The single agency security toward which the GSEs, Fannie Mae and Freddie Mac and their regulator, the Federal Housing Finance Agency (FHFA), have been working for several years, is not yet operative, but it just got a round of applause. Linda Goodman, Codirector of the Urban Institute's (UI's) Housing Finance Policy Center, and associates Bing Bai and Jim Parrot, writing in UI's Housing Wire blog say the new security will save taxpayers millions of dollars while making the market more responsive to borrowers and lenders.

The GSE's have each issued their own mortgage-backed security for more than four decades but the securities issued by Freddie Mac have historically traded at a lower price than those issued by Fannie Mae. A subsidy was often required to equalize pricing so originators would put their loans in Freddie's security pools and assure that company retained an adequate market share. The subsidy cost taxpayers as much as $1 billion a year. FHFA proposed the single security to overcome the pricing disparity.

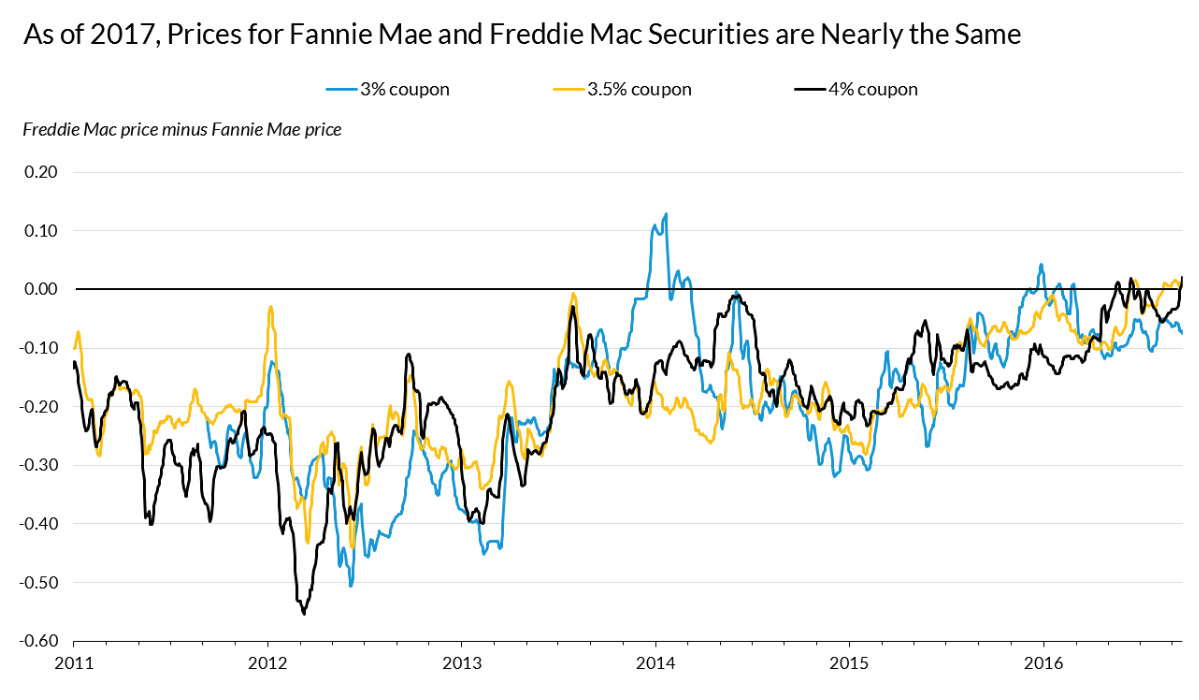

Apparently it worked, even without being operational. The authors say, once the security effort began, the disparity all but disappeared. The 0.30 discount at which three of Freddie's coupons traded relative to Fannie's in 2012 and 2013 narrowed to around 0.15 by 2014-2015 and had nearly disappeared by early this year.

