Taken together, two recent posts in the CoreLogic Insights blog may indicate that, after several years of being a close trade-off or even more affordable than renting, buying a home might be losing any advantage.

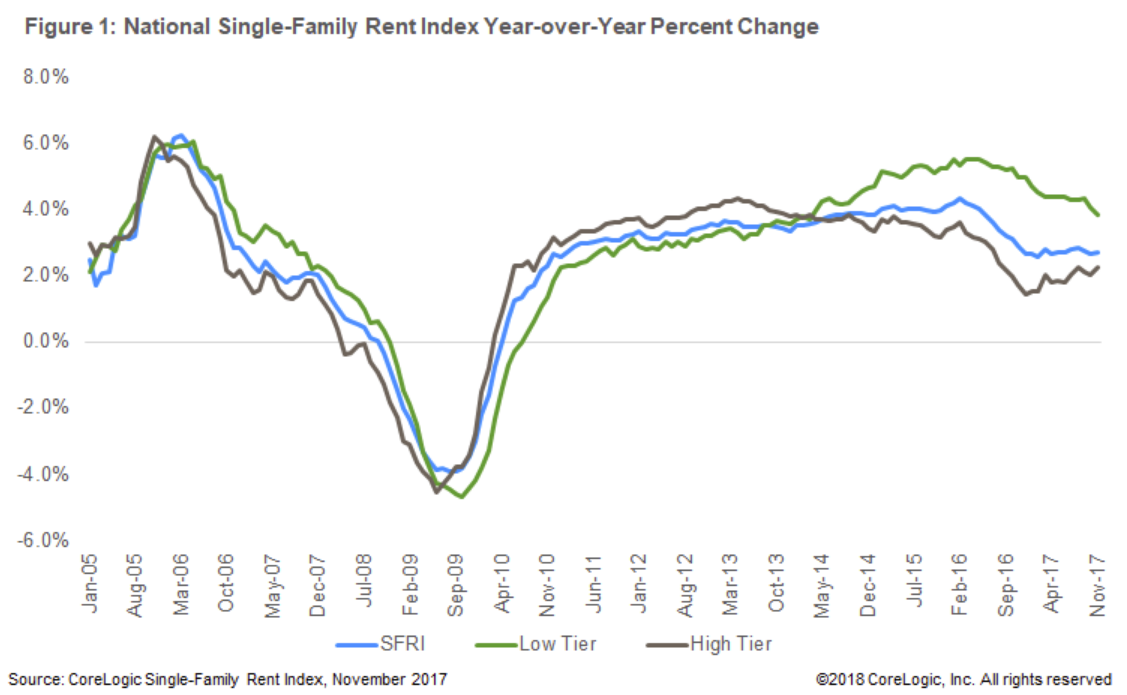

Shu Chen writes that the growth in rents nationwide seems to be slowing after seven years of steady increases. CoreLogic's Single-Family Rent Index (SFRI) shows that year-over-year rents, were increasing on an annual basis when the rate topped out at 4.3 percent in February 2016. The growth has been decelerating slowing since then. In November 2017 the year over year increase was 2.7 percent.

The Index measures changes to the cost to rent single-family rental homes, including condominiums, using a repeat-rent analysis to measure the same rental properties over time. The analysis is conducted both nationally and for 75 individual Core Based Statistical Areas (CBSAs). Of 20 select metros analyzed, only Honolulu and Miami experienced a decrease in single-family rents in November.

The slowdown however has not been universal. Higher priced properties are continuing to see rent increases accelerate. Properties with rents above 125 percent of the region's median, increased 2.3 percent on an annual basis in November 2017, up from a year-over-year gain of 1.7 percent the previous November. At the low end of the market, properties with rents under 75 percent of the regional median had rent increases of 3.8 percent compared to gains of 5 percent a year earlier.

