Whenever housing prices rise faster than the rate of inflation, the question arises, are we in a housing bubble? Two Urban Institute (UI) analysts, Bing Bai and Edward Golding, say rapidly growing prices can be benign when they are buoyed by fundamentals such as job and income growth, and are indications of an expanding economy. A bubble, on the other hand, is inflated by artificial or temporary factors. The latter kinds of price increases are often unsustainable and may come to no good end.

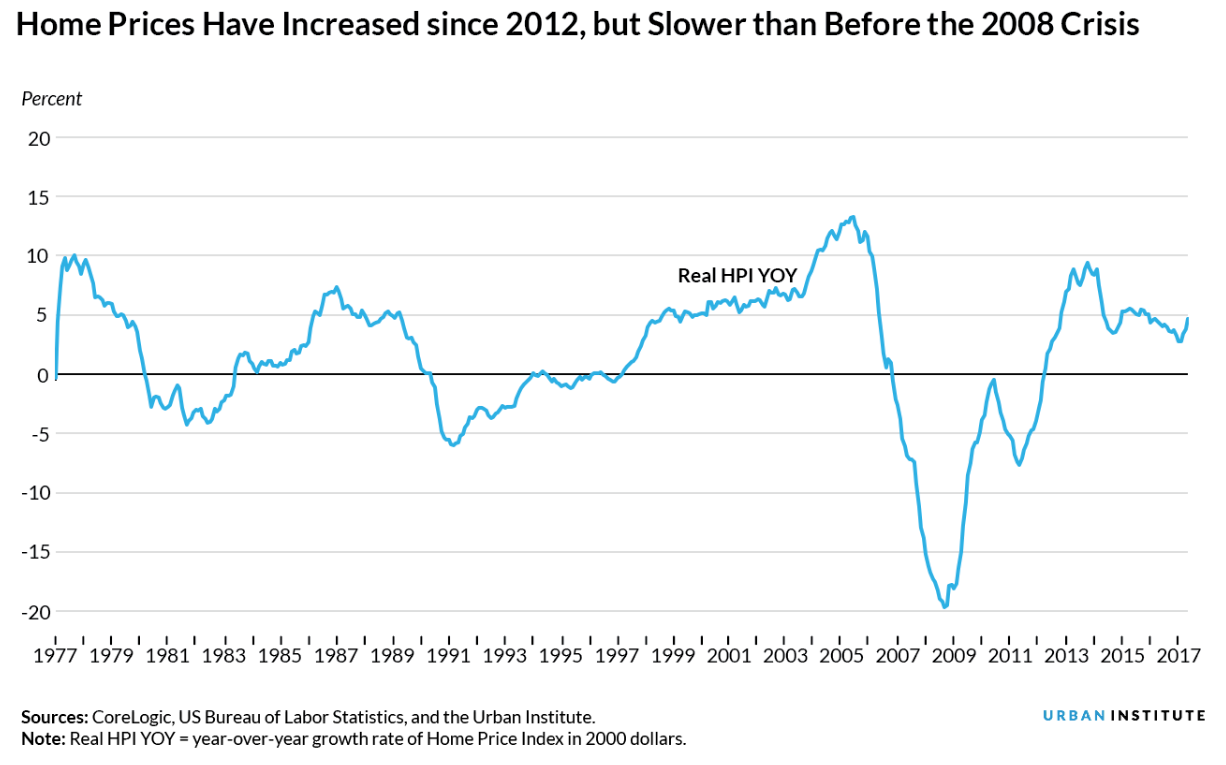

Appreciating home prices over the last five years have outpaced inflation by a cumulative 34 percent. While this is a significant difference, it is modest compared to the 87 percent difference between price growth and inflation in both 1997 and 2006. But, even if the differential is not yet alarming, the crucial question is whether those prices are driven by fundamentals or speculation.

The authors, writing in UI's blog, lay out two parameters for determining the sustainability of price increases. They conclude that the current rapid acceleration of home prices doesn't mean the nation as a whole is in a bubble, but certain metro areas do appear to be trending toward bubblicious.

Bai and Golding use the Housing Finance Policy Center's Housing Affordability Index which tracks whether the median household can afford a standard mortgage on a median-priced house. At present it indicates a median household can afford a home that costs $70,000 more than the actual median price of houses being sold, indicating that, even with the rising prices, homes remain affordable by national historic standards. Thus, price gains are probably tracking a broader economic expansion. Compare this to 2006, when there was a $22,000 shortfall between "affordable" and the median sales price. This indicates that we are not in a bubble nationally, and nowhere near the situation that preceded the 2008 housing crisis.

This is not the case however in some local markets. The authors looked at the 37 largest metropolitan statistical areas (MSAs) using the same key factors, affordability and the real increase in house prices since their lowest point after the crash. They summed the rankings and identified the MSAs most likely to be in a bubble, giving it a "bubble watch" rank.

The MSAs topping the list tend to have both strong price growth and low affordability. The San Francisco area, for example, has the fourth highest rate of appreciation and ranks at the bottom when it comes to affordability. Further down, the list the rank could be driven by price increases or by the lack of affordability.

Some of the effects of rapidly rising prices are mitigated on the bubble scale by where the MSA was pre-crash and where it landed afterward. For example, Las Vegas and Detroit have seen rapid price increases, but homes remain affordable. The opposite is true in Philadelphia, where prices have not gone up as much but are already unaffordable. To model these, one would need to account for the following factors:

- A lack of building that has constrained supply. With the exceptions of Detroit and Fort Worth, most of the 25 highest ranked metros have experienced shortages of housing supply in recent years.

- Some MSAs are rebounding from "overshooting" in the downturn. Detroit was already in decline before the last bubble and home prices didn't get much of a boost during it, increasing only 12 percent at the peak. The city then saw a major bust along with the rest of the nation; prices plunged 62 percent in the downturn. Since its trough, Detroit price gains have been the third fastest in the nation, still it remains one of the most affordable areas (ranked 23rd) and has the biggest gap between the two measures. Its number 14 bubble-watch rank is mostly driven by home price growth, while Phoenix, ranked about the same, has seen relatively rapid house price increases and limited affordability.

- International investors are buying houses in certain MSAs. International activity in the US residential market has been strong in recent years, and California, Florida, and Texas have been the favorites of foreign buyers. MSAs those three states rank high on the bubble-watch list.

- New nontraditional investors are buying houses as rentals. This may increase purchase prices and rental prices in ways that are unsustainable.

The authors say that keeping an eye on whether bubbling at the metro level is becoming unsustainable is an important consideration for public policy. It should be part of the discussion when the Federal Reserve mulls interest rates and states and localities should pay attention when they rethink building and land-use restrictions. Bai and Gooding say they intend to continue to refine their measures to better distinguish areas experiencing healthy and sustainable house price growth from those in bubble territory.