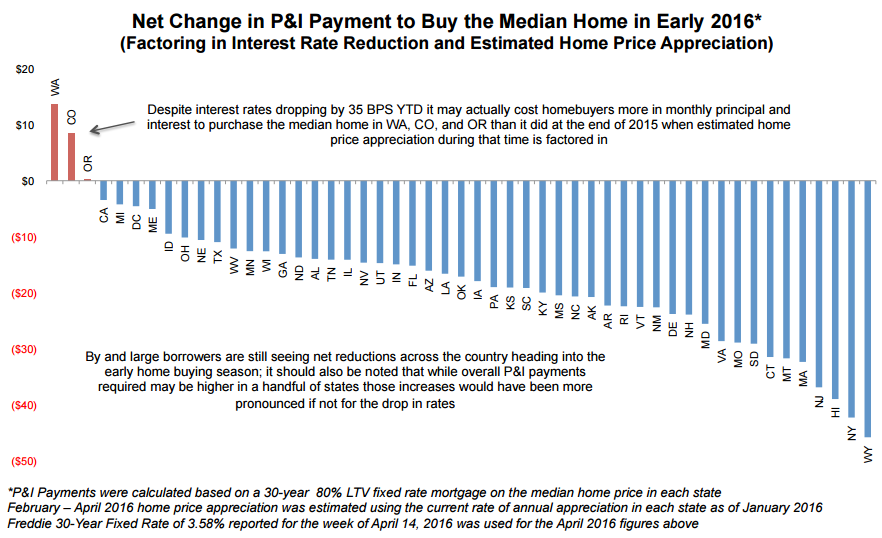

Any benefits to affordability delivered by recent improvements in interest rates have been significantly downgraded or even erased by home price increases. Black Knight Financial Services said in its March Mortgage Monitor that the interest rate declines the country enjoyed during the first months of 2016 could have saved a homebuyer $44 per month on a mortgage used to purchase a median priced home. However, home price appreciation cut that back to just $18 per month.

At the time the Monitor's data was compiled, in March 2016, mortgages interest rates had fallen year-to-date by about 35 basis points. Black Knight used those lower rates to calculate principal and interest payments to determine how lower rates impacted affordability of an 80 percent loan-to-value (LTV) 30-year fixed rate mortgage. All things being equal those declines would have saved borrowers "significant" money on a home purchase, but rising home prices are muting the effect. In some parts of the country home price gains could soon wipe out all the benefits from falling rates.

Black Knight Data & Analytics Senior Vice President Ben Graboske said Black Knight's Home Price Index for February showed an annual home price appreciation of 5.3 percent which would reduce that $44 median savings appreciably. "The mortgage on a median-priced home is still more affordable than it was in December despite rising prices," Graboske said, "just not as much as one might expect given that rates are as low as they are. This isn't to say that interest rate reductions aren't beneficial to buyers - they almost certainly are. If rates hadn't dropped over the past four months, it would cost an additional $28 to buy the median-priced home today as compared to December 2015.

"By and large, borrowers are still seeing net reductions in monthly payments across the country heading into the early home buying season. In some areas though, prices are appreciating so quickly that they may have fully offset any savings from rate declines. Assuming the HPA observed in February continues through March and April, it may actually cost home buyers more in monthly principal and interest to purchase the median-priced home in Washington, Colorado and Oregon than it did at the end of 2015, even with a 35 BPS drop in interest rates."

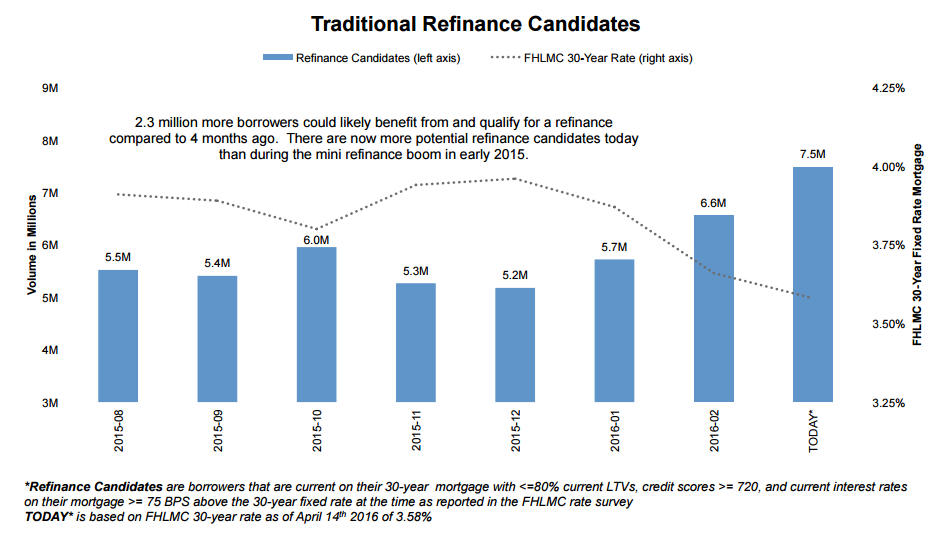

The company noted that the falling rates have also increased the population of homeowners who could qualify for as well as benefit from refinancing their 30-year mortgages by about 2.3 million in the two months since it last did this analysis. This would bring the pool of refinancable homeowners to 7.5 million borrowers, the largest since 2013.