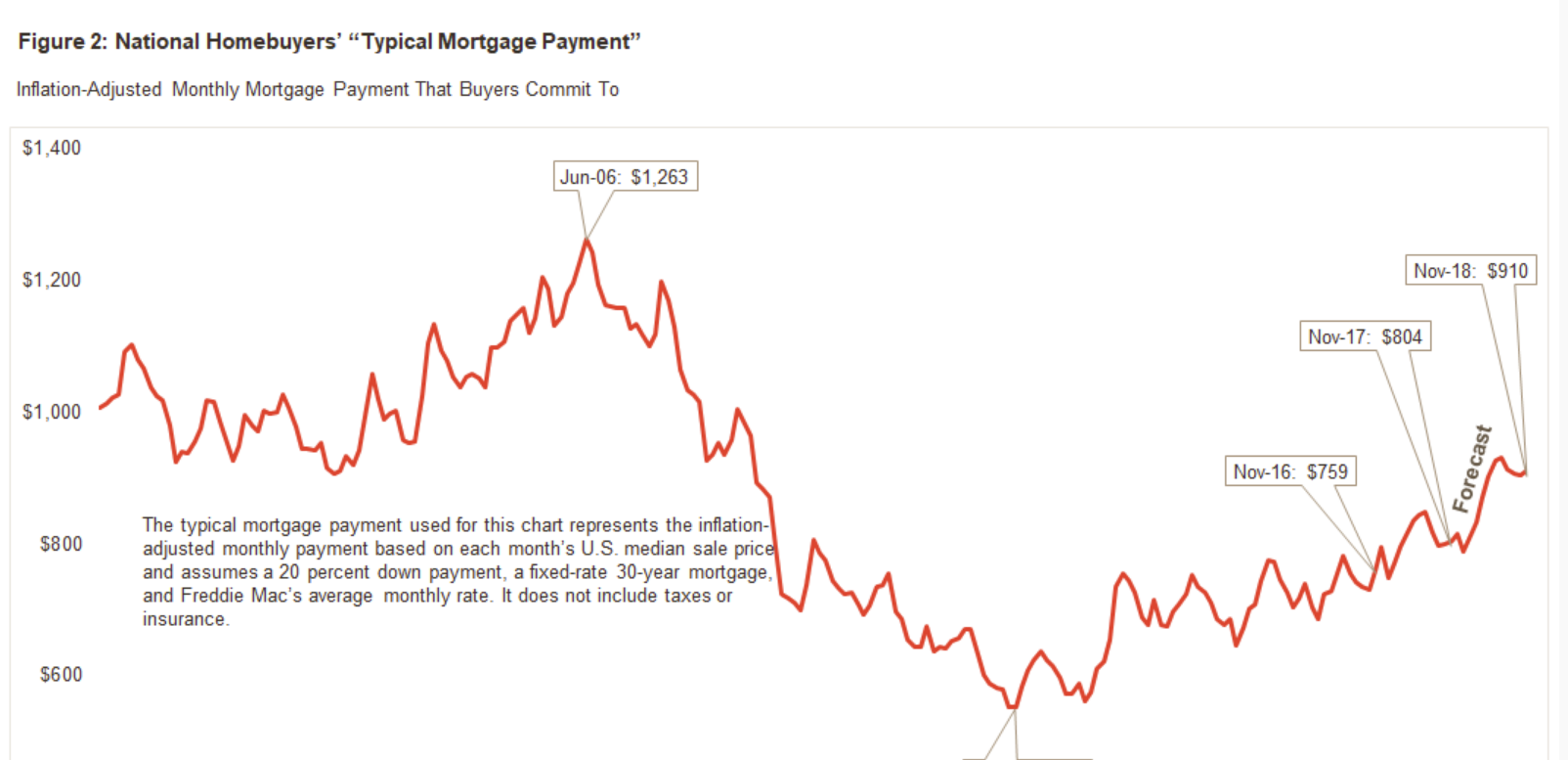

The cost of purchasing a home, on the other hand, may be accelerating faster than actual home prices indicate. Andrew LePage says that the forward looking CoreLogic Home Price Index (HPI) is forecasting a 5 percent increase in home prices this year but should some mortgage rate forecasts for the year pan out, homebuyers may face mortgage payments that have risen by three times that amount.

The typical mortgage payment, he says, is a good proxy for affordability because it shows the monthly amount for which a homebuyer would have to qualify to get a mortgage on a median priced home. That payment is a way to measure the impact of inflation, mortgage rates, and home prices over time and is calculated using Freddie Mac's average rate on a 30-year fixed-rate mortgage with a 20 percent down payment. It does not include taxes or insurance.