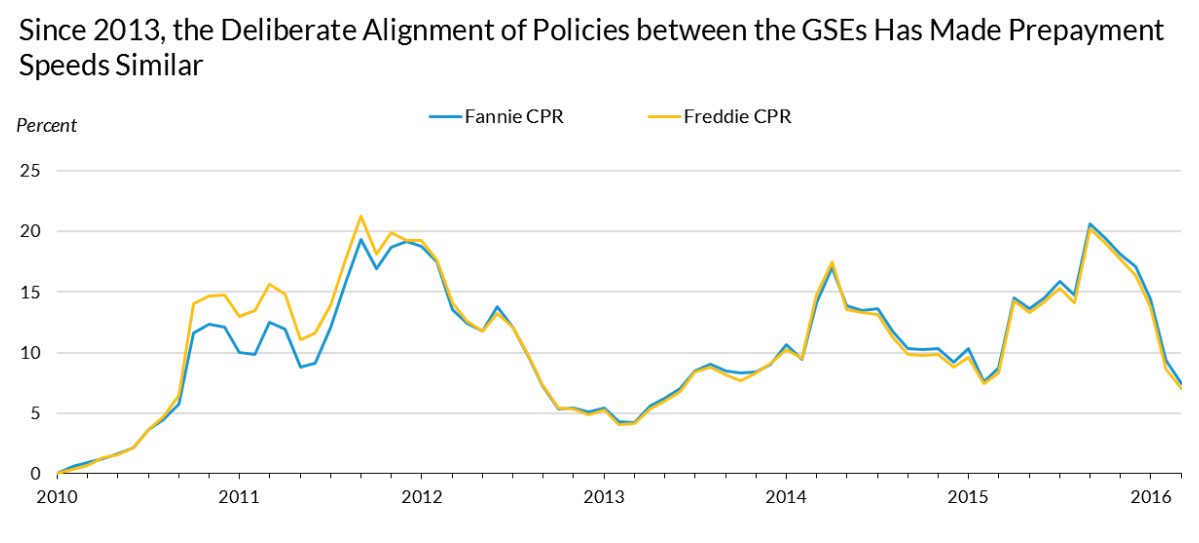

It seems operational factors and anticipation may have done as much to eliminate the disparity as actually issuing the security. Freddie Mac usually had prepayment speeds that were faster than Fannie Mae's, reflecting a different issuer mix and differences in their streamlined modification programs. But FHFA's insistence on aligning the operational policies of the GSEs put prepayment speeds on the same track. The price convergence also reflects that the market anticipated that the single security, announced several years ago, would become a reality.

So why would FHFA and the GSEs bother moving to a single security if the problem has disappeared? Goodman, et al say the convergence is not sustainable in its absence. Part of the disparity is due to the lower liquidity of Freddie Mac which still exists, so if that is not addressed and the perception that the single security will become reality disappears, the pricing disparity will almost certainly return.

The merging of the two price points was necessary before the single security could work smoothly. The GSEs will continue to issue their individual securities but both can also issue into Fannie Mae Mega Pools, Freddie Mac Giant pools and real estate mortgage investment conduits (REMICs) for each. For this the securities need to be fungible, something the market recognizes and has begun pricing into their investments.

Freddie Mac is already using the Common Securitization Platform (CSP) which is a joint venture of the GSEs and from which the new security will be issued. Fannie Mae is expected to convert to it in the second quarter of 2019 at which point the single security will go live.

There are remaining considerations to be addressed such as conversion of existing Freddie Mac securities to the new issue and how that switch will be actuated and treated for tax purposes. A host of questions also remain regarding regulatory handling of limitations on concentrations on one or the other security, given their fungibility. None of these concerns, the authors say, are sufficiently large to hold up the new security.

They conclude, "The bottom line, though, is that progress toward a major development in the secondary mortgage market is under way. This will be a significant achievement, making the market more responsive to borrower and lender needs, boosting competition, and increasing the availability of mortgage credit."

Co-author Parrott, a non-resident scholar at UI, has also completed an analysis of the CSP. We will summarize it in a subsequent article.