Freddie Mac's Economic and Strategic Research Team gave its forecast for housing in 2018 (which, as discussed below, it is now hedging a bit) in its October Outlook. This month they present a retrospection of how housing fared in the old one. Since we all lived through it, too much detail would be overkill, but for the sake of nostalgia (or maybe relief), a brief review.

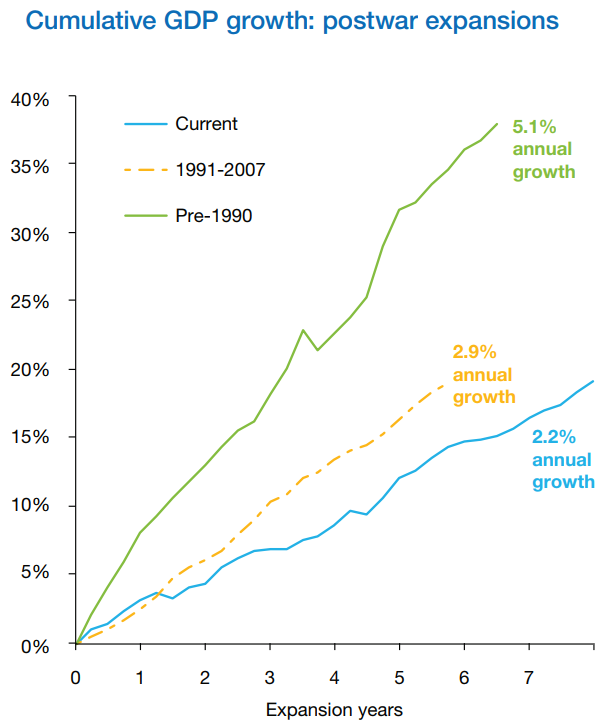

Not for the first time, Freddie Mac says 2017 appears on track to finish as the best year for housing in a decade. It was fostered by a GDP that averaged slightly over 3.0 percent in the first half of the year, and even though this expansion has been modest relative to other recoveries, it has been consistently positive. Robust job gains have helped support homebuyer demand, although wage growth has been disappointing.

Low inflation has also helped; consumer price inflation has averaged about 1 percent over the last three years while core inflation (without volatile food and energy prices) has risen just under 2 percent. This has helped keep long-term interest rates low. Those rates have been bouncing around, rising by a quarter-point following the November 2016 election and remaining over 4 percent through the first quarter of the year. Rates then settled back, and, at least until recent weeks, stayed below that level, helping to counterbalance rising home prices in the battle for affordability.

Despite the favorable environment created by the above factors, housing markets have stalled in the second half of the year. Freddie Mac says this is due to, wait for it, low inventory.

Single-family housing starts "kept grinding higher," but not enough to offset the decline in multifamily ones and home sales lost momentum mid-year. The early momentum of both starts and sales however, will be enough to carry them to their best year since the recession.

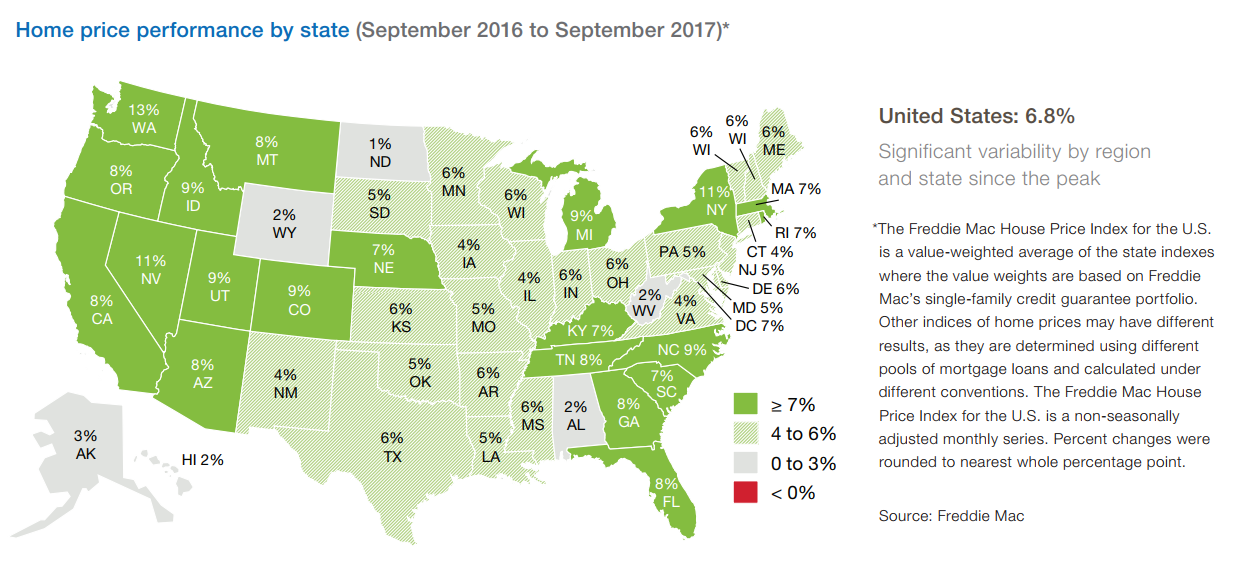

Strong demand, low mortgage rates and a lack of for-sale inventory pushed national home prices up 6.4 percent on an annual basis in the third quarter. Growth in some markets like Washington and Nevada has exceeded 10 percent, leading to concerns over a price bubble.

