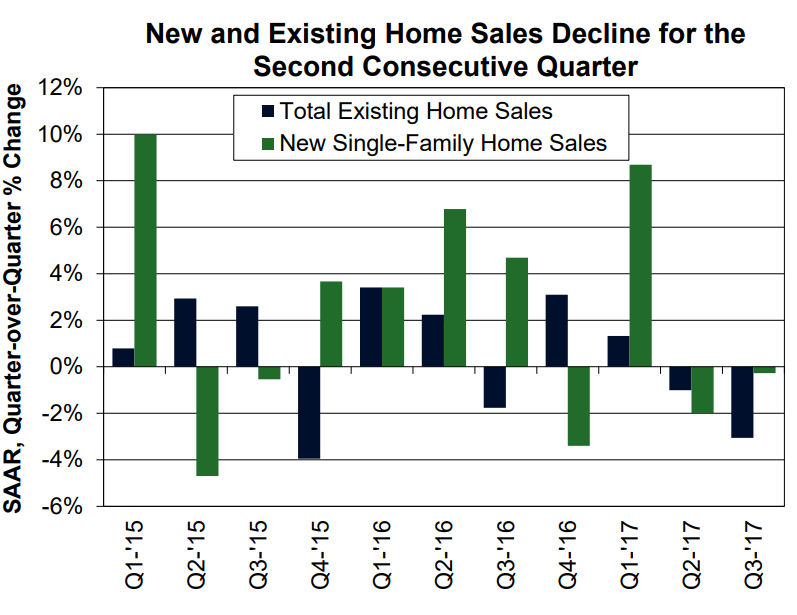

Housing activity in the third quarter of 2017 is described as "continuing its rough patch" in Fannie Mae's latest edition of Economic Developments. The company's economists say that activity pulled back across the board during the quarter. It was also the third in a row in which housing starts fell, although Friday's report on October residential construction signals a possible resurgence. New home sales were also down, despite an impressive 18.9 percent gain in September, a month in which existing home sales also rose for the first time in four months. The increase was not enough to bring the quarter into positive territory.

The economists note that, while "the hurricanes disrupted activity in the South, housing weakness was present before the hurricanes and largely stems from the supply side." Building activity has been constrained by shortages of labor and permitted land. Now building material prices have risen; framing and structural panel lumber prices are up 20 to 32 percent respectively from a year ago. The inventory of existing homes for sale is also a problem; it has declined on an annual basis for more than two years, with conditions unlikely to change in the near term.

The lean inventories, especially in the existing home market, continue to provide "a tailwind" to prices, hurting affordability and further constraining sales. The main measures of home prices show annual appreciation of more than 6 percent.

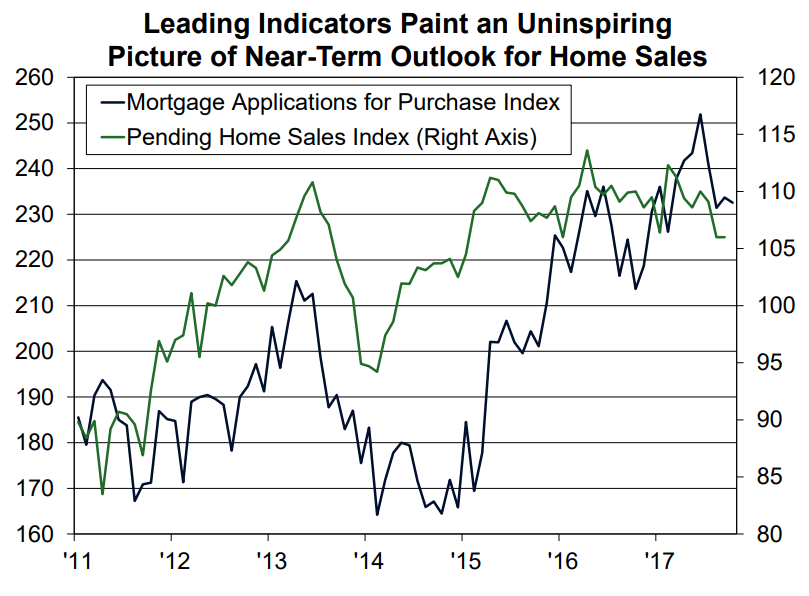

Leading indicators suggest that the rough patch demonstrated by third quarter numbers may be spilling into the fourth. Pending home sales, which are generally expected to predict sales of existing homes one or two months hence, were flat in September at the lowest level since January 2016. Contract signings have declined on an annual basis in five of the past six months. In addition, average monthly purchase mortgage applications fell in October for the third time in four months.