Approximately 40 percent of these potential candidates took out their current mortgages from 2009 through 2011, during the downturn of the market and may not have been aware they had sufficient equity to refinance. Roughly one million have crossed the 20 percent equity threshold over the past 12 months and now have the 80 percent LTV necessary to qualify for a refinance, however Black Knight says that over two-thirds of the total population met eligibility requirements in early 2015 as well, but did not take advantage of refinancing at that time.

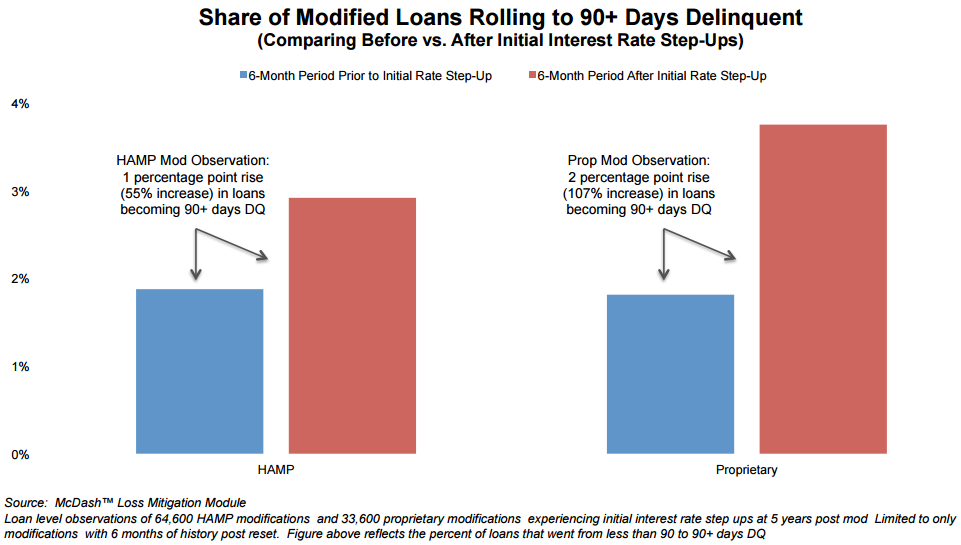

In addition to reprising the delinquency data the company released earlier in its "first look" report, Black Knight also focused part of the Monitor on the status and recent performance of loans that were modified both by individual lenders and through the Home Affordable Modification Program (HAMP) run jointly by the Treasury Department and the Federal Housing Finance Agency.

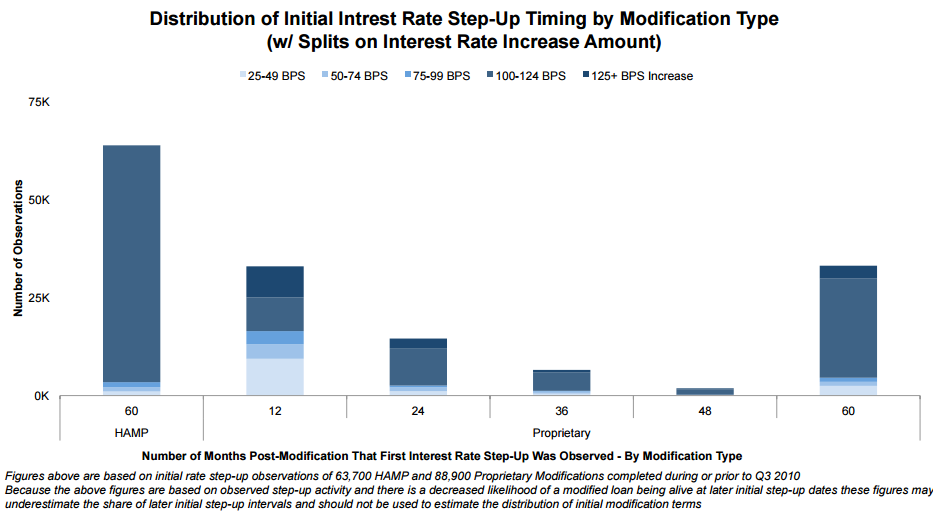

According to Treasury 96 percent of the HAMP modifications included a rate reduction and 80 percent are scheduled for a rate step-up after five years and some will have subsequent resets as well. There were many variations to proprietary modifications and Black Knight looked only at those with interest step-ups at five years.

