Every foreclosure related report that issued during the last few months has increased certainty that the millions of delinquencies and foreclosures the country plaguing the country for the last three years are finally beginning to clear the system.

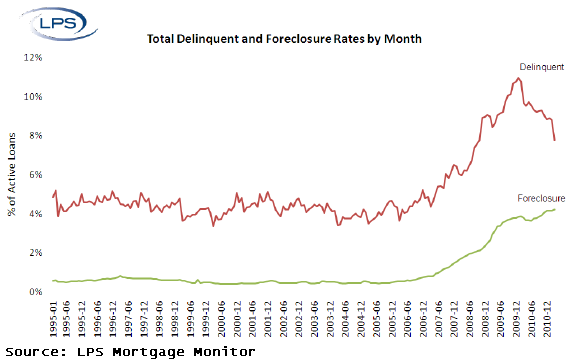

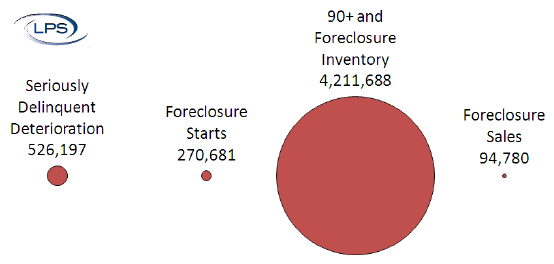

The Mortgage Monitor Report released by Lender Processing Services, Inc. (LPS) on Tuesday provides further evidence that delinquencies are down and the pace of foreclosures is picking up after months of moratoria, retrenching and procedure reviews. At the same time, at the end of March, the inventory of foreclosures (loans referred to an attorney and awaiting auction or repossession) hit an all-time high and foreclosure starts soared by one-third. The foreclosure inventory is 2.2 million loans and the foreclosure rate stands at 4.2 percent.

Delinquencies decreased from February to March by 11 percent, reaching the lowest levels in three years and were down nearly 20 percent from the same figure one year earlier. Even better news is the drop in early stage delinquencies with numbers of 30-day and 60-day delinquencies approaching pre-crisis levels. Part of this is seasonal; the first quarter of virtually every year shows a drop in new delinquencies, and historically March is consistently the month with the largest declines. Still, from February 1 to March 31 there was a drop of close to 463,000 delinquent loans in the 30 + and 60+ category for a total of 2,121,352 early delinquencies. The overall delinquency rate now stands at 7.78 percent.

The rise in foreclosure inventory and decrease in delinquencies over the last six months have affected all loan types. The most dramatic drop in delinquencies has been in Agency Prime Mortgages. Delinquencies have declined by about 20 percent to a current rate of 4%. FHA/VA loan delinquencies dropped about 16 percent to 9.6 percent and subprime loan delinquencies while still standing at a 27.1 declined 15 percent.Foreclosures on borrowers with an option ARM loans have increased by 20 percent in the last six months to a 19 percent rate. Foreclosures of non-Agency Conforming Prime loans were up about 17 percent to 4.4 percent and Subprime loans increased 16 percent to 15.2 percent.

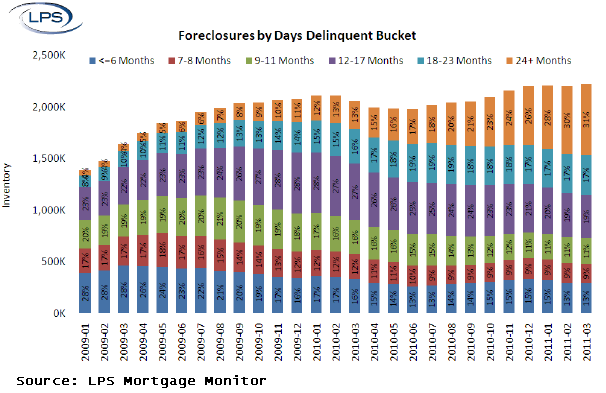

A foreclosure was initiated against about 250,000 loans in March an increase of about 25 percent month-over-month. The biggest jump in foreclosure starts was among loans that were six months or more in arrears. Both statistics indicate that the delays in foreclosures caused by problems with loan documentation have ended and loans will begin to move more rapidly toward resolution. Foreclosure sales also bumped up to 95,000 during the month but remain far below the levels before the robo-signing scandal jammed up the system.

LPS refers to the foreclosure pipeline as "bloated." Foreclosures sales are outnumbered by foreclosure starts three to one and by loans in foreclosure 30 to one. Loans that are 90+ delinquent combined with the foreclosure inventory outnumber sales 45 to one.

Despite the recent pick-up in foreclosure starts and sales, loans still remain in a delinquent status for an extraordinary period of time. In eight states and the District of Columbia the process averages over a year, taking an average of 444 days in New York, a judicial foreclosure state and 419 days in DC, a non-judicial region. South Dakota, with a judicial process, averages 219 days to foreclosure, the fastest in the country.

The states with the highest percentage of non-current loans are Florida, Nevada, Mississippi, New Jersey, and Georgia.

The post-crisis vintage of new mortgages continues to hold

up well. Loans originated in 2005 were

running about a 5 percent delinquency rate at the point where 24 payments

should have been received. At that same

point the 2009 vintage is at about 3 percent.

The most recent loans, originated in 2010, looks even better; at 14

months the delinquency rate is about 1.5 percent compared to 2 percent for the

2009 loans and well over 3 percent for those originated in 2005.

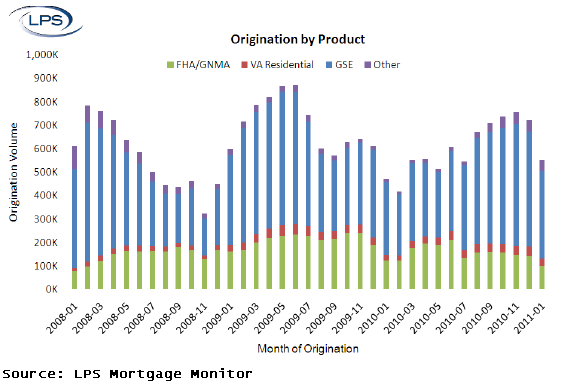

The report also found that mortgage origination activity continues to be dampened,

primarily due to an ongoing reduction in refinance activity. As interest rates

rise and credit requirements remain more exacting, the majority of homeowners

eligible to refinance may have already done so.

Housing Scorecard: Delinquencies Down. Foreclosures Delayed

Foreclosure Filings Drop. Prevention Policies Distorting Supply and Demand

LPS Data Shows Long Delays in Foreclosure Process