The Departments of Housing and Urban Development and Treasury issued their joint Housing Scorecard for May on Thursday. The big news is that the Administration is finally moving to penalize servicers who have consistently failed to meet the goals of the Making Home Affordable Program, which is designed to help homeowners who have fallen behind on their loan payments.

The Scorecard contains results of new Servicers' Assessments, which summarize performance for the 10 largest loan servicers. The assessments rely on information from reviews conducted during the first quarter of 2010 on three categories of program implementation: identifying and contacting homeowners, homeowner evaluation and assistance, and program reporting, management, and governance.

While all ten servicers are in need of improvements, four were identified as needing "substantial improvements"; Bank of America, J.P. Morgan Chase Bank, Ocwen Loan Servicing, LLC; and Wells Fargo Bank. Program administrators found that there were extenuating circumstances leading to the negative results in the assessment of Ocwen Loan Servicing (they acquired another servicing portfolio during the testing period), however Bank of America, J.P. Morgan Chase and Wells Fargo will have financial incentives withheld for this quarter and payments will continue to be withheld until specified improvements are made.

To be clear, new fines are not being imposed. Incentive payments are simply being withheld. Servicers receive payments from Treasury for every successful permanent modification they complete under the Home Affordable Modification Program as well for each short sale/deed-in-lieu they complete (pursuant to the Home Affordable Foreclosure Alternative Program). The three companies were reported to have received $24 million in incentive payments last month. New incentive payments will be withheld. In certain cases though, particularly where there is a failure to correct identified problems within a reasonable time, Treasury may also permanently reduce the financial incentives paid out to servicers.

Six servicers were identified as needing moderate improvement and no financial penalties were assessed. Those servicers are: American Home Mortgage Servicing, Inc.; CitiMortgage, Inc; GMAC Mortgage, LLC; Litton Loan Servicing LP; OneWest Bank, and Select Portfolio Servicing. Treasury said those servicers that fail to improve in the areas identified will be subject to servicer incentive withholding in the future.

"While we continue to get tens of thousands of new homeowners into mortgage modifications each month, we need servicers to step up their performance to meet the needs of those still struggling," said acting Treasury Assistant Secretary for Financial Stability Tim Massad. "These assessments set a new benchmark by providing an unprecedented level of disclosure around servicer performance and will serve to keep the pressure on servicers to more effectively assist struggling families."

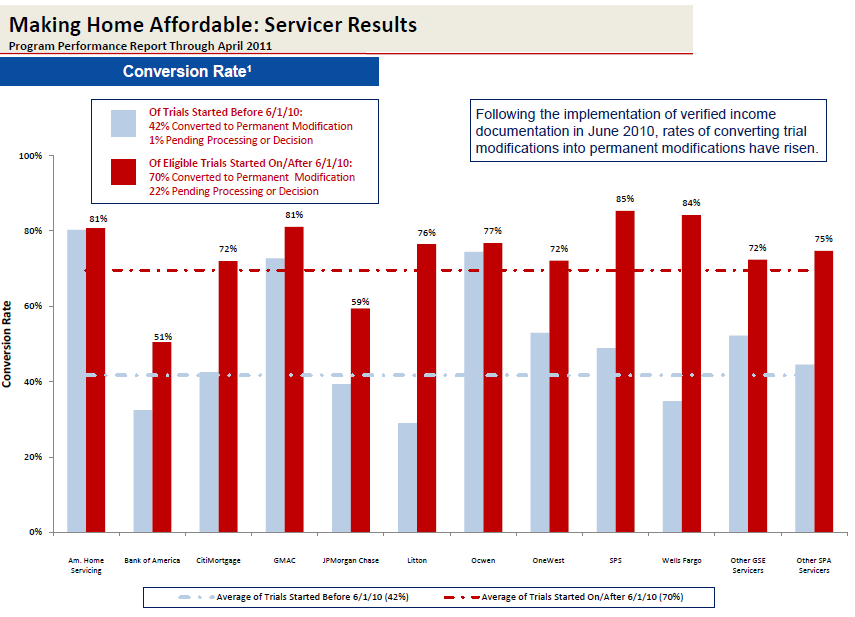

The HAMP report for May indicated that 20,000 more homeowners entered into a trial modification during the month and 29,000 converted from trial to permanent status. Since the program began 1,588,000 borrowers have entered the program and 699,000 have converted to permanent status. Below is a chart illustrating the conversion rate of individual loan servicers.

It is clear that many of the problems that existed with HAMP early on have eased. Seventy percent of trial modifications started since June 2010 have been made permanent and the average length of a trial modification beginning after that that date is 3.5 months. Trial modifications started before that date required an average of 5.2 months before converting to permanent status. In May 2010 the number of borrowers who had been in the "three month" trial modification period for six months or more stood at over 190,000. Today that number has fallen to under 25,000. Below is a chart illustrating the time it takes individual servicers to convert a trial modification to a permanent modification.

Apart from the HAMP report, the Housing Scorecard is primarily a recap of information compiled from other sources and generally covered previously by Mortgage News Daily. This includes Census Bureau reports on construction permitting and housing starts, National Association of Realtors® data on sales of existing houses, RealtyTrac foreclosure statistics and the S&P/Case-Shiller Housing Price Index.

New to this month's report is a Housing Scorecard Regional Spotlight which, in this edition highlights recovery conditions in Phoenix, Arizona, one of the cities hardest hit by the housing downturn. According to Assistant HUD Secretary Raphael Bostic, the administration's programs have assisted over 100,000 families avoid foreclosure in Phoenix. Foreclosures still dominate the market in the city where sales of distressed homes currently represent 56 percent of all existing sales compared to a national figure of 35 percent.