The Mortgage Bankers Association (MBA) today released its Weekly Mortgage Applications Survey for the week ending May 6, 2011.

The MBA's loan application survey covers over 50% of all U.S. residential mortgage loan applications taken by mortgage bankers, commercial banks, and thrifts. The data gives economists a snapshot view of consumer demand for mortgage loans. In a falling mortgage rate environment, a trend of increasing refinance applications implies consumers are seeking out lower monthly payments. If consumers are able to reduce their monthly mortgage payment and increase disposable income through refinancing, it can be a positive for the economy as a whole (may boost consumer spending. It also allows debtors to pay down personal liabilities faster. A trend of declining purchase applications implies home buyer demand is shrinking.

Excerpts from the Release...

The Market Composite Index, a measure of mortgage loan application volume, increased 8.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 8.3 percent compared with the previous week. The four week moving average for the seasonally adjusted Market Index is up 2.9 percent.

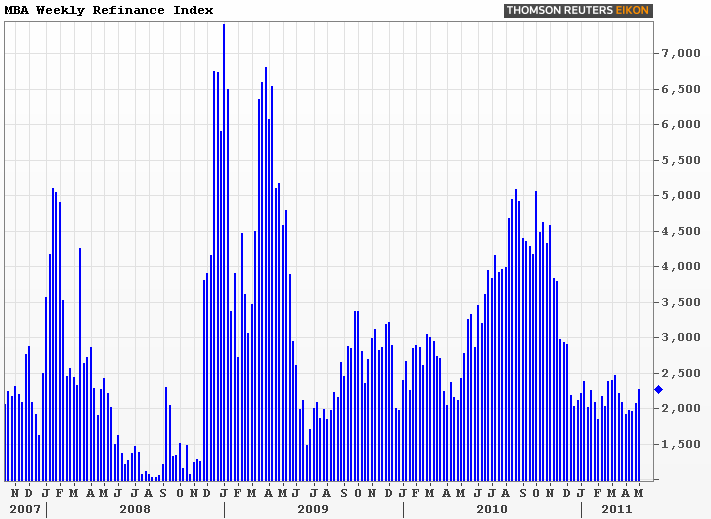

The Refinance Index increased 9.0 percent from the previous week, and is at its highest level since the week ending March 18, 2011. The four week moving average is up 4.3 percent for the Refinance Index. The refinance share of mortgage activity increased to 63.1 percent of total applications from 62.7 percent the previous week. The refinance share is at its highest level since the week ending March 25, 2011.

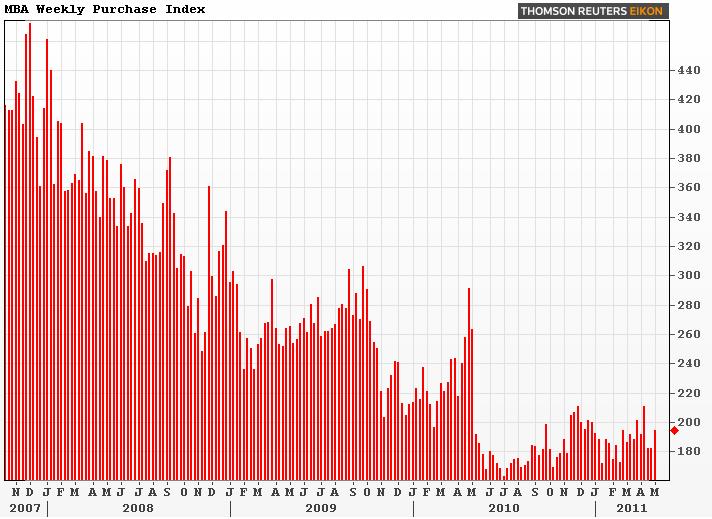

The seasonally adjusted Purchase Index increased 6.7 percent from one week earlier. The unadjusted Purchase Index increased 7.1 percent compared with the previous week and was 25.8 percent lower than the same week one year ago. The four week moving average is up 0.4 percent for the seasonally adjusted Purchase Index.

