While it trails well behind credit history and debt-to-income levels, collateral problems are consistently the third most frequent cause of loan denials. CoreLogic said Home Mortgage Disclosure Act (HMDA) data for 2015 show collateral issuers were the reason behind 13.7 percent of the 450,000 first-lien purchase mortgage applications that failed approval.

The share of loans turned down for collateral reasons has remained consistently in the 12-13 percent range since home prices began to recover in 2012. But Yanling Mayer, writing in CoreLogic's Insights blog, says there is a wide variation in collateral denials on a geographic basis, ranging from 7 percent in Delaware to 22 percent in Michigan. While lenders don't provide specific causes in their HMDA reports, Mayer says appraisals coming in below the contract selling price is common. Data from other sources show 10 to 13 percent of appraisals nationwide come in below the contract sales price, a number consistent with HMDA data.

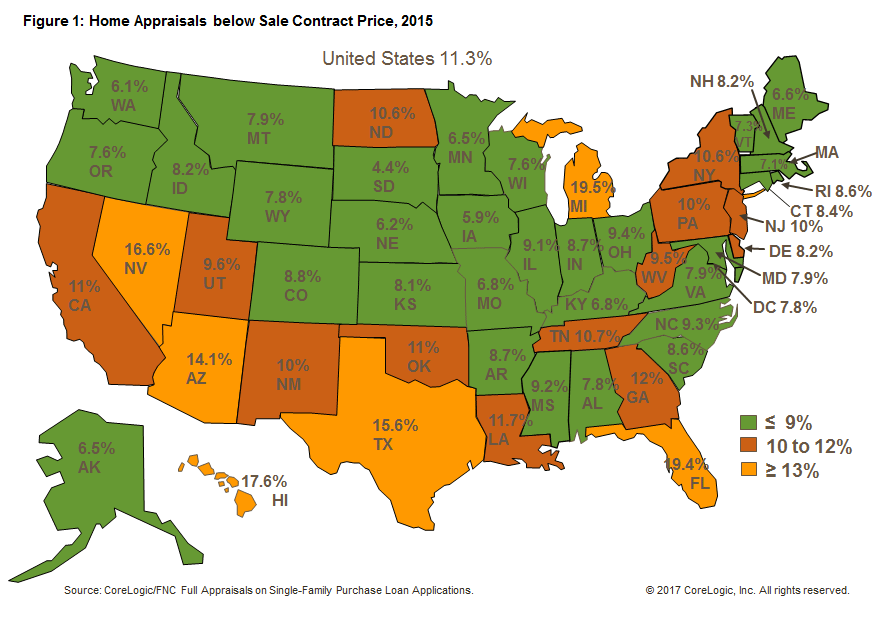

Those below-contract value figures, which average 11.3 percent on a nationwide basis in 2015 and through November 2016, also vary widely at the state level. Only about a dozen states exceed that national average, but CoreLogic points out that the frequency of too-low appraisals in Michigan at 20 percent and Hawaii at 18 percent are very close to their failed collateral percentages of 22 and 20 percent from HMDA. As Mayer says, "likely not a coincidence."

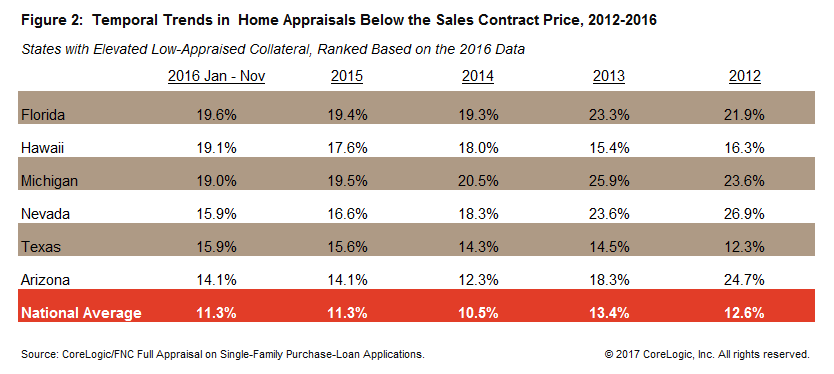

In addition to geographic variations Mayer points to several "temporal" differences. Most states show a small-to-modest decline in the number of appraisals that come in under the arms-length contract price as the recession recedes, but they nevertheless stay close to the 7-9 percent range. What stands out the most are Florida, Hawaii, Michigan, Nevada, Texas and Arizona in which, despite rising sales and a strong market recovery, have appraisals that continue to come in relatively frequently at a too-low level.

As of November, nearly one in five appraisals in Florida and Michigan come in under contract price. For Florida, the improvement from 21.9 percent in 2012 to 19.6 percent is rather modest given the state's steadily rising sales volume, declining distressed sales, and strong home price growth. The same moderate improvement is noted in Michigan. In Nevada and Arizona, on the other hand, the incidences of low-appraised collateral fell significantly during the same period marked, similarly, by a strong housing recovery and Hawaii and Texas experienced upticks in low appraisals even though they too have had significant declines in the volume of REO and short sales, rising housing activity and solid home-price growth.

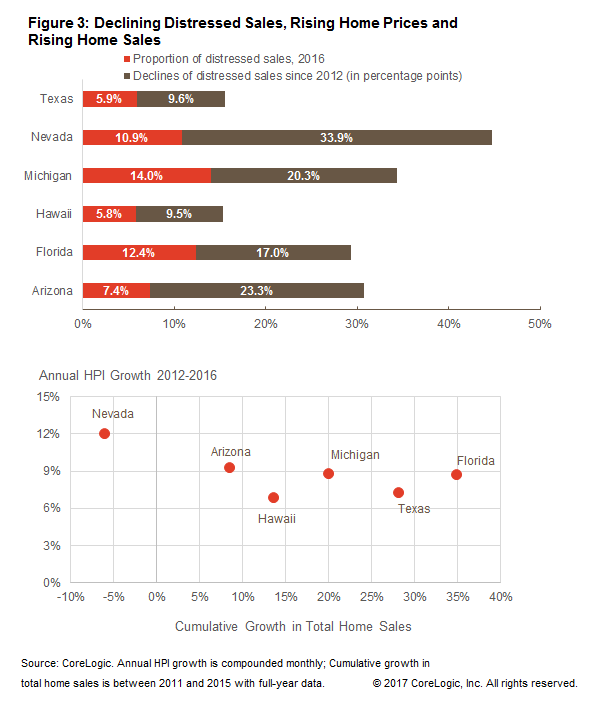

Mayer concludes that due to its reliance on sales comparisons, the quality and accuracy of home appraisals can only be as good as the availability and quality of the appraiser's comps. The pool of available comparables can be impacted by many factors such as local sales activity, level of housing distress, whether the subject property is itself distressed, and where the property falls in the price tiers. These, along with appraiser experience, can all influence the appraisal accuracy.