housing boom. However, early studies of the impact of counseling produced sometimes conflicting or inconclusive results and raised questions about the effectiveness of borrower education and counseling."

Most studies have been observational. One, for example reviewed data on 40,000 participants in Freddie Mac's Affordable Gold Loans Program and concluded that borrowers who received classroom and home study counseling had reductions in their subsequent rates of serious delinquency of 26 percent and 21 percent respectively. Borrowers who received individual counseling averaged a 34 percent reduction.

But such observational studies can't make clear that such reductions are the result of the education received. The Insights article says that "Perhaps the borrowers who received counseling also were more high-educated than the borrowers in the other group. Maybe they had a greater disposition or ability to apply the information provided by the education course. Maybe they had higher credit scores than the other borrowers."

The advantages of studying the impact of homeowner education through an experimental study, one in which participants are divided into a treatment group and a control group, are obvious but such studies are expensive and in some cases participants differ from the general population by the simple fact they are willing to participate. There is also the ethics issue of offering a benefit to one group but not to another and finally a measurement issue; how does one define the expected benefit of homeownership counseling? Do we expect that those who receive counseling will be more likely to purchase a home or to take on debt or that they will rent longer to build up a larger downpayment. Do we expect that their credit scores will rise?

In 2014 the Federal Reserve Bank of Philadelphia reported on a five year controlled study on pre-purchase education. The study included only first-time homebuyers who had not previously have applied for a mortgage, received prior counseling, or were under contract to purchase a home or in a program that required counseling. Both the treatment and control groups received a two-hour pre-purchase workshop and a workbook that included information on preparing for homeownership, shopping for a home and a mortgage, applying for a mortgage, and closing and settlement. No further services were provided to the control group.

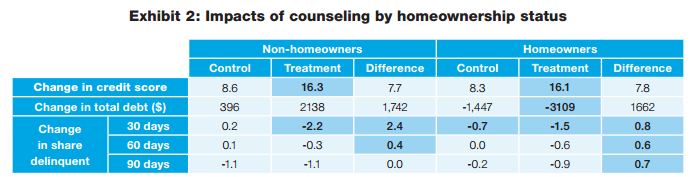

The treatment group was given one-on-one counseling on budgeting, guidance on homebuying and the availability of other services from the counseling agency. Twenty-nine percent of participants opted to use some of the extra services.

The credit scores of the control group rose by 8.5 points following the workshop while the treatment group raised their scores an average of 16.2 points after completing all of the training. Over the course of the five year experiment some participants in each group bought houses so the groups were further divided into homeowners and non-homeowners. The treatment group, whether homebuyers or not, continued to have credit score increases about twice that of the two control group cohorts.

Freddie Mac says the increase in non-mortgage debt among the groups was especially intriguing. Non-homeowners increased their total debt over the five years but the treatment group increased more than the control group. Homeowners decreased their total debt with the treatment group decreased the most. Freddie Mac said perhaps non-homeowners felt more able to take on debt without the burden of a mortgage or homeowners may have reduced their non-mortgage debt to prepare for applying and taking on a mortgage.

There also appeared to be an effect on credit performance. The treatment group, whether homeowners or not, showed greater changes in the share of delinquencies of all durations than did the control group.

Freddie Mac concluded that the Federal Reserve's study supports its belief in pre-purchase homeownership counseling but weighed in in favor of the benefit of the two hour workshop. It appears to have provided all participants with a statistically significant increase in credit scores. Both the workshop and the individual counseling reduced future delinquencies, especially among homeowners.