The progressively more tragic consequences of the Japanese earthquake remind us that reality can change in an instant. What we initially received as news of an earthquake several thousand miles away has amounted to a living hell for the people of Japan.

The death count is unknown but is much worse than initially thought. Power outages are widespread. Roads are closed along the coastline. Water, food and fuel shortages are being reported. And now there are growing fears of a major radiation leak at the Fukushima nuclear complex, which is 140 miles north of Tokyo.

"The devastation caused by the Tohoku Pacific Offshore Earthquake and subsequent tsunamis is even greater than initially estimated," said economists at Nomura Global Economics, a Japanese bank, who said 11 nuclear reactors and three oil refineries shut down after the earthquake.

"The size of the economy of the main earthquake-affected region is roughly the same as that of the area hit by the Great Hanshin (Kobe) earthquake in 1995, but with this Tohoku Pacific (Sendai) earthquake affecting road networks, power plants and other infrastructure over a wide area, we expect the short-term economic impact to be greater than the Kobe earthquake," they added.

The Bank of Japan implemented emergency short-term fund-supply operations and has increased the purchase of its repurchase agreements to prevent financial meltdown.

While we expect Japanese headlines to grab the world's attention in the week ahead, the show must go on. The main event in the U.S. is a one-day FOMC meeting. When the FOMC Statement is released at 2:15pm on Tuesday afternoon, the Federal Reserve is not expected to announce any change in the QEII Treasury purchasing program. Bernanke and the Board of Governors should say the economy continues to improve at a moderate pace, but not fast enough to rapidly repair the ailing labor market. A comfortable view of inflationary pressures is expected to be communicated, but a nod may be given toward rising food and energy prices as a short-term burden on consumer balance sheets. A potential wildcard of the FOMC meeting is the chance for a few dissenting votes.

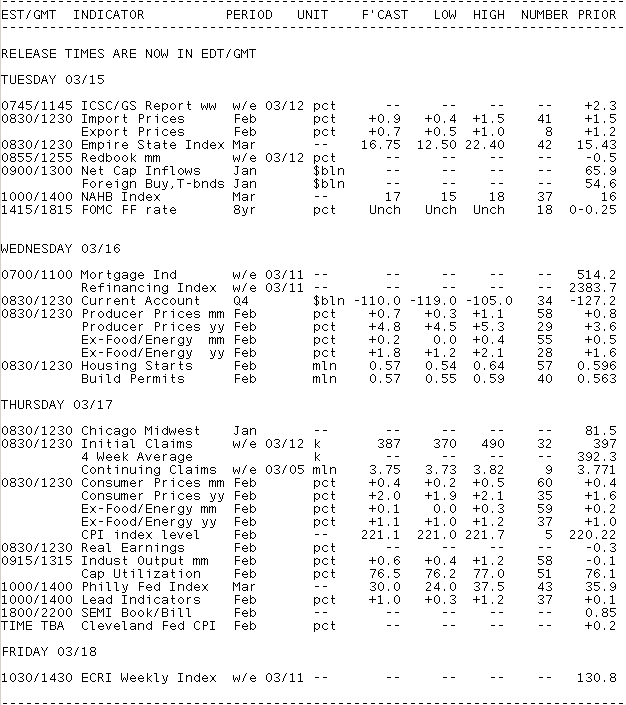

Key Events This Week:

Monday:

10:15 - The Federal Reserve will purchase an estimated $6.5 to 8.5 billion in Treasury securities maturing between 5/15/2018 and 2/15/2021

Tuesday:

8:30 - Little is expected to have changed in the Empire State Manufacturing Survey, which hit an 8-month high last month when it rose 3.5 points to 15.4. Economists anticipate a 16.0 score this month, with predictions ranging between 14 and 20. Any number above zero reflects growth, so these figures are optimistic albeit less encouraging that the Philadelphia Fed numbers.

"We expect the Empire State index to fall slightly to 15.0 in March from an eight-month high of 15.4 in February," said economists at Nomura Global Economics. "The manufacturing sector looks solid, with all the major survey indices reporting healthy results in recent months, but surging energy and commodity prices are likely to begin tempering business confidence."

10:00 - The NAHB's Housing Market Index, a gauge of homebuilder sentiment, has remained stagnant at 16 for the past four months. With any number below 50 representing pessimism, the index is a far cry from optimism and minor fluctuations can be comfortably ignored. It may be worth noting the 6-month outlook improved a point to 25 last month.

