The Mortgage Bankers Association (MBA) today released its Weekly Mortgage Applications Survey for the week ending September 17, 2010.

The MBA's loan application survey covers over 50% of all U.S. residential mortgage loan applications taken by retail mortgage bankers, commercial banks, and thrifts. The data gives economists a snapshot view of consumer demand for mortgage loans.

In a low mortgage rate environment, a trend of increasing refinance applications implies consumers are seeking out a lower monthly payment. If consumers are able to reduce their monthly mortgage payment and increase disposable income through refinancing, it can be a positive for the economy as a whole (creates more consumer spending or allows debtors to pay down personal liabilities like credit cards). A falling trend of purchase applications indicates a decline in home buying demand, a negative for the housing industry and the economy as a whole.

Excerpts from the Release...

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.4 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 22.9 percent compared with the previous week, which included the Labor Day holiday. The four week moving average for the seasonally adjusted Market Index is down 2.3 percent.

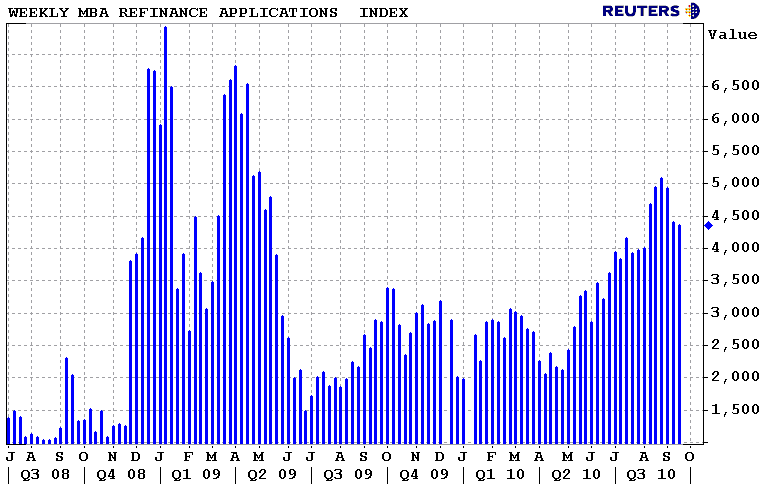

The Refinance Index decreased 0.9 percent from the previous week, which is the third straight weekly decrease. The four week moving average is down 3.0 percent for the

Refinance Index. The refinance share of mortgage activity increased to 81.1 percent of total applications from 80.5 percent the previous week.

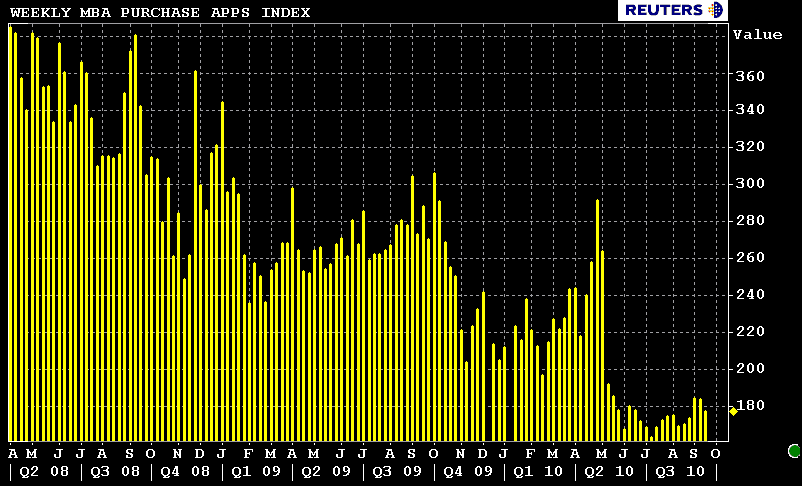

The seasonally adjusted Purchase Index decreased 3.3 percent from one week earlier. The unadjusted Purchase Index increased 18.9 percent compared with the previous week and was 38.0 percent lower than the same week one year ago.

The four week moving average is up 1.0 percent for the seasonally adjusted Purchase Index.

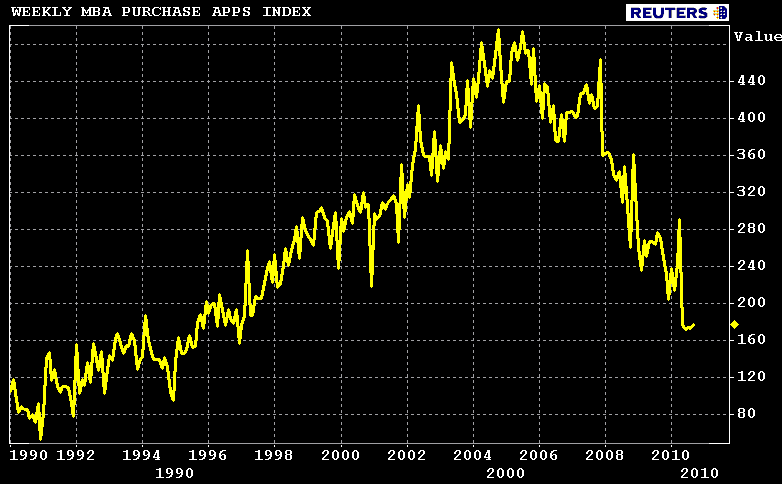

Here is the long term point of view...

The average contract interest rate for 30-year fixed-rate mortgages decreased to 4.44 percent from 4.47 percent, with points decreasing to 0.81 from 1.08 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans. The effective rate also decreased from last week.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 3.88 percent from 3.96 percent, with points decreasing to 0.86 from 1.03 (including the origination fee) for 80 percent LTV loans. The contract 15-year rate is the lowest recorded in the survey, matching the rate from the week ending August 27, 2010. The effective rate also decreased from last week.

The average contract interest rate for one-year ARMs increased to 6.96 percent from 6.89 percent, with points decreasing to 0.21 from 0.23 (including the origination fee) for 80 percent LTV loans. The adjustable-rate mortgage (ARM) share of activity decreased to 5.9

percent from 6.2 percent of total applications from the previous week.

Has refi demand topped out? Have purchase apps bottomed? The latter is far less likely than the former. Color from lock desks confirms the slow down in application activity last week, but you tell me; Are you adding new borrowers to your pipeline as fast as you were in late summer? Are you still refinancing clients who've just refinanced in the past 20 months? Do you think we've hit another peak in refinance demand?

Relative to the week before, our loan pricing data shows mortgage rates were actually worse late last week than they were on Wednesday, Thursday, and Friday in the previous week. This implies the MBA received mortgage rate survey data early last week because borrowing costs went on a three day skid heading into the weekend. Tuesday was the best day to lock. Of course, we can't rule out the fact that retail lenders tend skew the average. Retail generally focuses their pricing strategies on capacity constraints and the amount of loans in their pipeline. On Monday (this week) I heard the biggest retailer had lowered rates considerably. Given the slow down in demand, it is quite possible retail threw off the average as they attempted to pick up some production.