When one thinks about renters it is usually clusters of three-story garden style apartments, or high-rise elevator buildings that come to mind. But Freddie Mac says that the majority of America's 43 million renter households, 25 million of them in fact live in properties considered single-family housing - detached homes, townhomes, and two-to-four-unit properties (with the last category accounting for about 8 million units). The total valuation of single-family rentals (SFRs) is estimated at well over $4 trillion, compared to $3.7 trillion for the traditional five+ unit rental properties. Urban dwellers make up 35.5 million of the nation's renters while 7.5 million live in rural areas, but in the latter, 66 percent of the rental stock is single family housing.

Because of the heavy involvement of single-families in the rural market, one generally considered to be underserved by the housing finance industry, Freddie Mac has taken a comprehensive look at the SFR market and how it is owned and financed. The study is part of the company's Duty-to-Serve (DTS) obligation from the Federal Housing Finance Agency (FHFA). It looks first at the current and evolving SFR market and we have summarized its findings here. The second part, an examination of where demand is expected to take the market and the role Freddie Mac may play in its financing, will be discussed at a later date.

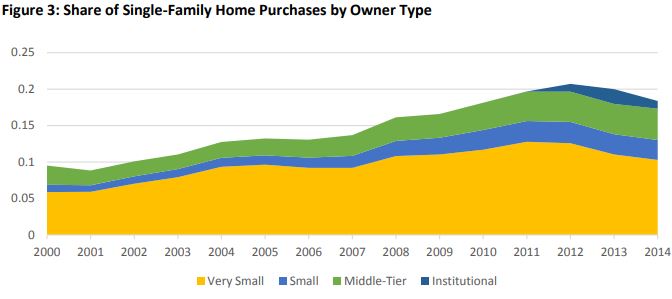

The SFR sector has been evolving rapidly. In the 20 years preceding the Great Recession, SFRs stayed in the vicinity of 10-12 million units or a 30-35 percent market share, however the years since the Recession have seen the addition of 4 million rental homes, an increase of 35 percent. (Editor's note: numbers and percentages are a bit confounded in this report as Freddie Mac's sources vary in how they define "single-family housing." Some numbers, such as the 35 percent increase, include only one-unit detached housing.)

This also accounts for substantial variation in estimates of the total valuation of SFR assets. In addition, as Freddie Mac points out, not all homes used as rentals carry mortgage debt and in fact are not uniformly financed in that manner as is the SF ownership or the multifamily rental markets. However, if the leverage among SFRs was assumed to be similar to the latter's 35 percent loan-to-value (LTV) ration, it would suggest a debt market of $1 to $1.5 trillion.

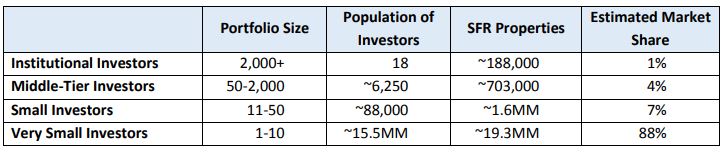

The typical SF investors have traditionally been of the small mom-and-pop variety. During the housing crisis, with lender-owned real estate flooding the market, large institutions began to buy up houses, individually and in bulk. To understand the different ownership types present in today's market, Freddie Mac used data from HouseCanary which focuses on the one-unit portion of the market. That data shows that 15.5 million different investors own approximately 23 million units and some consolidation of what was historically a highly fragmented business. Institutional investors did not enter the market until 2012 and have only accounted for 1-2 percent of total purchases through 2014, spending $16 billion between 2012 and 2014 with an additional $3 billion spent on renovations.

The SFR market is not uniform geographically and their ownership varies that way as well. The concentration of SFR stock in rural areas is a reflection of the less concentrated population but also reflects its importance to rural residents where the percentage of renter households living in "other" types of housing - manufactured houses, RVs, houseboats - is almost as large as that living in multifamily units (15 v 19 percent). Often the "other" forms are not new but rentals of older stock in various levels of disrepair.

SFRs play a role in more specialized geographies as well. In those designed by the Federal Housing Finance Agency's DTS regulation as High Opportunity Areas, SFRs house 52.3 percent of renter households and 13.9 percent of households overall. It was in these areas that the SFR had its greatest growth after the Great Recession, 17.9 percent compared to 12.3 percent nationwide. SFRs also provide 28.8 percent of rentals in Areas of Concentrated Poverty (ACPs) as defined by DTS, a 7.9 percent post-depression increase.

A total of 19.2 million SFRs are in metropolitan statistical areas (MSAs), but 1.6 million of these are in rural designated areas. (The Census Bureau has only two definitions - rural and urban. Thus, many areas most would consider suburbia are officially designated rural. Freddie Mac also uses rural and non-rural as alternate definitions). The remaining 3.4 million rural SFRs are spread throughout the country.

Ownership in rural areas tilts toward the smallest investors, 98 percent of which are small or very small. Only 0.04 percent of properties are in institutional portfolios. In non-rural areas there is more middle-tier and institutional involvement, leaving 93.6 percent of SFRs in small and very small portfolios.

Institutional investors have tended to concentrate their purchases in certain markets in Southeast Texas and parts of the Midwest such as Atlanta, Dallas-Fort Worth, Chicago, and Indianapolis. They purchase in areas with low price-to-rent ratios and where values declined significantly during the Great Recession. Middle-tier investors are distributed more evenly across the country.

Freddie Mac says that, while SFRs tend to be larger than multifamily units in the same market they are still an affordable option, especially for those who need larger units. The 2015 American Housing Survey (ACS) put the median size of an SFR at 1,291 square feet (sf) compared with 811 sf in multifamily rentals. The median monthly housing cost (rent, utilities, other costs) is higher in an SFR ($1,023 v $929) but the rent only cost is lower ($810 v $835) as is the rent per SF, $0.79 compared to $1.15.

An analysis of SFRs scattered across the country found that 66 percent of rents are affordable to families earning less than 100 percent of area median income (AMI) and 55 percent are below their respective Small Area Fair Market Rents (SAFMR) for Section 8 rent voucher limits.

Without SFRs there simply is not enough supply of multifamily units to meet rental demand. An estimated 65.2 million people live in them, an average of 2.9 people per unit compared with 2.1 persons in a multifamily unit. They have a higher retention rate (70 percent) than apartments (50 to 53 percent) an indication that residents may become more tied to their communities.

From 2006 through 2012, the growth in SFRs increased substantially, especially among the 35 to 44-year age group, the peak age for raising school-aged children. SF renters in this group increased by 2.6 percent compared to 0.8 percent for multifamily renters and with a 4.7 percent decrease in homeownership.

Several factors have been driving demand for SFRs, some of which apply to rentals in general; tighter mortgage lending standards, the huge millennial generation and its student debt and the rising cost of purchasing and maintaining a home. There has also been a change in household preferences toward renting.

Freddie Mae expects the demand for SFRs could remain strong and even grow. While some renters will transition to homeownership, there will be a need for more SFRs due to constrained affordability and the size of the Millennial generation.

The second part of Freddie Mac's report looks at how demand and growth are expected to play out and what segment of the market might most facilitate that growth, large institutional investors, middle-tier, or the small investor, and the role Freddie Mac might play.