Black Knight Financial Services took close-up looks at both home affordability and the recent surge in cash-out refinancing in its new Mortgage Monitor released on Monday. The publication reflects data through the end of December 2015.

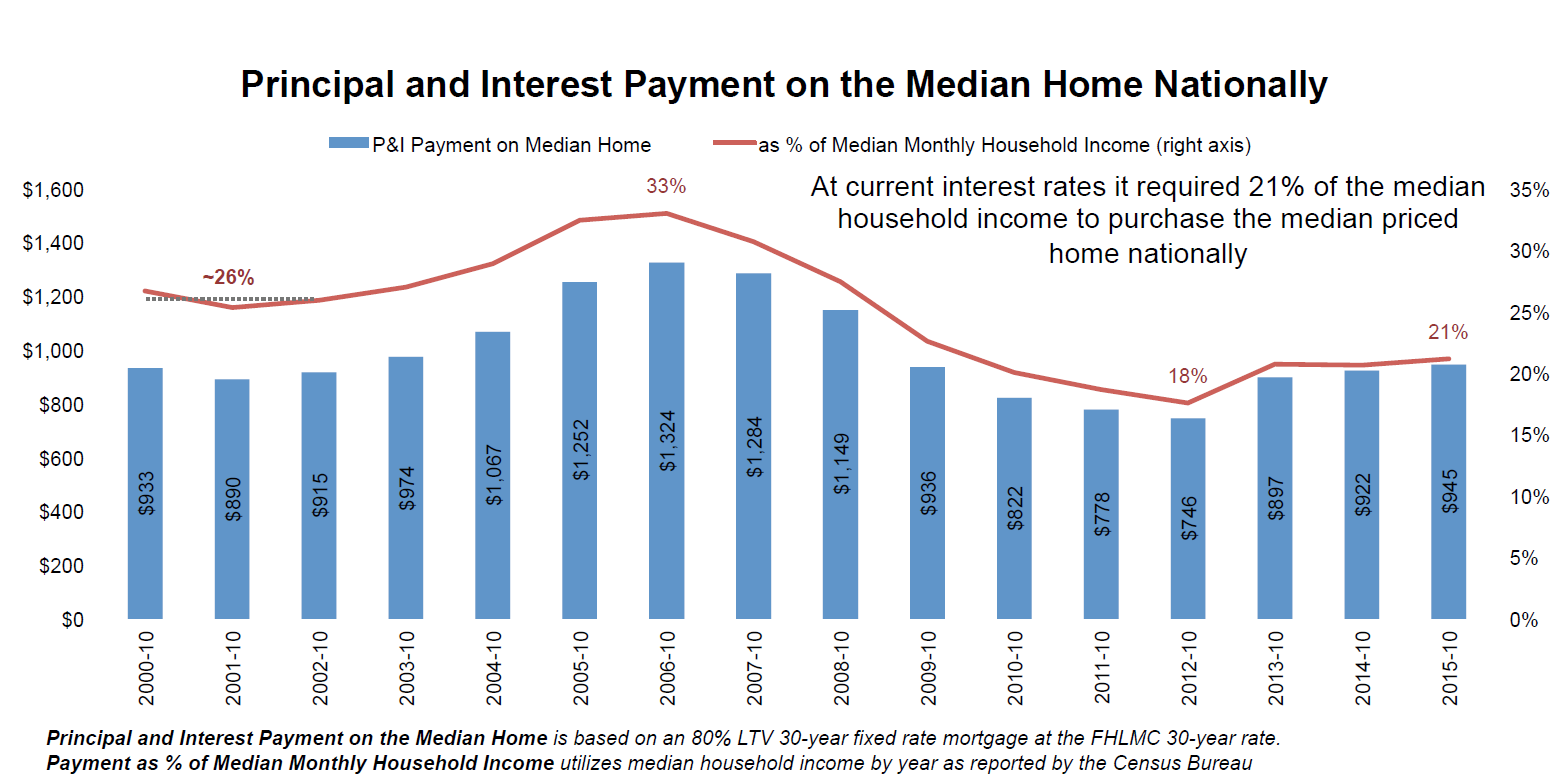

The company said that there have now been 43 consecutive months of annual home price appreciation, causing it to revisit the question of affordability. Its analysts used national medians for home prices and household income levels and found the mortgage payment-to-income ratios still favorable by historic standards.