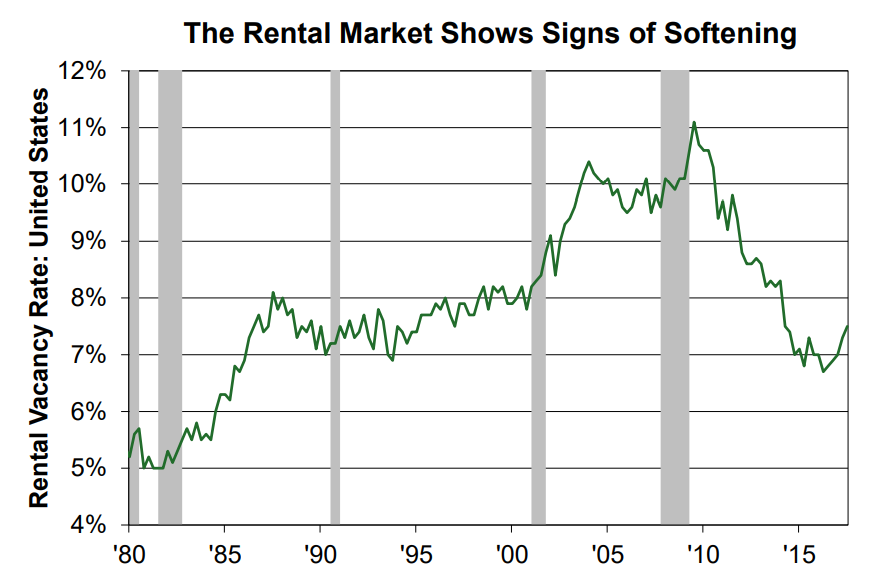

That the Census Bureau's homeownership rate increased year-over-year for the third consecutive time in the third quarter appears to validate Fannie Mae's earlier opinion that the rate has stabilized. They warn however that the same census report indicates the rental market may be softening. The vacancy rate for all rental housing types rose on an annual basis for the second consecutive quarter to its highest reading in more than three years, 7.5 percent. This is partially because the supply of apartment units, especially in large metro areas and at the high end of the price scale, has increased.

The economists are holding to their forecast of gradually rising interest rates; remaining near 3.9 percent in the fourth quarter and rising to 4.2 percent by the end of 2018. They have revised their projections for housing starts through the end of next year down to 1.250 million and expect total home sales to increase by 1.4 percent this year compared to 2016.

Total mortgage originations in 2017 will be down 12 percent from 2016 to $1.81 trillion and the share of refinancing will decline by 12 points to 37 percent. Originations will fall by another 5 percent to $1.71 trillion in 2018 and the refi share will shrink to 31 percent.

In its broader look at economic developments, Fannie Mae says the hit expected from the hurricanes either did not materialize or was drowned out by growth in business optimism. Both business fixed investment and inventory building pushed the economy to grow at a 3 percent pace in the last quarter. One contributor has been the high level of auto sales resulting from the need to replace vehicles destroyed by Hurricanes Irma and Harvey. Housing remained a soft spot, as the residential investment component dragged on the economy for the second consecutive quarter, subtracting 0.2 percentage points from growth.

The 3.0 percent annualized growth of the GDP in preliminary estimates for the third quarter would make it the first time there was back-to-back growth of that magnitude since 2014, and it was six-tenths of a percent stronger than Fannie had forecast. That, along with data showing a pickup in domestic demand at the end of the quarter has led them to revise their forecast for the fourth quarter GDP up by 0.2 percent to bring the annual rate to 2.4 percent. They forecast growth will moderate to 2.0 percent in 2018. A tax cut, if enacted, presents some upside risk to growth next year.