Black Knight's current Mortgage Monitor notes that refinances are increasingly being driven by a cash-out rather than interest rate motives both because home prices have so substantially increased household equity - tappable equity now is estimated at $5 trillion - and rates have trended higher. In a separate section of the Monitor, Black Knight merges that discussion with an analysis of the current pattern for mortgage prepayments.

Refinancing overall had a tough first quarter in 2017, falling by 45 percent compared to the fourth quarter of 2016, but largely unanticipated decline of rates starting in March may have breathed new life into that activity. However, there is another part to the story.

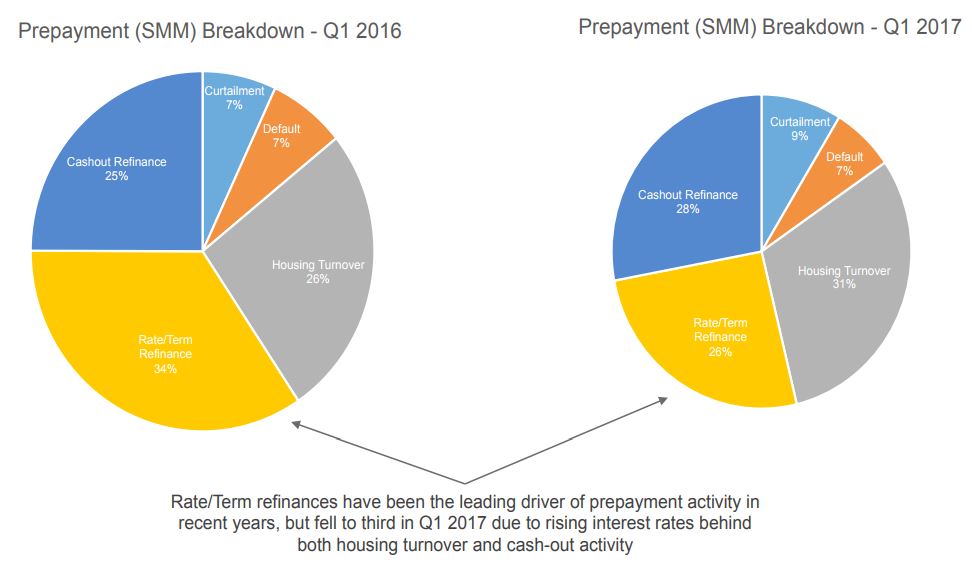

While rate/term refinancing declined over 30 percent between the first quarter of 2016 and the same quarter in 2017, the average prepayment or SMM rate, generally viewed as a vector for refinancing, dropped by only 10 percent over the same period. Curtailments (early payoffs or paydowns of mortgage balances) pre-payments related to housing turnover (sales) , and via cash-out refinances actually increased. Then in May of this year, the SMM rate hit a calendar year high. It could go even higher, Black Knight says, if rates remain at current levels.

The growth of these reasons behind prepayment have not only impacted overall volume, it has changed the composition of prepayments and alters the way investors and analysts should monitor prepayment activity. Rate/term refinancing is now third among the reasons for prepayment, (ahead of only curtailments) even as purchase mortgage applications, which would indicate housing turnover, are at the calendar year low. This situation is not likely to continue for long, but it provides a view of what the market may look like when interest rates rise in the future and shows the importance of accurately incorporating equity-drive prepayment risk in any prepayment models.

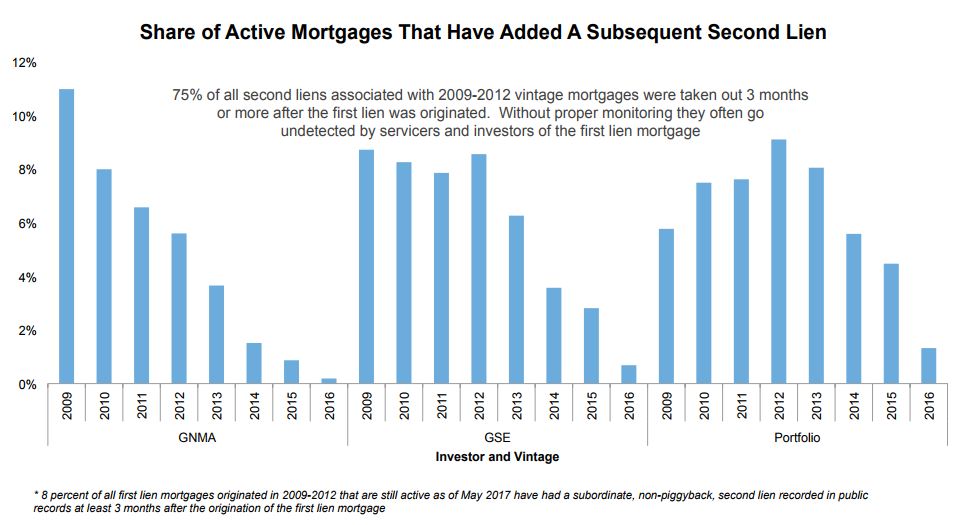

Black Knight also notes that, even though loans originated since 2009 are considered among the safest in decades, many already carry some "second lien risk." This is especially true of portfolio loans and those backed by Fannie Mae and Freddie Mac. Adding a second lien post origination can significantly alter first lien performance, the company says.

Nearly 11 percent of loans originated between 2009 and 2012 already carry a second lien. Unlike pre-crisis loans where nearly two-thirds of such liens were piggy backs taken out at the same time as first mortgage origination, the most recent loans were largely (75 percent) taken out more than three months after the first mortgage closed, making it difficult for servicers and investors to identify.

Black Knight also notes that the growing tappable equity that is driving the cash-out refinance boom also presents some portfolio risks, especially for those properties with mortgages originated post crisis, many of which carry very low interest rates. The share of homeowners that are taking out second mortgages has risen each year since 2009 and that trend can be expected to continue as equity grows. The growth may accelerate if rising interest rates incentivize homeowners to tap equity through a HELOC rather than refinancing out of their existing low-interest first mortgage.