The June edition of the Obama Administration's Housing Scorecard released on Friday showed that housing prices turned slightly upward while mortgage defaults continued to fall as have the numbers of completed foreclosures and short sales. However, the aggregate equity of American homeowners also declined.

According to the Scorecard, a joint report by the Departments of Housing and Urban Development (HUD) and Treasury, in May, 4.3 percent of prime mortgages were at least 30 days late - a significant decline from the peak of 5.9 percent seen in 2010. Moreover, seriously delinquent prime mortgages - those at least 90 days late or in foreclosure - dropped by 22 percent from a high of 1.9 million recorded last year. As new delinquencies decrease across the nation, the number of new homeowners seeking assistance through the Administration's programs may also decrease.

All three of the indices of home prices included in the scorecard, Case-Shiller, Core-Logic, and FHFA - increased slightly with Core-Logic showing the largest increase - 2.7 points. At the same time aggregate home equity declined by $271 billion since the previous report. The sales of both new and existing homes decreased, however the inventory of new homes declined slightly to a 6.2 month supply from 6.3 months. The inventory of existing homes rose from 9.0 months to 9.3 months. The supply of vacant homes held off of the market continues to increase and now totals 3,861,000 compared to 3,602,000 in the previous quarter.

"The housing data in this month's Scorecard paint a mixed picture of the housing market, despite growing evidence of progress in the broader economy," said HUD Assistant Secretary Raphael Bostic. "Last month we saw a slight uptick in home prices and a continued decline in mortgage defaults as our foreclosure prevention programs reach more borrowers upstream in the process. But we have much more work to do to reach the many households who still face trouble and to help the market recover. That is why this Administration continues to push for effective implementation of our recovery programs as we continue to help homeowners through this crisis."

The Scorecard includes by reference the monthly report on the administration's programs to assist homeowners who are delinquent on their mortgages, principally the Home Affordable Modification Program (HAMP). This report has increasingly focused on the performance of mortgage servicers who have been widely blamed for HAMP's less than optimum results. Last month HUD announced that all ten of the major servicers administrating the program had failed to live up to performance standards and withheld incentives from three of the largest firms. FULL STORY

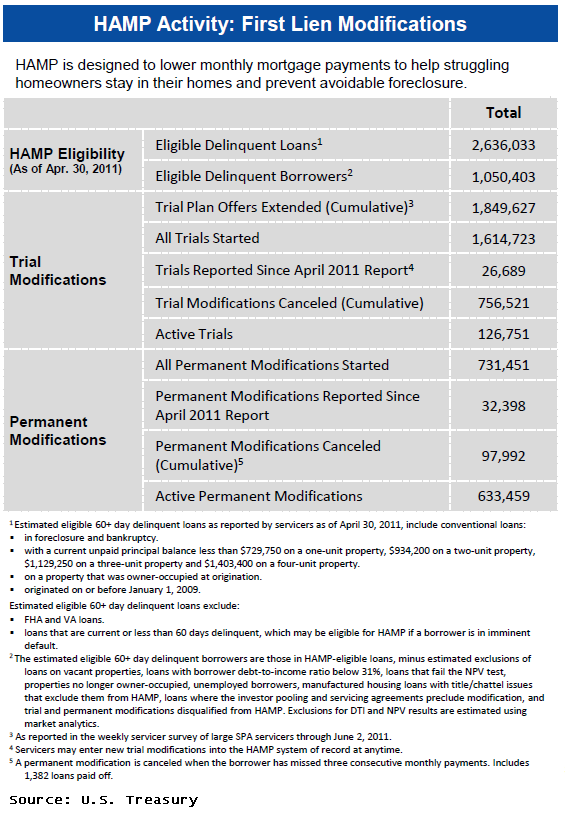

During the reporting period 32,398 loans were converted from trial modification status to permanent status bringing the total to 731,451 since the program began; 633,459 of the permanent modifications are still in force. A total of 1,614,723 trail modifications were initiated since the program started in April 2009 and 126,751 borrowers remain in trial modifications. Since the last report 26,689 borrowers have entered into trials.