Looking at median principal and interest payments in each October over the last 15 years the company saw those payments consuming 26 percent of median household income in 2000, rising to 33 percent at the peak of the bubble in 2006 before falling to 18 percent as prices bottomed out in 2012. The median across those years was 26 percent. In October 2015 a mortgage payment required 21 percent, still considered an affordable level.

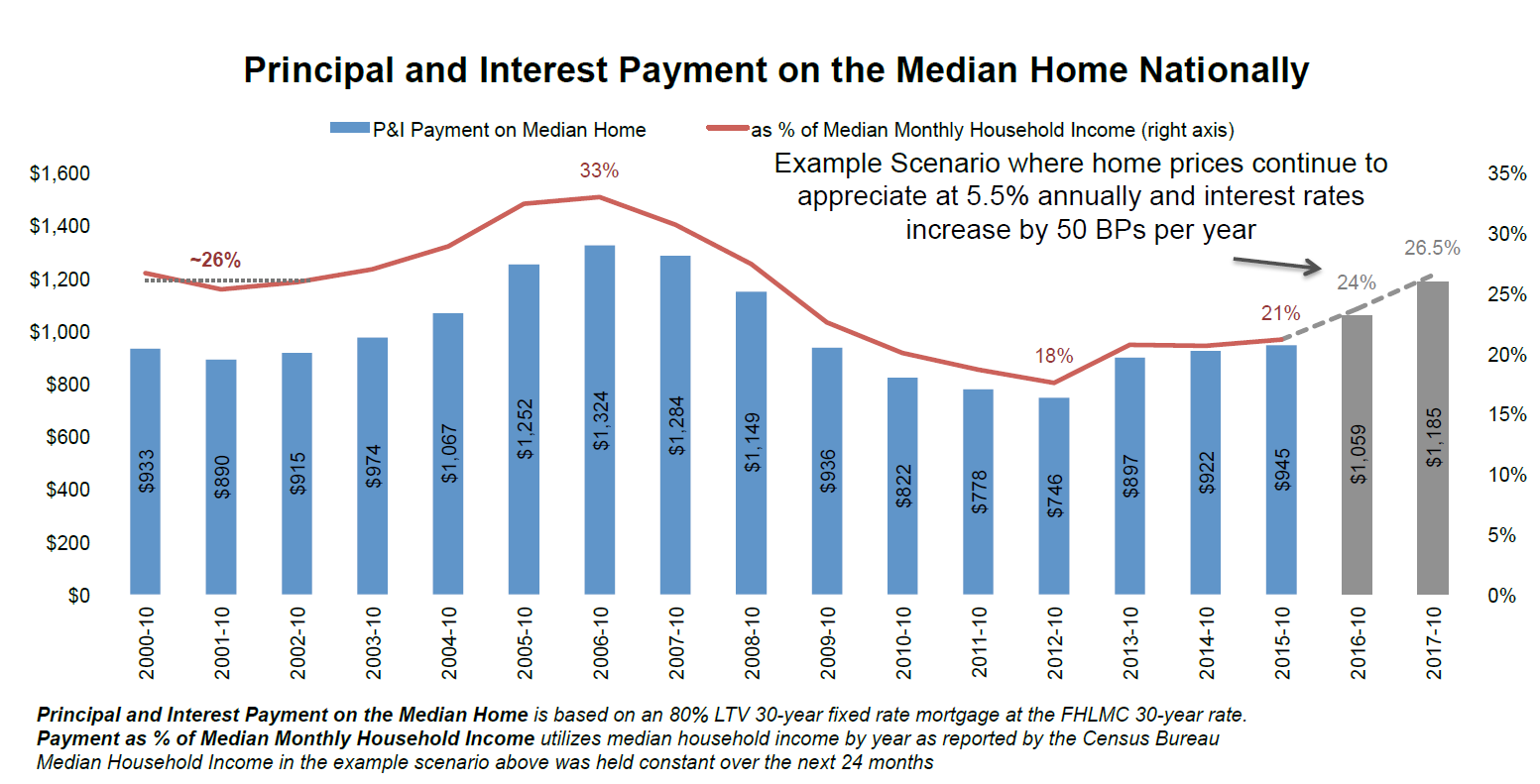

However, as Black Knight Data & Analytics Senior Vice President Ben Graboske explained, the long-term impact of rising interest rates and home prices on affordability varies with geography and warrants close observation moving forward. " When we look at an example scenario using today's rate of home price appreciation and a 50-basis-point-per-year increase in interest rates," Graboske said, "we see that in two years home affordability will be pushing the upper bounds of that pre-bubble average."