"The index of homebuilders' business sentiment has not been above 20 since August 2007," economists at Nomura Global Economics said. "It is unlikely to break into the 20s any time soon but we expect warmer weather and an improving job market to help push the March index up one point to 17."

2:15 - The FOMC Meeting Announcement isn't expected to produce any major changes in monetary policy. The Fed Funds target rate should remain in the zero to 0.25% range, while its quantitative easing program of asset purchases should remain on schedule to terminate at the end of June. Still, everyone reads the statement and any changes to the language will be closely monitored.

Wednesday:

8:30 - Housing Starts are forecast to take a fall in February after a sharp 14.6% jump upwards to start the year. Economists polled by Reuters look for the annualized pace of housing construction projects to fall to 560k from 596k a month before, reflecting some correction to the earlier volatility. January starts rose solely because of a 78% gain in multi-family units, while single-family units - a more closely-watched component - slipped 1%.

"Big spikes in housing starts are usually followed by corrections in the following month," note economists at IHS Global Insight. "Overall we project that housing starts dropped around 3% to a 580,000 annual rate in February. We expect permits to make small but steady improvements over the course of the year as job growth picks up. For February, we project that housing permits increased around 2% to a 574,000 annual rate."

8:30 - Expect the Producer Price Index to rise 0.7% in February, economists say. The headline is expected to jump on rising energy prices, the same culprit that pushed the index up 0.8% one month before (gas prices, for instance, were hiked 6.9%). The core index, which excludes volatile energy and food prices, is anticipated to rise 0.2% after a 0.5% uptick in January. Annually, headline prices were up 3.6% while core prices were 1.6%.

"Producers have been getting squeezed by higher energy costs since October," said economists at BTMU, who noted that headline wholesale prices rose an average +0.7% each month between October and January.

"The usual culprits are at play in February, where we believe food prices rose +2.3% and energy prices rose +1.2%," they added. "Strip out those two components and core wholesale inflation is expected to be flat."

10:15 - The Federal Reserve will purchase an estimated $5.5 to7.5 billion in Treasury securities maturing between 3/31/2015 and 8/31/2016

Thursday:

8:30 - Initial Jobless Claims rebounded by 26k to 397k in the week ending March 12. Economists hope the downward trend resumes this week, with the consensus looking for 385k new claims for unemployment benefits. Predictions are in a pretty narrow range between 380k and 395k, in line with the February average of 389k.

"The most recent report marks the fourth week in the last five with a sub-400k filing rate," noted economists at Nomura Global Economics. "Although claims rose to 397k last week, the four-week average remained near 2½-year lows. We expect more readings in the 300,000s in the coming weeks."

8:30 - Rising energy prices accounted for two-thirds of the 0.4% uptick in January's Consumer Price Index. February's story is supposed to be much the same with another 0.4% gain in the cards, economists predict. The core index (ex-food and oil prices) is supposed to inch forward 0.1% following a 0.2% rise the month before - the biggest increase since October 2009. Annually, headlines prices were up 1.6% and core prices were up 1%.

"Prices at the consumer level are getting pushed up by energy, specifically gas prices," said economists at BTMU. "The national average for a gallon of gas hit $3.57 in the week of March 7th, and prices averaged $3.26 in February - +3.7% higher compared to January. We think the energy component of CPI likely increased by +3.5% in February with price increases elsewhere in medical care, transportation, housing, and food. Year-over- year headline prices are expected to rise by +2.1% - the highest since April 2010."

9:15 - Industrial Production, the key report for the week, is expected to climb 0.6% in February following a 0.1% slip in January and a 1.2% gain in December. Predictions range from 0.5% to 0.9%. Wild weather swings were blamed for the January decline as utilities output dropped 1.6%, whereas manufacturing output was up 0.3%.

"All manufacturing surveys point to a strong month, much better than January, when factory output was held by inclement weather," said economists at IHS Global Insight. "February hours worked in manufacturing rose 0.7%, and along with higher vehicle output, should boost the manufacturing sector to a better than 1.0% gain."

10:00 - Leading Economic Indicators, a composite gauge that seeks to anticipate turning points in the economy, has been rising for the past seven months straight. The January index rose just 0.1% though, down from a 0.8% gain to end 2010. Economists look for a more robust 1% gain in February, as economic data continued to be optimistic for the month, particularly in the labor markets.