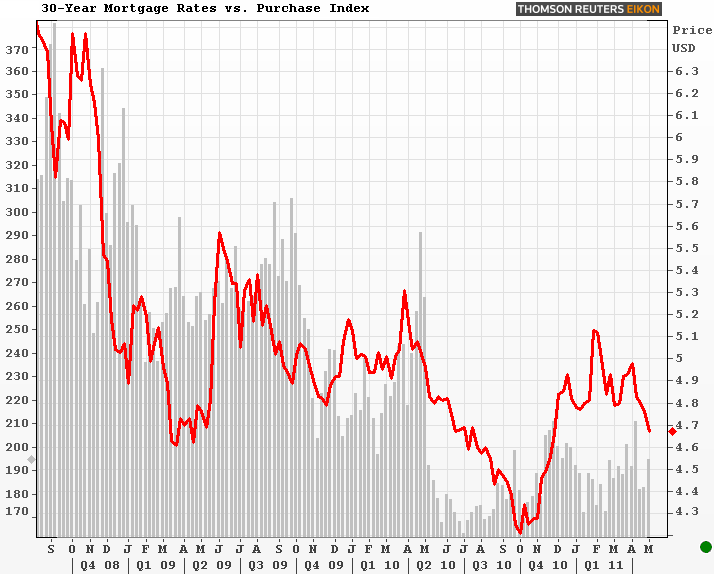

The average contract interest rate for 30-year fixed-rate mortgages decreased to 4.67 percent from 4.76 percent, with points increasing to 1.10 from 0.75 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans. The 30-year rate is at its lowest since December 2010. The effective rate also decreased from last week.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 3.81 percent from 3.96 percent, with points increasing to 1.05 from 0.82 (including the origination fee) for 80 percent LTV loans. The 15-year rate is at its lowest since November 2010. The effective rate also decreased from last week.

The adjustable-rate mortgage (ARM) share of activity decreased to 6.5 percent from 6.7 percent of total applications from the previous week.

"Rates dropped again last week as the Federal Reserve continued its QE2 asset purchase program. The 30-year fixed mortgage rate is now 46 basis points below its 2011 peak, and has decreased for four straight weeks by a total of 31 basis points," said Michael Fratantoni, MBA's Vice President of Research. "Over this four week span, the refinance index has increased by about 18 percent. Despite the recent increases however, refinance application volumes remain more than 50 percent below levels seen last fall."

Re: The logic behind falling interest rates. Although the Fed's daily asset purchases have indeed been supportive of lower benchmark yields, there are big picture factors to consider in the directional move we've witnessed over the past month. Expansion in the global economy seems to be slowing and investors are acting increasingly nervous about their allocation choices. If it is confirmed that emerging economies have hit a rough patch, the impact of such a slowdown would spread through the U.S. economy starting with the manufacturing sector. This would be a favorable development for interest rates and serve as a reminder of how sensitive our economic recovery really is in the long run. Going full circle on Michael Fratantoni's comment on Fed asset purchases, the Federal Reserve is scheduled to complete its quantitative easing (QE) program by the end of June. If the economy does indeed slide for the worse and the Fed does not decide to re-up its QE program, it may actually lead interest rates lower as the broader economy suffers from reduced liquidity in financial markets.

Re: The refinance index being slow to react to falling mortgage rates. WE AGREE!

Would significantly lower interest rates spark an increase in loan demand?

We think 30-year fixed mortgage rates need to approach 4.25% before a sizable uptick in refinance demand is observed. On the buyer front, since early February we've heard reports from originators about a seasonal increase in purchase loan demand, since then purchase business seems to have slowed. Falling rates will certainly increase affordability conditions though, which helps offset the notion that home prices have more room to run lower. If you're looking to buy, be sure to access local market conditions with not only your Realtor but an appraiser as well. And for Heaven's sake...maintain your reserves/savings just in case home prices keep falling.

The road ahead is long and paved with much uncertainty....the economic recovery will be choppy at best until the housing market is able to sustain consistent positive progress.