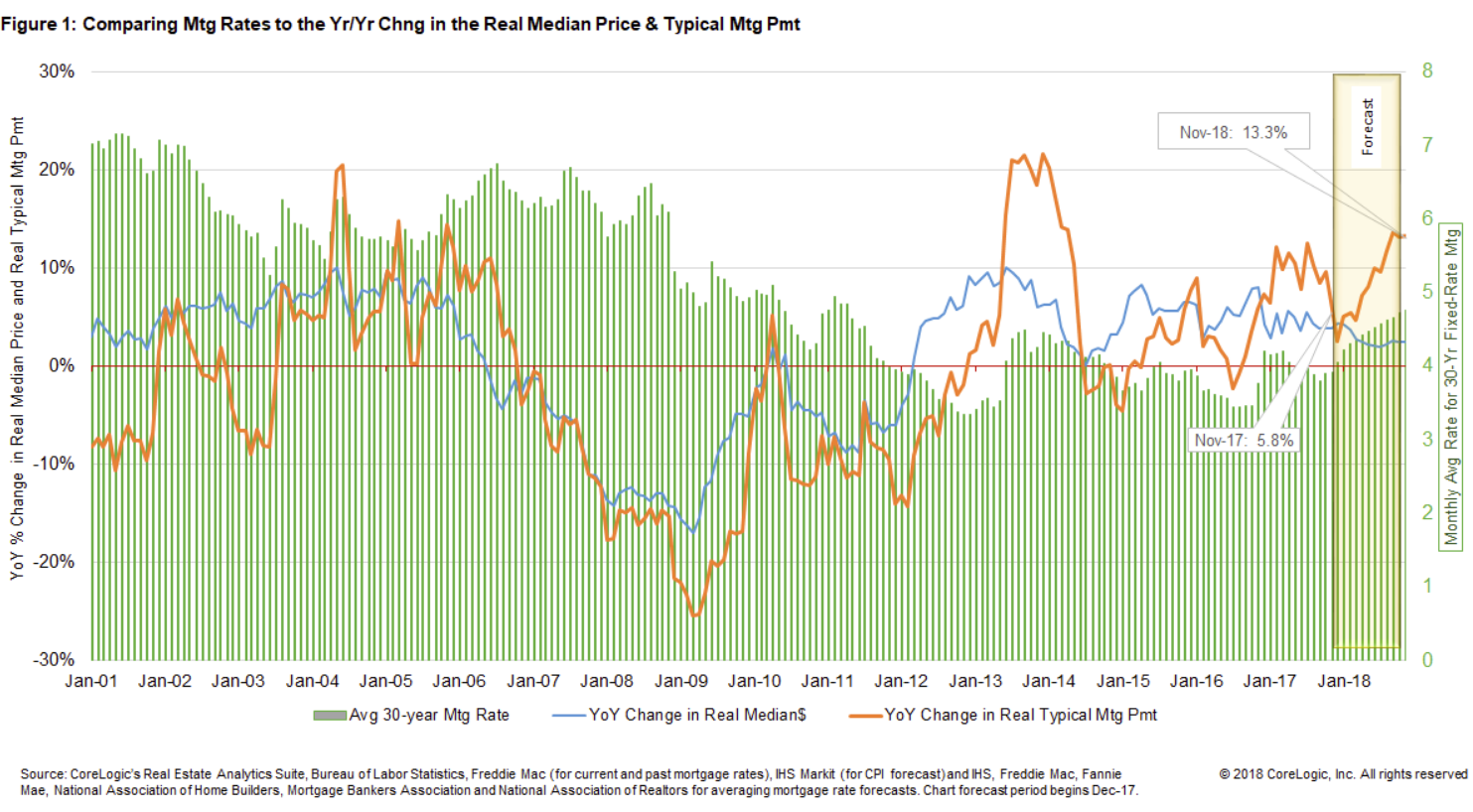

A consensus forecast suggests mortgage rates will rise by about 85 basis points, between November 2017 and November 2018. The CoreLogic HPI Forecast suggests the median sale price will rise 2.6 percent in real terms over the same period (or 4.6 percent in nominal terms). Based on these projections, the inflation-adjusted typical mortgage payment would rise from $804 in November 2017 to $910 by November 2018, a 13.3 percent year-over-year gain. In nominal terms the typical mortgage payment's year-over-year gain would be 15.5 percent.

Another projection from IHS Markit forecast is for real disposable income to rise by just under 4 percent this year, meaning homebuyers would see a larger chunk of their incomes devoted to mortgage payments.

When adjusted for inflation the typical mortgage payment puts homebuyers' current costs in the proper historical context. Figure 2 shows that the inflation-adjusted typical mortgage payment has trended higher in recent years, in November 2017, with interest rates at 3.9 percent, it remained 36.4 percent below the all-time peak of $1,263 in June 2006 when the average mortgage rate was about 6.7 percent. The inflation-adjusted median sale price in June 2006 was $245,259 (or $199,900 in 2006 dollars), compared with a November 2017 median of $212,460.