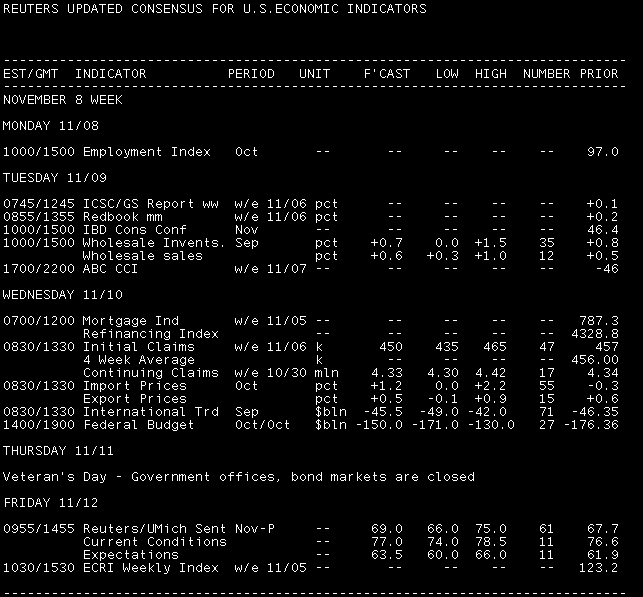

The week ahead brings little new data. The highlight of the economic calendar is the trade deficit on Wednesday and the month’s first consumer sentiment survey on Friday. Other than that the Treasury will conduct debt auctions on Monday, Tuesday, and Wednesday and the bond market is closed on Thursday in observance of Veteran's Day.

Key Events This Week:

Monday:

12:30 ― James Bullard, president of the St. Louis Fed, speaks on "Monetary Policy and Inflation Outcomes in the United States" to the New York Society of Security Analysts

2:45 ― Federal Reserve Bank of Dallas President Richard Fisher speaks on the current state and outlook for the U.S. economy before the Association for Financial Professionals Annual Conference

3:30 ― Federal Reserve Board Governor Kevin Warsh speaks on "The Economy and the Conduct of Monetary Policy" before the Securities Industry and Financial Markets Association (SIFMA) "Invest in America" 2010 Annual Meeting, New York,

Treasury Auctions:

- 11:30 ― 3-Month Bills

- 11:30 ― 6-Month Bills

- 1:00 ― 3-Year Notes

Tuesday:

10:00 ― Wholesale Inventories are anticipated to jump 0.7% in September, adding to a 0.8% gain a month before. The gains follow increases that began in January, according to analysts at BBVA, who said inventories contributed 1.44% to GDP in the third quarter. While not a major market mover, the index does suggest wholesalers are expecting sales to continue rising. The same index showed sales rose 0.5% in August; this month economists look for a 0.6% advance.

“The ISM inventory index in September increased 4.2 points to 55.6 which implies that wholesale inventories continued to rise in September,” noted BBVA. “We expect that wholesale inventories jumped around 0.7% in September.”

Treasury Auctions:

- 11:30 ― 4-Week Bills

- 1:00 ― 10-Year Notes

Wednesday:

7:00 ― MBA Mortgage Applications showed volume down 5% in the final week of October. Refinancings are generally high but have fallen for three straight weeks, while purchases advanced slightly but remain 28% below the level from this time last year.

With the average 30-year fixed-rate mortgage at just 4.28%, refinancings are expected to continue at high levels, but the real question is whether purchases can take flight.

The latest macro-housing news wasn’t positive. Last Friday’s pending home sales index showed contracts for secondary market sales fell 1.8% in September, versus the +3% forecast. That drop was the first since June, leaving the index nearly 25% below last year’s levels.

8:30 ― Initial Jobless Claims averaged 455k per week in October, compared with 458k in September and 487k in August, so the trend is definitely improving. With last week’s monthly employment report beating expectations and sending equities to new heights, there could be extra attention on how many claims turn up in the week ending Nov. 7.

A sustained level below 450k is consistent with net private job growth, according to economists at BTMU, and this week the consensus forecast is precisely at 450k. Some economists look for as few as 440k, while the high end of the range is just 455k.

Meanwhile, continuing claims ― a tally of those still receiving regular jobless benefits ―fell 42k to 4.340 million in the week ending Oct. 23.

8:30 ― The U.S. Trade Balance is expected to narrow slightly in September to -$45.5 billion, according to the consensus call from Reuters. One factor helping reign in the gap is a decline in both volumes and value of petroleum products. The prior month’s deficit expanded more than $4 billion to $46.4 billion, as a 0.2% gain in exports wasn’t enough to keep pace with the 2.1% jump in imports. Total exports were $153.9 billion; total imports were $200.2 billion worth of goods and services.

“Following the August surge in imports, businesses will want to avoid overstocking and we expect a drop in consumer goods and autos imports,” said economists at IHS Global Insight. “On the export front, increased aircraft exports should partly offset declines for industrial supplies and capital equipment exports. Looking into the fourth quarter, we expect trade to become a boost to growth as import growth slows and a weaker dollar supports U.S. export competitiveness.”

2:00 ― The Treasury Budget Statement for October 2010 should record a monthly deficit of $153.5 billion, according to economists polled by Reuters. Big as that gap is, it’s a reduction from the $176 billion hole seen one year before, so it may not be a bad start to the new fiscal year.

The total budget gap for the fiscal year ending last month was $1.29 trillion debt, or 8.9% of GDP, according to Bloomberg, which notes that the October deficit has averaged$53.6 billion over the past decade.

Treasury Auctions:

- 1:00 ― 30-year Bonds

Thursday:

No data ― Veterans Day. Stocks & Futures Markets open.

6:45 ― Federal Reserve Bank of Atlanta President Dennis Lockhart discusses current economic topics before the "Employment and the Business Cycle" conference hosted by the Federal Reserve Bank of Atlanta,

Friday:

8:35 ― Federal Reserve Board Governor Daniel Tarullo speaks on "Next Steps in Financial Regulatory Reform" before the Center for Law, Economics, and Finance conference on the Dodd-Frank Act

10:00 ― The Reuters / U of Michigan Consumer Sentiment index is expected to rise to 69.0 in mid-November from 67.7 at the end of October. Gains are always welcome, but with October’s score at a calendar year low, it will take more than a two-point gain to have analysts optimistic that consumers are ready to spend. Forecasters are hoping the recent rise in equities will play a key role in boosting optimism ― the benchmark S&P 500 has jumped almost 17% since Aug. 31.

“The questions within the University of Michigan survey are geared more toward financial markets so sentiment should get a lift from the recent run-up in equities,” said Ellen Zentner at BMTU, noting that the first read on consumer sentiment each month carries the most market weight.

While looking for an increase, Zentner also noted that the broadest BLS measure of unemployment, which includes discouraged workers, actually ticked higher in September to 17.1%, compared to 17.0% in September 2009.

Economists at BBVA said other recent macroeconomic has been more positive, including an increase in auto sales and bumps in manufacturing indexes. Those should help the index rise after falling for the previous two months.

4:35 ― Federal Reserve Board Governor Sarah Bloom Raskin speaks on "Mortgage Servicing Issues" before the National Consumer Law Center Consumer Rights Litigation Conference,

,

,