In a past life I worked in a cubicle next to a fellow who always used to say, "I always tell everyone that I give 100% at work. What I don't tell them is that 24% comes on Mondays, 29% comes on Tuesdays, 22% comes on Wednesday, 15% on Thursday, and 10% on Friday."

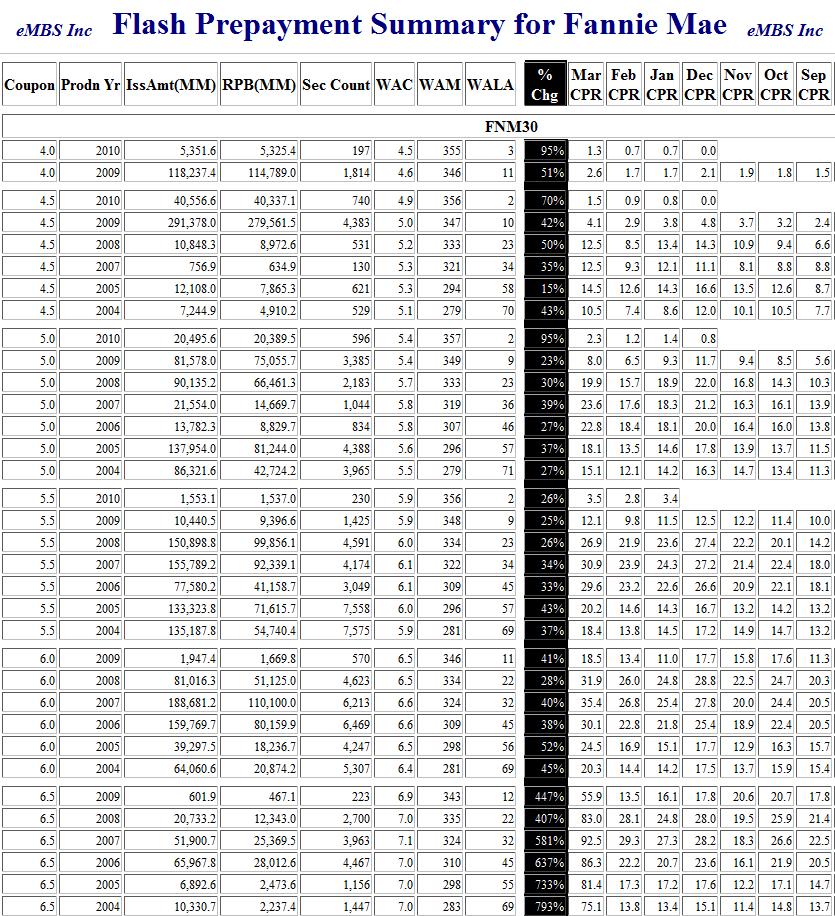

Percentages are important. As is well known, any investor in mortgages must consider default risk, interest rate risk, and early pay-off risk in assessing their value. Although originators rarely get excited about prepayments, investors and "The Street" watch prepay statistics closely, and recently we had a new batch to mull over. Overall it showed no big surprises, with Fannie & Freddie buying out delinquent high coupon loans and some lower coupon loans. Fixed rate Fannie prepayments were up 89% to a 27.6% CPR from 14.6% CPR, due to the announced buyouts of 120+ delinquent loans, 4 extra business days, and higher refi index. There were also buyouts of some trial HAMP loans as a result of the servicer announcement from Fannie Mae on March 5th, which increased the speeds in the lower coupons. Low FICO pools had the highest buyout speeds once again and would clearly be cheapest to deliver pools in the TBA market. Aggregate post-buyout Freddie speeds came in at 17.9% CPR, and Ginnie prepayment speeds were mostly slower.

As was announced, delinquent 6% FNMA Coupons expected to be bought out in April, with 5.5% securities coming in May. As a side note, Ginnie supply - made up of FHA & VA loans - as a percentage of total origination volume has dropped from around 38% to around 30% since December. Banks and foreign investors are replacing the Fed demand for this product - after all, these securities have a 0% risk weighting.

Below is the Fannie Mae prepayment speed summary from eMBS. Notice the huge uptick in prepayments speeds for higher coupons.

If a senior citizen pays even one penny for a reverse mortgage, is the borrower paying too much? The latest trend in reverse mortgage lending is for the lender to charge no origination or servicing fees. MetLife, Pentagon Federal Credit Union, and now Financial Freedom and Generation Mortgage are all taking this approach in making fixed-rate, home equity conversion mortgages (HECMs).

Wells Fargo's correspondent clients learned that "The Coach" expanded their acceptance of MI companies for the new affiliates. Republic Mortgage Insurance Company of North Carolina (RMIC-NC), Republic Mortgage Insurance Company (RMIC), MGIC Indemnity Corporation (MIC), Mortgage Guaranty Insurance Corporation (MGIC), PMI Mortgage Assurance Co. (PMAC), and PMI Mortgage Insurance Co. (PMI). Wells is not, however, going along with Freddie Mac and accepting mortgage insurance issued by Essent Guaranty.

