The National Association of Realtors® (NAR) released its April Pending Home Sales Index (PHSI) today. The index is said to be a leading indicator for the housing sector; it measures sales activity based on sales of single-family homes, coops and condos. The data reflects contracts but not closings, which normally occur with a lag time of one or two months.

Pending home sales fell in April with regional variations following increases in February and March, with unusual weather and economic softness adding to ongoing problems that are hobbling a recovery, according to the National Association of Realtors®. This is a reversal from the March Pending Home Sales report which indicated momentum was beginning to build as the summer months approached. WATCH THE VIDEO

Reuters Quick Recap...

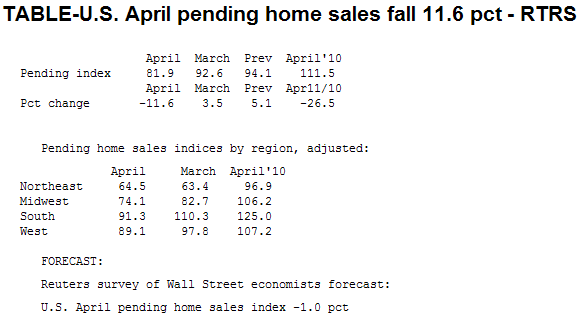

RTRS - U.S. APRIL PENDING HOME SALES INDEX -11.6 PCT (CONSENSUS -1.0 PCT) TO 81.9

RTRS - U.S. APRIL PENDING HOME SALES -26.5 PCT FROM APRIL 2010

Excerpts from the Release....

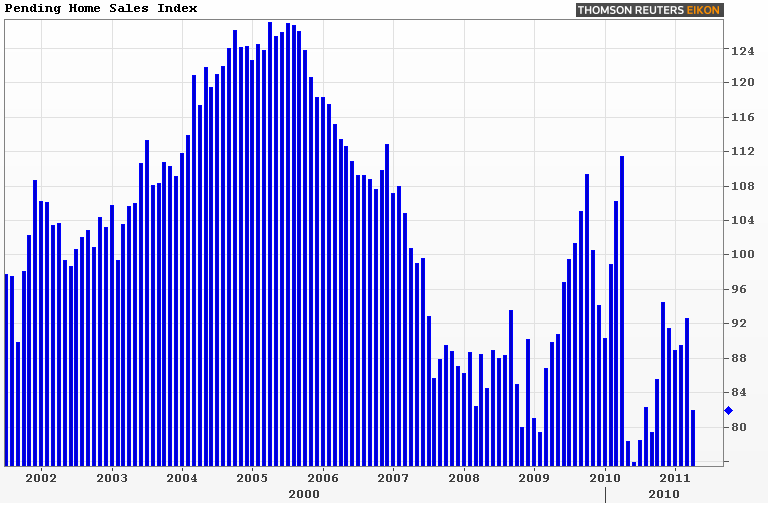

The Pending Home Sales Index, a forward-looking indicator based on contract signings, dropped 11.6 percent to 81.9 in April from a downwardly revised 92.6 in March. The index is 26.5 percent below a cyclical peak of 111.5 in April 2010 when buyers were rushing to beat the contract deadline for the home buyer tax credit.

The PHSI in the Northeast rose 1.7 percent to 64.5 in April but is 33.4 percent below a year ago. In the Midwest the index fell 10.4 percent to 74.1 and is 30.2 percent below April 2010. Pending home sales in the South dropped 17.2 percent to an index of 91.3 in April and are 27.0 percent below a year ago. In the West the index declined 8.9 percent to 89.1 and is 16.9 percent below April 2010.

Lawrence Yun, NAR chief economist, said the dip in contracts may be due

to temporary factors. “The pullback in contract signings is

disappointing and implies a slower than expected market recovery in

upcoming months,” he said. “The economy hit a soft patch in April from

sharply rising oil prices, widespread severe weather with the heaviest

precipitation in 20 years, and a sudden rise in unemployment claims.”

Yun notes the growth in retail sales slowed measurably in April, while sales at furniture and home furnishing stores declined sharply. “Nonetheless, the magnitude of the fall in pending home sales is larger than can be implied by broad economic factors, so we need to see if it’s just a one-month aberration.”

Yun said tight credit is the primary long-term factor holding back the market. “No doubt the continuing excessively tight mortgage underwriting process is making the housing market recovery unnecessarily slow,” he said. “Lenders and bank regulators need to be mindful of the historically low default rates among mortgage borrowers of the past two years. A robust economic and housing market recovery cannot occur as long as banks continue to hold onto huge cash reserves.”

“We simply have to get back to sound, common-sense lending standards to provide mortgages to creditworthy borrowers who are buying homes well within their means. Bank balance sheets show rising cash reserves and declining loan balances – it’s time to loosen the purse strings,” Yun added.

“Even with very favorable affordability conditions, job growth and a pent-up demand from abnormally low household formation during the past three years, the recovery will continue to be uneven and sluggish given the ongoing credit constraints,” Yun said.