Happy New Year. Welcome to MND 3.0!

After 12 months of planning and hard work, we are very excited to launch the updated site. We've added and improved many features in the latest version of the MND platform. HERE is a list of new tools.

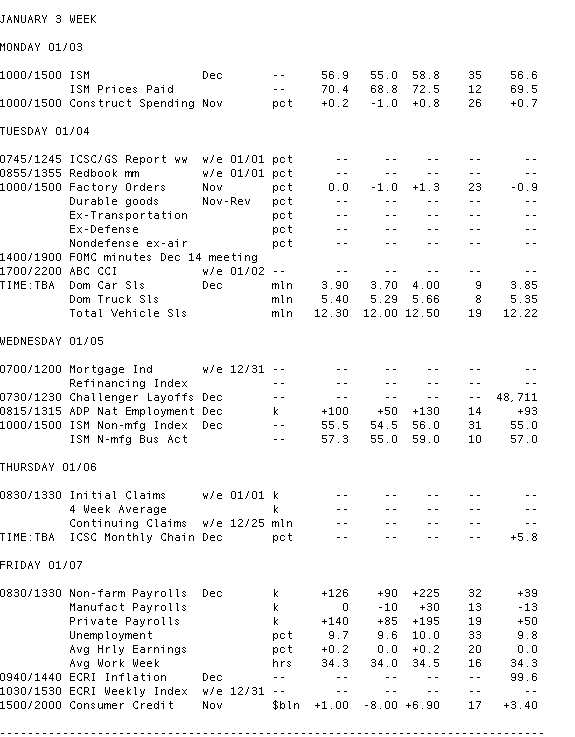

The week ahead offers several important economic events with the most influential data to be released on Friday morning...the Employment Situation Report. This data is expected to dictate the direction of mortgage rates over the coming weeks. That isn't the only news on the horizon though. We'll get an update on manufacturing conditions from the ISM on Monday. The FOMC Minutes from the December 14th Fed meeting will print on Tuesday. Then ISM will update us on non-manufacturing business conditions on Wednesday. December MBS prepayment speeds hit the tape on Thursday afternoon. There are five Fed QEII Treasury coupon purchase operations, one for every day of the week. And last but not least, the newly seated 112th Congress will likely jump right into heated debate over an assortment of issues, including our unsustainable budget deficit and transparency at the Federal Reserve.

Key Events in the Week Ahead:

Monday:

10:00 ― The ISM Manufacturing Index

, a closely-watched measure of the nation’s manufacturing industry, is expected to continue at robust levels in December. Economists polled by Thomson Reuters anticipate the index to come in at 56.9 ― 0.3 points higher than November’s score and 3.2 points higher than the 12-month average. Any score above 50 indicates growth in the industry.

New orders, a forward-looking component of the index, pulled back several points in November, but last week’s regional index from Chicago buoyed spirits when it jumped 6.1 points to 68.6, the highest since July 1988. New orders and employment also hit their highest levels since 2005 in the regional index.

“Regional surveys ― notably the big guns in Chicago, Richmond, and Philadelphia ― pointed to acceleration in manufacturing growth as the old year closed out,” said economists at IHS Global Insight. “Consumer spending appears to be picking up, and that could well have led to some inventory reductions at the end of the year.”

It may worth keeping in mind that the ISM survey “tells us next to nothing” about the small-firm sector, according to economists at High Frequency Economics, who point out that trouble ahead lies with smaller firms.

“We would certainly not choose to ignore the ISM survey, but it does need to be seen in context, and that context is that the headline index has substantially overstated the pace of economic growth in each of the past three quarters,” they said, predicting a score of 58 for the December survey.

10:00 ― Construction Spending

should rise 0.2% in November after a 0.7% pickup a month before, according to economists. As with the previous report, the headline advance masks some of the underlying weakness in the report ― single-family construction, for instance, has been in decline for six months, and four of the 11 categories for private non-residential construction fell to their lowest levels since December 2007.

“We expect nonresidential and multifamily residential construction to drop by 1% or more,” said economists at IHS Global Insight. “Single-family residential should also drop, but by less than 0.5%. These declines will offset increased spending on infrastructure. This pattern, declining nonresidential and residential spending and rising infrastructure spending, is likely to continue for several months.”

10:15 - The Fed will purchase an estimated $7-9 billion in Treasury coupons maturing between 2/15/2018 and 11/15/2010

Tuesday:

10:15 - The Fed will purchase an estimated $1-2 billion in Treasury TIPS coupons maturing between 7/15/2012 and 2/15/2040

2:00 ― Commentary on how appropriate a second round of quantitative easing was may be key to the FOMC Minutes

. Monetary policy was left unchanged at the latest Federal Open Market Committee meeting on Dec. 14. The policy statement was nearly identical to the previous one, as the Fed noted the economic recovery was continuing at an insufficient pace to reduce unemployment. The central bank also indicated it would complete its $600 billion Treasury purchase program, despite notable criticism in the weeks preceding the meeting.

“The market’s QE doubts could become even stronger as 2011 starts up, once consumer spending finds some lift from the cut in social security withholding taxes,” predicted economists at BMO Capital Markets. “However, … the incoming voting regional Fed presidents in the FOMC appear to be slightly more pro-QE than the outgoing group.

Wednesday:

7:00 ― MBA Mortgage Applications

continue to show that purchases remain low and are now under renewed pressure as mortgage rates rise from historically low levels. Refinancings are also taking a hit as those interest rates rise.

Economists at BTMU say 2011 is unlikely to be the year for a housing recovery, even though the dynamics would favor potential buyers locking in low mortgage rates now.