"The drop in initial filings for unemployment insurance in February-to an average of 389k from 432k in January-is the greatest contributor to the index, followed closely by the widening spread between 10-year Treasuries and Fed Funds," said economists at Nomura Global Economics.

10:00 - The Philadelphia Fed Survey is expected to moderate after leaping to a seven-year high in March. The index rose 16.6 points to 35.9, as all components grew including the employment index - it rose to from 17.6 to 23.6, its highest since May 1973. Economists at Nomura called it the most "encouraging indicator from the manufacturing sector since well before the Great Recession began three years ago."

10:15 - The Federal Reserve will purchase an estimated $5.5 to7.5 billion in Treasury securities maturing between 9/30/2013 and 2/28/2015

Friday:

10:15 - The Federal Reserve will purchase an estimated $1 to 2 billion in Treasury Inflation Protected Securities maturing between 4/15/2013 and 2/15/2041

A few charts and some perspective from AQ/MG's latest MBS commentary: MBS LEDGE: Room to Rally with Little Reward to Offer

The FNCL 4.5 MBS coupon is looking to trade back into the 7-week range we unceremoniously occupied from late-December to late-January. Read on...

In benchmark TSYs we've noticed a real push back lately every time 10s cross through 3.40% resistance. These are real money hedgers fighting a potential move "down in coupon"....fighting a shift in duration bias that would force them to adjust their asset/liability cash flow management strategies. That can be a costly endeavor if the market is not totally committed to an interest rate rally...which it clearly isn't right now. A hesitancy to rally makes perfect sense in that regard...

It'll take a steady drip of bond market friendly news and events to break the even bigger resistance level that lies at 3.30%.

10s have traded below 3.40% and FNCL 4.5s have been bid over 102-00 in the past two-months, but "Best Execution" never improved past 4.875% (4.75% was reported but not widespread). And it's not gonna happen unless lenders start hedging their pipelines with 4.0 MBS coupons again. You might have read this on MND once or twice or ten times lately...

"Lenders have moved the Best Execution 30-year fixed note rate as low as they possibly can without drastically altering their pipeline hedging strategies. This is a factor of what production mortgage-backed security coupon is most liquid in the secondary mortgage market. On conventional loans, the 4.50 percent MBS coupon is the hedging vehicle of choice for lock desks. Home loans with note rates between 4.875 and 5.25% are generally used to fill 4.50 percent MBS coupon trades. Until MBS investors demonstrate sustainable demand for 4.00 percent 30-year fixed MBS coupons, lenders will not find it economically efficient to quote 4.75 percent note rates without expensive permanent buydown costs. From that perspective, if you are floating a conventional home loan interest rate, you should not be expecting further improvements to your actual rate in the short term. If the bond market recovery rally continues, closing costs will improve, but on the whole, it will take a sustained move higher in 4.00 percent MBS coupon prices for Best Execution to dip below 4.875 percent."

THIS LEAVES US STUCK ON ANOTHER LEDGE.....

The chart below is one way to illustrate our point. It graphs the price difference between the FNCL 4.5 MBS coupon and the FNCL 4.0 MBS coupon. Right now the price spread between the two coupons is 3.45 points or 345bps. The last time we saw lenders hedging with 4.0 MBS coupons, the spread was closer to 280bps. 4.0s have a lot of catching up to do! A flatter yield curve would certainly help our cause...

The FN 4.5/4 swap trades in ticks but we're gonna present it to you in bps to keep it simple.

Now for an update on our long-term 10yr TSY note chart. We think the bond market is repeating history. If that theory turns out to be the case, our target in 10s in 2.85%. 4.00% MBS coupons would surely be trading at that point. If not, this is as good as it gets!

GUIDANCE FROM OUR MORTGAGE RATES COMMENTARY: The failure of the bond market to extend its recent rally really serves to drive home a point we've been harping on for several weeks now: WE'RE STUCK. If you're floating, you're doing so for marginal improvements in UPFRONT COSTS ....not RATE. When it comes to the outlook for lower rates in the months ahead, we're still optimistic about that expectation but realize it will require a steady drip of bond friendly (economy-unfriendly) news and events . In the short-term, or at least until "the levy breaks" and all hell breaks loose around the planet, we don't expect lender rate quotes to look much better than they do right now.