The Office of Inspector General (OIG) for the Federal Housing Finance Agency (FHFA) has released an assessment of the FHFA's oversight of troubled banks within the Federal Home Loan Bank (FHLBank) System. While the OIG found positive actions on the part of FHFA, it specifically criticized a lack of policies, systems, and documentation standards that could strengthen that oversight.

Of the 12 FHLBanks that exist regionally, four have experienced significant financial and operational difficulties dating back to at least 2008. The four, located in Boston, Chicago, Pittsburgh, and Seattle and classified as of "supervisory concern" due to problems arising from their investments in certain high-risk mortgage securities.

The primary mission of FHLBanks is to support housing finance and the system issues debt in the capital markets at relatively favorable rates due to its status as a government sponsored enterprise (GSE). The proceeds of the debt are used by the individual banks to make secured "advances" to member financial institutions which secure these advances using single-family mortgages or investment-grade securities as collateral. The FHLBanks also hold investment portfolios that contain assets such as mortgage-backed securities (MBS).

FHFA has oversight responsibility for the FHLBanks and recognizes the need to ensure that they do not abuse their GSE status or act imprudently. FHFA's own examination guidance states that the agency will initiate a formal enforcement action, such as a cease and desist order, when a bank is identified as having significant "supervisory concerns" within the system.

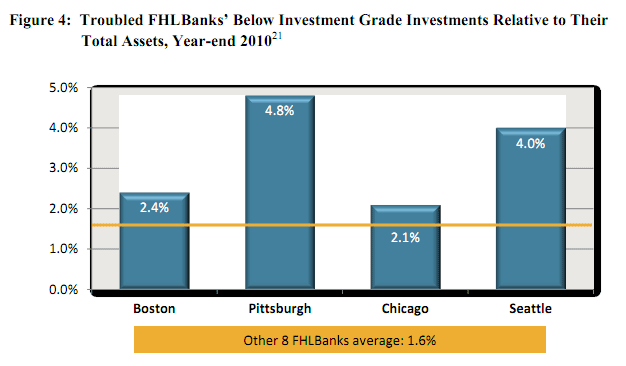

According to the OIG, the four troubled banks have experienced "significant financial and operational deterioration primarily due to their investments in private-label MBS secured by non-traditional mortgages." Two of the banks, in fact, hold more than twice the level of securities rated "below investment grade" than the average for the eight healthier banks.

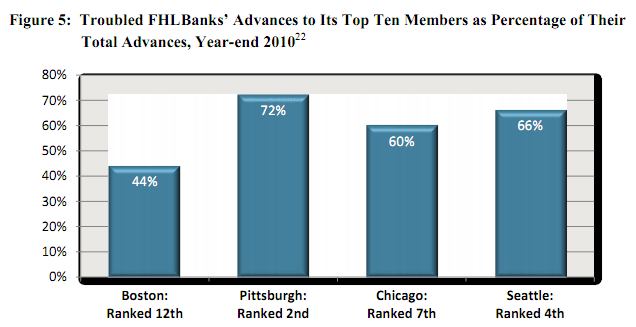

Another identified risk is a concentration of advances in a few member banks. Both the Pittsburgh and Seattle banks have a high percentage of their advance business confined to ten members (the situation only recently changed in respect to Boston) which leaves them vulnerable should one or more such institutions fail or withdraw from the system. OIG also found that the troubled banks tend to demonstrate a limited demand for advances, a high percentage of investments to total assets, and significant risk management and operational deficiencies.

OIG said a major concern is that troubled FHLBanks potentially have greater incentives to engage in higher risk business strategies in order to achieve higher returns. This means that FHFA needs to monitor their activities and control actions that could potentially lead to greater financial and operational deterioration and cause greater long-term risks.

The OIG found that FHFA has taken some steps to monitor and control the four banks which present "supervisory concern."

- Ensuring that they restrict the payment of dividends to preserve their retained earnings and capital.

- Encouraging FHLBank boards to place limits on investment activities.

- Monitoring through annual examinations and regular communications.

- Discussing with board members and managers the possibility of merging with healthier FHLBanks.

While FHFA's examination guidance specifies enforcement, OIG claims that FHFA does not view this as constituting a policy or requiring a course of action. FHFA believes, by initiating enforcement action on a case-by-case basis it has acted appropriately.

The OIG disagrees and views "FHFA's lack of a consistent and transparent written enforcement policy as undermining the Agency's oversight of troubled FHLBanks." FHFA and its predecessor FHFB have initiated formal enforcement against only two of the banks, Consent Orders issued against Chicago in 2007 and Seattle in 2010.

OIG faulted FHFA for the following:

- Its failure to establish a clear, consistent and transparent written enforcement policy for troubled banks has led to a discretion-based approach. This, in turn, has resulted in a lack of clarity for FHFA examination staff and the banks, neither of which have steady benchmarks against which to gauge their actions.

- The Agency has not established an automated management information reporting system to track FHLBank examinations finds. By relying instead on a manual system, FHFA managers are limited in their ability to assess the extent to which individual banks are correcting deficiencies and this has also impeded the ability of the OIG to assess the effectiveness of the Agency's oversight efforts.

- FHFA does not consistently document key actions with respect to its oversight of the troubled banks. This was a problem that OIG found particularly troublesome as applied to personnel actions as it identified cases where FHFA had influenced boards to terminate employees without adequately documenting its actions or the reasons for them.

In concluding its report the OIG made three specific recommendations which paralleled the above findings; recommending that FHFA

- Develop and implement a clear, consistent and transparent written enforcement policy that requires troubled banks to correct identified deficiencies within a specific time frame, establishes consequences for failure to do so, and defines exceptions to the policy.

- Develop and implement a reporting system that permits Agency managers and outside reviewers to assess examination report findings, planned corrective actions and timeframes, and their status.

- Document key activities consistently including personnel actions involving FHLBanks.

The performance period for this evaluation was from May 2011 to November 2011.