The Federal Housing Finance Agency (FHFA), conservator for Freddie Mac and Fannie Mae (the Enterprises) said on Thursday that, while modifications of loans tied to the Enterprises declined in the second quarter of 2011, those modifications continue to be robust. Voluntary home forfeiture actions, both short sales and deeds-in-lieu of foreclosure increased as did the pace of REO disposition.

The Foreclosure Prevention and Refinance Report issued by FHFA includes actions taken on Enterprise loans under both the Home Affordable Modification Program (HAMP) and the Home Affordable Refinance Program (HARP). According to the report, loans modified under HAMP continue to perform better than historical data would indicate.

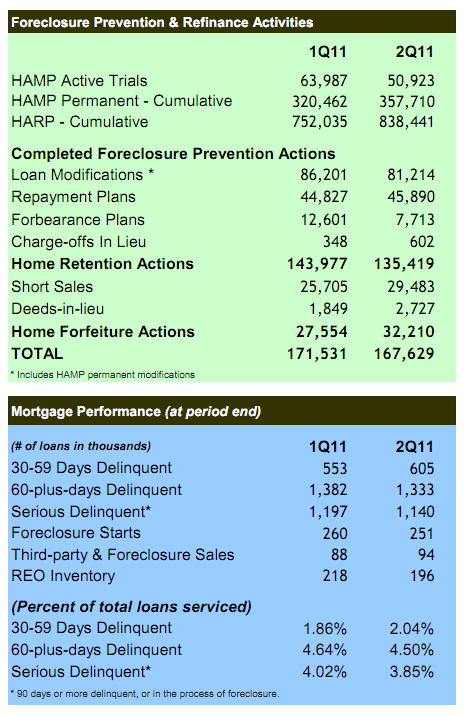

During the second quarter, 135,419 home retention actions were completed on Enterprise loans compared to 143,977 in Quarter One. This included 81,214 loan modifications, down from 86,201; 45,890 repayment plans - almost a thousand more than in the previous quarter - and 7,713 forbearance plans, down from 12,601 in Q1. There were also 602 "charge-offs in lieu," almost double the earlier activity. Broken down by Enterprise, 50,043 of the modifications were Fannie Mae loans compared to 50,043 in Q1 and 30,878 were Freddie Mac loans, down from 35,158.

During the second quarter 59 percent of loans modified received a both a term extension and a rate reduction, 9 percent received only a term extension and 30 percent received only a rate reduction. These figures have varied only one or two percentage points over the last four quarters.

Almost half of the Enterprise loans modified during the second quarter received a payment reduction of 30 percent or more. This number has remained fairly consistent over the last three quarters while the percentages receiving decreases of 1 to 30 percent has steadily increased and is now at 44 percent. The percentage of homeowners seeing no change or an increase in payments has shrunk to around 7 percent. In the three quarters leading up to the implementation of HAMP, (Q1, 2, and 3 of 2008) most loans that were "modified" actually ended up with payment increases. This was the case with 82 percent, 70 percent, and 53 percent respectively of the loans modified in those quarters.

Fannie Mae's borrowers have fared slightly better under HAMP than Freddie Mac's over the last few quarters. Sixty-two percent of its borrowers received both an extension of term and a rate reduction compared to 54 percent of Freddie Mac's borrowers and 32 percent of its borrowers received only a rate reduction compared to 28 percent of Freddie Mac borrowers. Freddie Mac was three times more likely (15 percent) than its sister Enterprise to only extend the term of the loan.

Fannie Mae was also more generous than Freddie Mac in the payment reductions it provided to borrowers. Fifty-four percent received payment reductions over 30 percent compared to 42 percent of Freddie Mac borrowers. Fannie Mae loans were reduced by less than 20 percent in 24 percent of cases; Freddie Mac in 28 percent. Payments were increased for 11 percent of Freddie Mac borrowers and 3 percent of Fannie Mae's.

Home forfeiture actions increased to 32,210 during the quarter, down from 27,554 in the earlier period. This included 2,727 deeds-in-lieu, up from 1,849 and 29,483 short sales, up from 25,705.

The Enterprises refinanced approximately 86,000 mortgages through HARP in the second quarter compared to 130,000 in Q1. This brings the cumulative number of refinances to 838,400 since the program began in 2009.

The enterprises' delinquency rates remain below industry standards with 3.85 of their loans considered seriously delinquent, down from 4.02 in the second quarter. Foreclosure starts declined from 260,000 to 251,000 quarter to quarter but early (30 to 59 days) delinquency increased from 1.86 percent to 2.04 percent.

The Enterprises acquired 78,485 properties during the quarter compared to 78,256 in Q1 and disposed of 100,550 compared to 94,441. At the end of June the inventory of real estate owned (REO) declined from 218,000 at the end of April to 196,000. Fannie Mae's inventory was down from 153,224 properties to 135,719 and Freddie Mac's declined to 60,599 from 54,159.

Eighty-four percent of the modified loans held by the Enterprises were current and performing after three months and 77 percent after six months. While the universe is limited, 73 percent were still performing after nine months. Despite the better terms given to Fannie Mae borrowers during modification, Freddie Mac borrowers were performing better at each of the benchmarks by one or two percentage points.