“Home affordability remains near an all-time high even though mortgage rates have risen from a record low of 4.17% in the week of November 12th to 4.81% in the week of December 24th,” they wrote. “Rising mortgage rates may even act as a catalyst for home sales if buyers believe rates are only going up giving more import to buying now. Prices are also very attractive, but now that they are falling again it could actually be a deterrent for home buying because who wants to buy a major asset that could very well fall further in value?”

8:15 ― Economists look to see 100k new private-sector jobs in the ADP Employment Report for December

. The survey last indicated that 93k private jobs were added to the economy in November ― the most in two years ― after a gain of 82k a month before. However, the “official” BLS report showed only 50k new private jobs in November, so it’s not clear how seriously the market will take this report.

Still, some economists believe the low number of jobless claims in recent weeks suggests some upward revision to the BLS report, which could mean the ADP report last month was right after all.

“Our model, based on jobless claims, the help wanted index and ISM employment, suggests the survey will report private payrolls rising by about 124k or so, after a 93k increase in November,” said economists at High Frequency Economics.

Forecasts range from 30k to 150k, according to 14 economists polled by Thomson Reuters.

10:00 ― The ISM Non-manufacturing Index

, a measure of the services, financial, and construction industries, is predicted to rise half a point to 55.5 in December. Any score above 50 indicates growth, and the 0.7 point climb last month meant the sector expanded at its fastest pace since May. New orders picked up one point to 57.7, the highest in seven months, and the employment component improved to 52.7 ― its strongest reading since October 2007.

“Cross currents continue to move in both directions, with financial markets, employment conditions and business activity improving,” said economists at IHS Global Insight. “However, orders momentum remains modest and freight activity is taking a step back after a couple of months of gains. On net, we are looking for a modest gain in the overall index.”

10:15 - The Fed will purchase an estimated $1.5 - 2.5 billion in Treasury coupons maturing between 8/15/2028 and 11/15/2040

1:00 ― Thomas Hoenig

, president of the Kansas City Fed, speaks before event hosted by The Central Exchange.

Thursday:

8:30 ― The four-week average for Initial Jobless Claims

fell 12.5k in the week ending Dec. 25 to 414k ― the lowest level since July of 2008. Weekly claims fell 34k to 388k, well below the consensus forecast of 415k. Pleasant as those numbers are, economists promptly called the surprise report unreliable given the distortions from a four-day workweek, the holiday season, and so on. (The Labor Department maintained this was a ‘clean’ report, however.)

For the final week of the year, economists expect to see a seasonally-adjusted 412k claims. Many point out that this week too will be dubious, and suggest we won’t have a reliable figure until mid-January.

“The fact that claims appear to be breaking out of the range held for much of the year ―

roughly 450k to 485k ― leads us to believe that the labor market is building momentum,” said economists at Deutsche Bank, who called the downtrend a significant development for the economy.

“That being said, we are somewhat concerned that there could be a measurable weather impact on the claims and payroll figures as a result of the recent blizzards in the upper Midwest and Northeast,” they added.

10:15 - The Fed will purchase an estimated $6-8 billion in Treasury coupons maturing between 1/31/2015 and 6/30/2016

11:00 ― Treasury announces the terms of debt supply to be auctioned in the week ending January 14. 3s, 10s, and 30s will be offered by Treasury.

The December prepayment report will be released on Thursday afternoon.

Friday:

8:30 ― The December Employment Report

is expected to show the economy added 126k new jobs to the economy last month, including 140k new private-sector jobs. (Government jobs are expected to be depressed, bringing the headline figure down).

Forecasts for the headline figure range from 90k to 225k, according to 32 economists polled by Thomson Reuters. The report follows a disappointing November report in which a net 39k jobs were created, including just 50k private jobs.

Some economists believe the November report could see upward revisions, based on better data from jobless claims, the ISM employment components, and the ADP report.

Economists at BTMU, for instance, wrote: “The November payroll report was very disappointing, showing only +39K jobs were created over the month. But the stock market shrugged it off because other labor market indicators leading up to the report had been positive. We expect November’s job count to get an upward revision.”

Looking to December’s report, economists at IHS Global Insight said firms “are becoming more confident in the expansion, and hiring is improving as a result.”

“Continuing declines in initial unemployment insurance claims indicate that the very weak November employment report was an aberration,” they wrote. “We expect payroll employment gains to improve to 150,000 in December from just 39,000 in November, and the unemployment rate to edge down to 9.7% from 9.8%.”

10:00 ― Ben Bernanke

, chairman of the Federal Reserve, testifies to the Senate Budget Committee on monetary and fiscal policy.

10:15 - The Fed will purchase an estimated $6-8 billion in Treasury coupons maturing between 7/15/2013 and 12/31/2014

4:30 ― The Fed’s vice chairwoman, Janet Yellen

, and several Fed Bank presidents including Charles Evans from Chicago, speak to the American Economic Association convention in Denver.

3:00 ― Consumer Credit

is expected to expand for the third consecutive month in November. Economists forecast a $1 billion increase, following a $3.4 billion expansion in October. However, the string of increases is rather misleading. Consumer debt shrunk $52 billion in the first 10 months of the year, and the recent increases are the result of federal student loans.

“Consumer credit is expected to gradually make its way back into positive territory,” wrote economists at IHS Global Insight after the October report. “However, it would not be a surprise to see a string of consumer credit declines in the upcoming months as the household deleveraging process continues. Holiday sales are expected to be up 4.5% versus last year, but consumer prudence will remain key in determining whether purchases are made on a cash or credit basis.”