The SEC voted 5-0 to put new rules for non-agency ABS/RMBS securitizations out for a 90-day comment period. We've been through these comment periods before, so here's your chance! The proposed securitization policies include beefed-up standardized minimum loan-level information requirements, which must be posted with the SEC and made available to investors 5 business days before deal pricing, a risk retention requirement, effectively a 5% "vertical" slice of the deal - i.e., 5% of the entire deal, not the first 5% of losses, and the same application of most of the disclosure requirements to 144A deals. Under FAS 166/167, keeping "skin in the game" means that the deal's assets have to stay on balance sheet, obviating a classic motivation of securitization, and impacting the credit rating of the security compared to the credit rating of the issuer and its chance of bankruptcy. Much has to happen before we see the resuscitation of non-agency securitization, and these are steps.

GMAC is tying tie loan officer pay directly to their success in attracting qualified homeowners rather than strictly volume. According to the president of its mortgage operation, "ResCap implemented a new structure for our mortgage loan officers beginning this month that more closely aligns pay for performance." The new policy will affect about 150 loan officers at GMAC's Fort Washington, PA office and is expected to lower overall origination costs. The new policy states that some compensation will be tied to the percentage of applications submitted by a loan officer that result in completed loans.

Commercial loans are still being made, in spite of the predictions that the default rate on older loans is only expected to increase. According to the MBA, Wells Fargo was the top US commercial & multifamily originator in 2009. Other originators in the top 10 include PNC Real Estate, Deutsche Bank, CBRE Capital Markets, HFF, Prudential Mortgage Capital Company, Meridian Capital Group, MetLife, Northmarq Capital, and Capmark Financial Group. Based on investor groups, Wells topped the list for commercial banks & savings institutions, HFF for conduits, MetLife for life insurance companies, PNC Real Estate for Fannie Mae's, CBRE Capital Markets, Inc. for Freddie Mac's, TIAA-CREF for pension funds, Glacier Real Estate Group for credit companies, and Deutsche Bank Commercial Real Estate for specialty finance.

Huh? Mortgage rates improved, even after the Fed stop buying them last Thursday? Wow! Just think of all the folks who thought that mortgage rates would zoom up relative to Treasury rates! (Fortunately I was not one of them - I am so rarely right that I have to keep reminding myself about it.) Money managers, pension funds, insurance companies, and servicers were all buyers, and the only selling came from lenders with about $1.5 billion of origination. READ MORE

With rates going up and now back down somewhat, hedged originators might be feeling a little whipsawed, but since the pipelines aren't all that big these days perhaps the damage is minimal. (And of course the largest owner of MBS (the Fed) controls its own funding costs and doesn't have to hedge.) We are past the quarter-end, almost done with the first of the April auctions, and banks are appearing to be stepping into the void left by the Fed. Remember that the Fed was never a traditional buyer of mortgages, so we are back to a more normal market - another good thing. Origination is still expected to be down 40-50% in 2010 as good credit homeowners refinanced in 2009. They won't be back to refi again in 2010, so most origination will be purchases as we are already seeing. READ MORE

Yesterday we continued to see bonds' prices improve, and rates drop, after a solid $21 billion 10-yr sale by the Treasury. The yield on the auction was within 2 basis points of where the existing 10-yr was trading, indirect bidder participation was solid and the bid/cover was highest for a 10-year auction since at least 1994 - so maybe 4% is the current magical yield after all. The bond market was helped by Ben Bernanke's somber statements about the economy not being out of the woods yet and the fact that inflation is not an issue. On Monday the 10-yr hit 4% for the first time since June, but we've bounced off that level and are now back down to 3.86%. And today we got our first economic news of the week, with Initial Jobless Claims coming in at 460,000, up 18k from 442,000. The 4-week moving average moved up slightly. After the number mortgage prices are generally better by about .125.

(Warning: rated PG)

Two lawyers had been stranded on a desert island for several months. The only thing on the island was a tall coconut tree, their only source of food. Each day one of the lawyers would climb to the top to see if he could spot a rescue boat coming.

One day the lawyer yelled down from the tree, "Wow! I can't believe my eyes. There is a woman out there floating in our direction!"

The lawyer on the ground was most skeptical and said, "You're hallucinating - you've finally lost your mind."

But within a few minutes, up to the beach floated a stunning red-head, face up, totally naked, unconscious, without even so much as a ring or earrings on her person.

The two attorneys went down to the water, dragged her up on the beach and discovered, yes, she was alive, warm and breathing.

One said to the other, "You know, we've been on this God forsaken island for months now without a woman. It's been such a long, long time...So... Do you think we should well... You know... Screw her?"

"Out of what?" asked the other.