Commercial and multifamily mortgages continue to have the lowest rates of charge-offs of any loan types at banks and thrifts and perform better than the overall loan portfolios at those institutions according to the Mortgage Bankers Association (MBA).

In response to what it referred to as a great deal of discussion and conjecture about those loans in recent months, MBA updated an earlier "DataNote" analysis of commercial and multifamily mortgage data from the 4th quarter of 2008 with data from the same period in 2009.

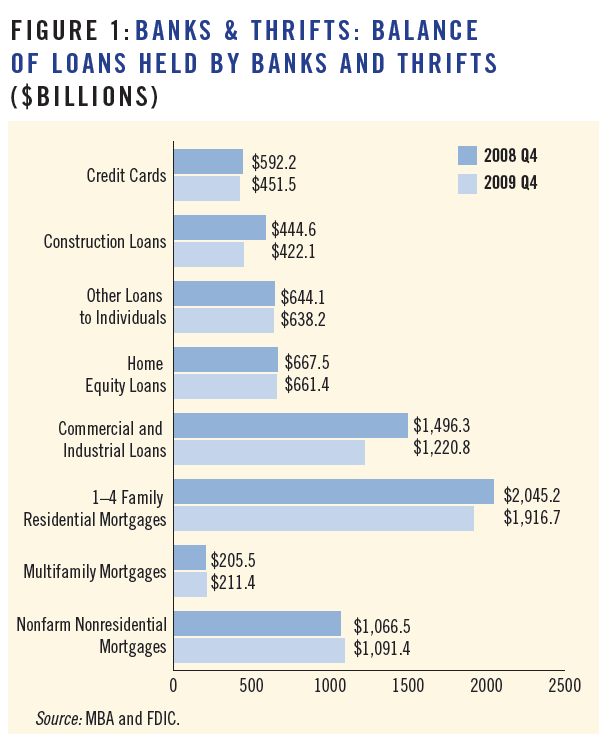

The report states that 56 percent of the assets held by banks and thrifts at the end of 2009 consisted of loans and leases, a category that includes 1-4 family mortgages, home equity loans, credit cards and other consumer loans, commercial mortgages, multifamily mortgages, construction loans, and commercial and industrial loans. One to four family residential loans constitute the largest part of this category of bank holdings at $1.9 trillion or 26 percent of the total; commercial and commercial mortgages represent another $1.1 trillion or 15 percent, and commercial and industrial loans $1.2 trillion or 17 percent. Multifamily mortgages are a much smaller component at $211 billion or 3 percent of the portfolios but these are the only category of loan to have grown over the last year.

From the release:

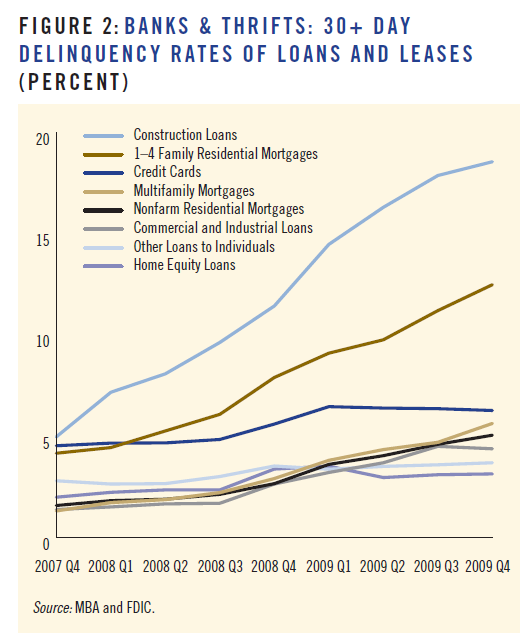

The overall 30+ day delinquency rate among all loans in the 4th quarter of 2009 was 7.30 percent. Commercial mortgages had a 5.06 percent delinquency rate during the quarter and multifamily mortgages loans 5.64 percent. The best rates were recorded by commercial/industrial loans at 4.39 percent and, surprisingly, home equity loans at 3.15 percent. It should be noted that about 45 percent of the commercial mortgage category is comprised of business loans backed by owner-occupied property and supported by the income of those businesses rather than by income producing rental property.

Construction loans had the highest 30+ day delinquency rates among the various loan types, spiking from around 5 percent in the 4th quarter of 2007 to 18.6 percent by the 4th quarter of 2009. The report said that this increase was driven mainly by poor performance among single-family related land and construction loans. Single-family mortgages were second with a 12.49 percent rate, and credit cards were third at 6.28 percent.

Delinquency rates increased across most categories with overall delinquencies among all loans and leases up by 0.44 percent from the third quarter of 2009 to the fourth. Commercial mortgages increased 0.5 percent and multifamily mortgages were up 0.9 percent. Single-family mortgages increased by 1.3 percent and construction loan delinquencies were 0.7 percent higher.

As is historically the case because of the value of the underlying security, commercial and multifamily mortgages had the lowest charge-off rates of any type of loan at commercial banks and thrifts during 2009. 0.8 percent of commercial mortgages and 1.1 percent of multifamily mortgages were charged-off during 2009 compared to 1.7 percent of 1.4 family residential loans, 2.4 percent of commercial and industrial loans, 2.9 percent of home equity loans and 9.1 percent of credit card loans.

In dollars, the charge-offs of commercial and multifamily mortgages are also low in relative terms. Over the last two years banks and thrifts have charged off $105.5 billion in loans to individuals, $83 billion in residential loans, $51 billion in commercial and industrial loans, and $47 billion in construction loans but only $11 billion in commercial mortgages and $3 billion in multifamily loans. MBA makes the assumption that had banks lent the money they have given to commercial and multifamily mortgages to other types of loans instead, they would have suffered roughly $36 billion in charge-offs during 2008 and 2009 that they have not seen.

The MBA report points out commercial and multifamily mortgages have, like other parts of the economy, been negatively impacted by job losses, consumer restraint and manufacturing declines. The relatively stable performance and low charge-offs of commercial mortgage through the recent recession, however, have helped rather than hurt the stability of banks and thrifts.