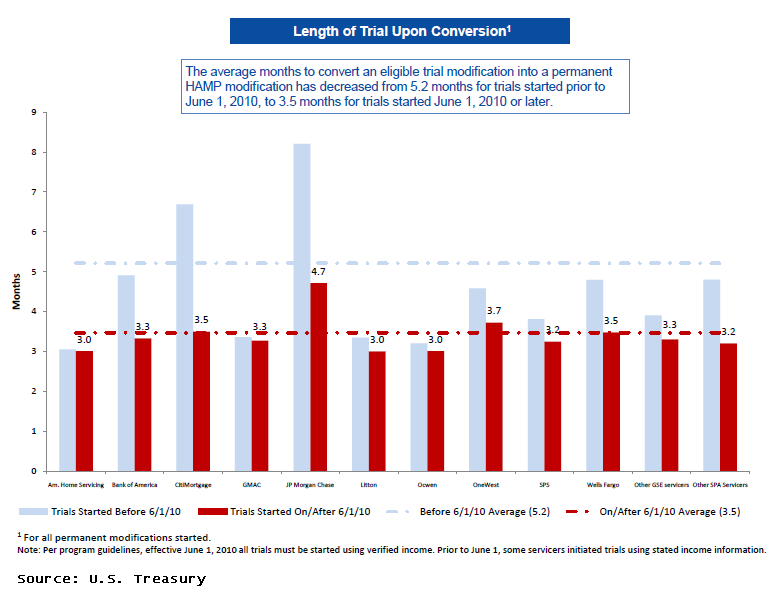

The average trial modification period for loans entering modification when borrowers were required to provide verified income information upfront, is 3.5 months. Those loans entering into modifications prior to June 1, 2010 had an average trial period of 5.2 months. It is interesting to note that, on the graph below showing the average length of trials, two of the largest servicers were most responsible for that 5.2 month average. CitiMortgage and JPMorgan Chase had average trial periods averaging longer than 5 months while all other principal servicers had average trial periods of less than 5 months.

All servicers have improved conversion timelines since June 1, 2010.

Before the change in documentation requirements in June 2010 the average conversion to permanent status was 42 percent. It is now 71 percent with another 20 percent of loans currently pending processing or a decision on conversion. Two servicers, Bank of America and JPMorgan Chase lag the others dramatically with conversion rates of 55 percent and 63 percent.

Not all 60+ day delinquent loans are eligible for HAMP. Based on the estimates, of the 4.6 million homeowners who are currently 60+ days delinquent, 1.05 million homeowners are eligible for HAMP. As this represents a point-in-time snapshot of the delinquency population and estimated HAMP eligibility, Treasury expects that more homeowners will become seriously delinquent between now and the end of 2012, and some of those homeowners will be eligible for HAMP.

Estimated eligible 60+ day delinquent loans as reported by servicers as of April 30, 2011, include conventional loans:

- in foreclosure and bankruptcy.

- with a current unpaid principal balance less than $729,750 on a one-unit property, $934,200 on a two-unit property, $1,129,250 on a three-unit property and $1,403,400 on a four-unit property.

- on a property that was owner-occupied at origination.

- originated on or before January 1, 2009.

Estimated eligible 60+ day delinquent loans exclude:

- FHA and VA loans.

- loans that are current or less than 60 days delinquent, which may be eligible for HAMP if a borrower is in imminent default

Second liens have interfered with the modification of many senior liens and the administration has recently focused on eliminating this obstacle. The Second Lien Modification Program (2MP) has now resulted in 27,105 second lien modifications, 19,000 of these in the last four months. In some cases these modifications have resulted in full extinguishment of the subordinate debt.

The current HAMP report also includes information on two other programs. The Principal Reduction Alternative (PRA) requires servicers of non-GSE loans to evaluate the benefit of principal reduction where mortgages have a loan-to-value ratio of 115 percent or more. They are not, however, required to reduce principal as part of a modification. There have been 21,299 PRA modifications begun with 4,938 modifications now permanent. The median principal reduction in permanent modifications is $69,532, or 32.2 percent of the loan balance.

The second initiative, Home Affordable Foreclosure Alternatives (HAFA) offers incentives to homeowners seeking a short sale or to give a deed-in-lieu of foreclosure. There have been 17,781 HAFA agreements started with 8,541 completed. Of these 8,309 were short sales and 232 were deeds-in lieu.

"The Administration remains committed to reaching homeowners who are still struggling so that our country can fully recover from an unprecedented housing crisis," said Treasury Assistant Secretary for Financial Stability Tim Massad. "The Administration's programs continue to benefit tens of thousands of additional homeowners every month, while keeping the pressure on mortgage servicers to offer more sustainable assistance to prevent avoidable foreclosures."