Low interest rates have allowed single-family mortgage origination volume and the refinance share to hold up better than expected, but it doesn't take much to dampen refinancing. During the first three quarters, when rates were mostly over 4 percent, refinance originations declined 35 percent year-over-year. Purchase activity partially offset the decline, but full-year volume is expected to be down around 15 percent from 2016.

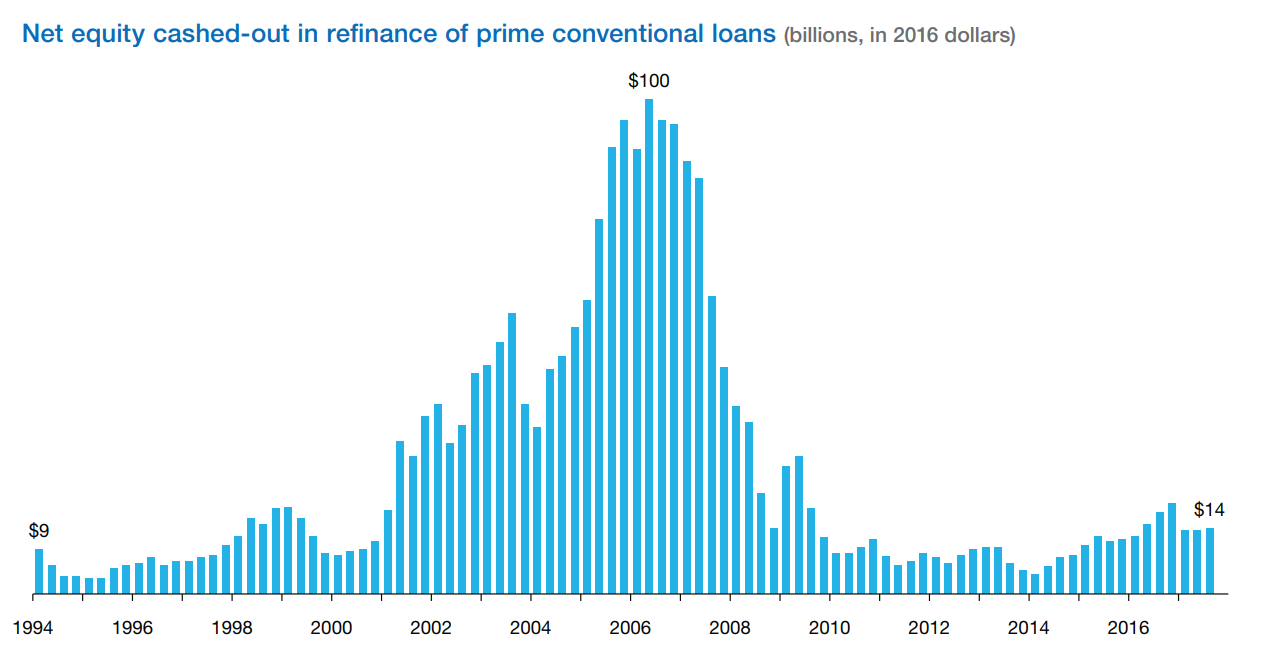

As home values and equity increased, the Federal Reserve put the annual gain at $1.3 trillion in Q2, so has the share of those refinances in which equity was extracted. Cash-out refinancing, while remaining far below the 89 percent share in 2006, continues to grow, representing 62 percent in the third quarter of this year.

Freddie Mac estimates that $13.5 billion in net home equity was cashed out in the third quarter through refinance of conventional, conforming mortgages, up from $13.1 billion in the second quarter. This, however, is less than 25 percent of what was extracted during the peak of such refinancing in Q2 2006, $100.2 billion in 2016 dollars.

Borrowers who refinanced, regardless of whether they took out cash, cut their mortgage rate by about 60 basis points or 14 percent. Thirty-one percent of refinancing homeowners took out shorter-term fully amortizing loans, but this is 35 percent fewer than in the previous quarter.

Borrowers who refinanced had held their old mortgages a median of 6.1 years and saw a median of 15 percent in appreciation during that period, the highest appreciation rate since the third quarter of 2008.

As to that hedging on the 2018 forecast. Freddie's economists say, given the levels of uncertainty surrounding proposed changes in tax policy in both the House and the Senate's current bills, they haven't factored the potentially large impacts into their forecast. "Estimates from different analysts show a large variation in estimated impact, based on assumptions about which provisions will be enacted and how the economy will respond. Given the uncertainty around the tax proposals and their impact on the economy, we present a baseline forecast assuming no tax changes."