Fannie Mae's economists remain upbeat about economic growth in the medium term but said on Monday that they see increasing downside risks. In its March forecast, the company's Economic Research Team had predicted that growth would slow during the first quarter but with a subsequent pickup that would result in growth of 2.8 percent in 2018. In its current edition of Economic Developments, they say growth slowed more in the first quarter of the year, to 1.7 percent rather than the 2.1 percent expected earlier. At the same time, the government revised its fourth quarter 2018 estimate from 2.5 to 2.9 percent. Based on that encouragement, Fannie Mae has held steady, revising its full year estimate down only 0.1 percent.

Fundamentals remain strong and fiscal stimulus from the tax cut and new federal budget is expected to boost demand. The downside risks to growth foreseen by Fannie Mae include Treasury Secretary Mnuchin's concession that there is the "potential of a trade war" amidst the current heated rhetoric with China over tariffs.

If the threats and counter-threats on trade continue, the economists say, they could lead to a significant loss in consumer and business confidence. If the U.S. actually deploys trade restrictions and China retaliates with reciprocal tariffs, a reduction in its Treasury holdings, or other actions, "the trade war could reverse much of the positive impacts of the fiscal stimulus or could trigger an even worse outcome-recession."

The Federal Reserve remains optimistic about economic growth and employment and its view on inflation is unchanged. Its favorite measure of the latter, the Personal Consumption Expenditures (PCE) deflator- picked up to 1.8 percent after holding at 1.7 percent for three consecutive months. With inflation trending up toward the Fed's target amid continued labor market improvements, Fannie Mae expects the Fed to raise interest rates for the second time this year in June and then once more before the end of the year. This is a revision of their earlier thinking that there could be a fourth hike and given the dangers regarding trade protectionism that have emerged since the last forecast, they are even hedging their bets about hike number three.

Based on recent history, the authors don't find the slowdown in the first quarter at all alarming. Since the end of the recession, growth in the first quarter has consistently slowed compared to the last quarter of the previous year then has strengthened during the remaining three quarters. Between 2010 and 2017, the GDP increased an annualized average of 1.2 percent in the first quarter, at least one percentage point below the average growth in the next three quarters. Fannie Mae expects that pattern to hold this year.

Early data indicates that real residential investment declined during the first quarter after strong 12.8 percent annualized growth in the fourth quarter of 2017. New home sales were down for the third straight month in February while existing home sales rose, but not quite enough to offset their January drop. Total sales - new and existing - were flat in January and February when compared with that same period last year.

Total housing starts were down in February and nominal residential construction spending was up only slightly during the first two months of the year. The main home price indices - those from Case-Shiller, CoreLogic, and the Federal Housing Finance Agency - continued to show strong annual gains ranging from 6.1 percent to 7.3 percent in January.

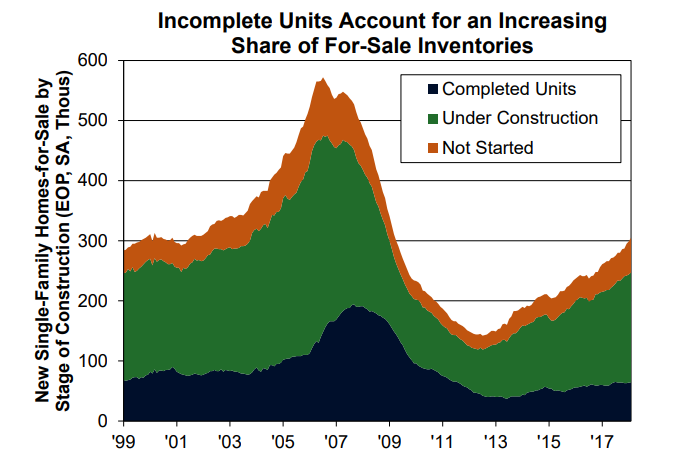

The near-term outlook for home sales is mixed. Despite the rebound in pending home sales in February, purchase mortgage applications fell sharply, and only partially recovered in March. Fannie Mae still expects an increase of 3 percent in total home sales in 2018. The inventory of existing homes for sale is still declining on an annual basis and, while the number of new homes for sale has continued to trend up, the increase has been concentrated in incomplete units. Ongoing tightness in the inventory of completed new homes for sale will probably continue to restrain sales.

The company's mortgage rate and mortgage volume forecasts for 2018 are essentially the same as in March. Total mortgage originations are expected to fall about 8 percent from 2017 to $1.69 trillion in 2018, with a refinance share of 29 percent, nearly 10 percentage points below the share in 2017.

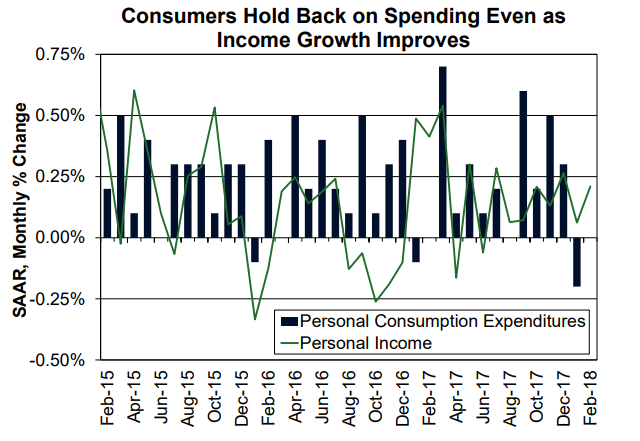

There were a few other interesting nuggets in the Fannie Mae's forecast. Consumer spending was seen as unsustainable in the fourth quarter, largely because of demand for autos to replace those damaged in the two fall hurricanes but the decline in the first quarter was worse than expected. This was especially notable since both real and nominal personal income growth rose. Thus, the savings rate rose, up two-tenths to 3.4 percent. Consumer spending should improve in March as tax refunds has caught up to historical norms and the new tax rates are showing up in payroll withholding.

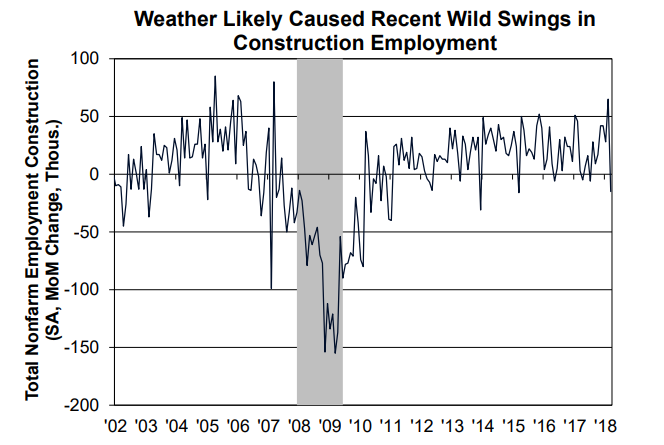

Labor market conditions joined into the overall volatility in March, with 103,000 new jobs, the worst showing since last September. Weather may have played a role as the swings were evident in weather sensitive industries like construction where employment fell by 15,000, the largest drop in three years.