Looking at a sample of 64,600 HAMP and 33,600 proprietary modifications, all of which had received an initial rate and for which six-months of post reset performance data was available the company found that there was an increase in defaults post change but so far the impact has been "relatively minimal." Only about 1 percent of borrowers that have gone through the HAMP resets appear to have defaulted because of an increase in their mortgage payments. To put this in context, of the estimated 290,000 borrowers that faced those increases through the fourth quarter of 2015, only 2,900 would have become 90+ days delinquent as a result.

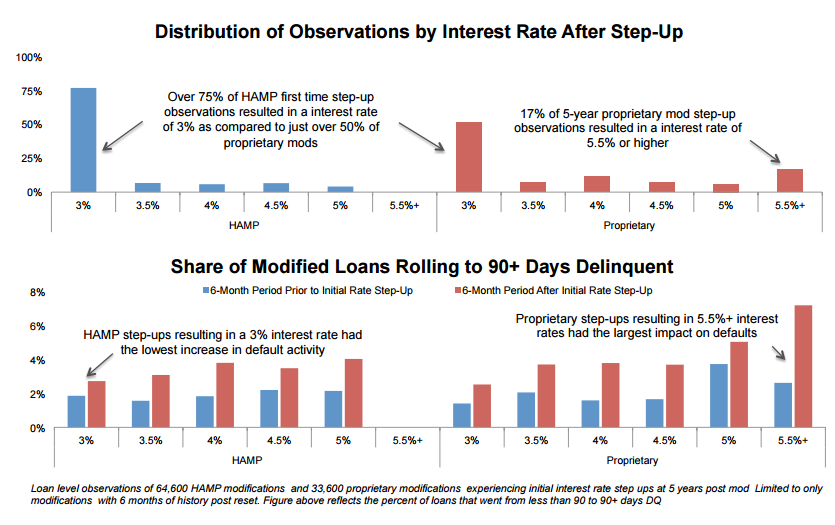

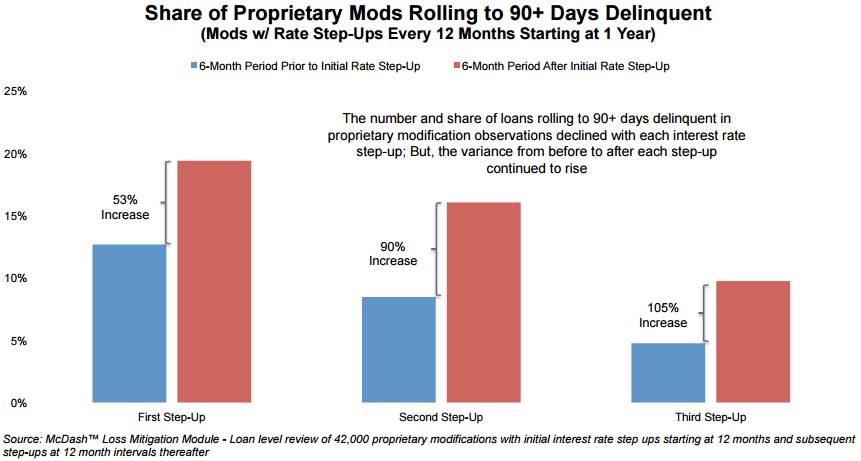

The most pronounced impact of proprietary step-ups on delinquencies appears to be due in part to higher resulting rates. Those step-ups that resulted in 3 percent rates had the lowest impact on the performance under both HAMP and proprietary modifications with the lowest among HAMP mods going from 2 percent to 3 percent, a 0.9 percent increase in delinquencies and a 46 percent increase in the roll rate to 90+ days delinquent.

Proprietary modifications that rose to 5.5 percent or higher saw delinquencies increase by 4.6 percentage points and the roll rate go up 174 percent. On the HAMP side, another 1 percentage point increase in interest rate - to 4 percent, doubled the impact on delinquencies.

While HAMP modifications had a uniform 60-month timetable before the initial adjustment there were a wide variety of arrangements within the proprietary universe. Black Knight said those loans with early resets were a likely contributor to the high early recidivism rates in those modifications. Additionally, many early resets resulted in a significant rate increase; 24 percent saw rates increase by 125 basis points or more only one year after they were modified.

Black Knight concludes that the further a borrower goes into a modification the more likely he is to perform both before and after a rate reset. However, the greater the increase in the rate the higher the percentage of loans rolling into delinquency.

If HAMP follows the proprietary pattern the number of defaults will likely be lower with each scheduled step up although the percentage difference will likely be greater. There will probably be fewer modified loans in existence at the second step-up as well.