Under this scenario, within 12 months the payments on a median priced home would rise $114.00 per month requiring 24 percent of household income, still below the 2000-2002 average. After 24 months the monthly payment would be $240 higher consuming 26.5 percent of income. Black Knight points out that interest rates have a much greater impact on affordability than home price appreciation. A 1 point rise in rates is equivalent to a 13% jump in home prices.

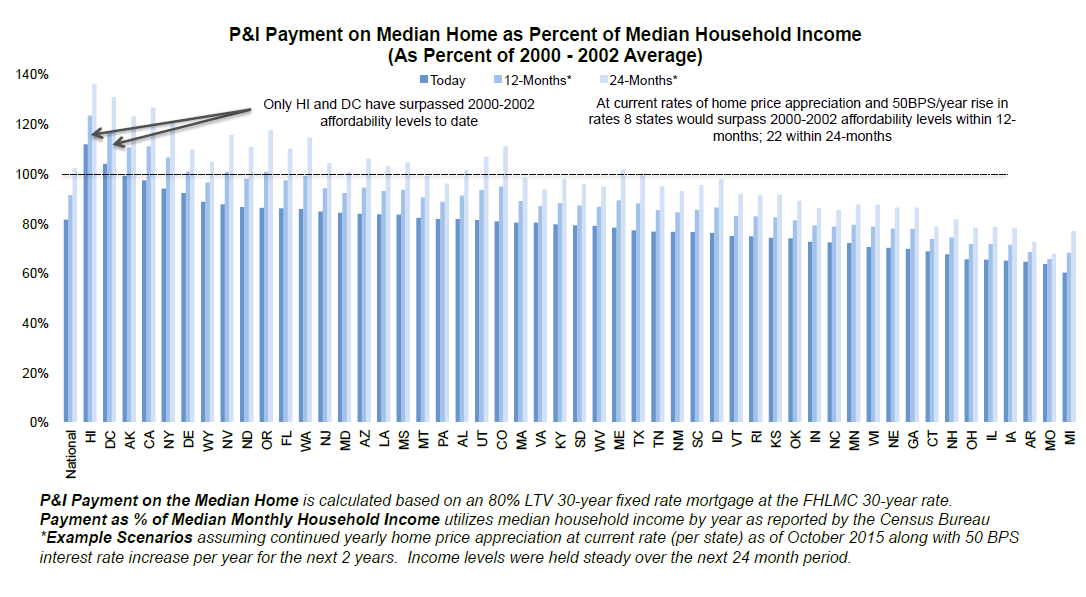

While rates rise similarly across states those increases can have different impacts on affordability from state to state. Black Knight applied the same formula to each state, benchmarking each against its own pre-bubble affordability ratio.

Graboske continues, "At the state level under that same scenario, eight states would be less affordable than 2000-2002 levels within 12 months and 22 states would be within 24 months. Right now, both Hawaii and Washington D.C. are already less affordable than they were during the pre-bubble era. On the other hand, even after 24 months under this scenario, Michigan - among other states - would still be much more affordable at the end of 2017 than it was in the early 2000s.

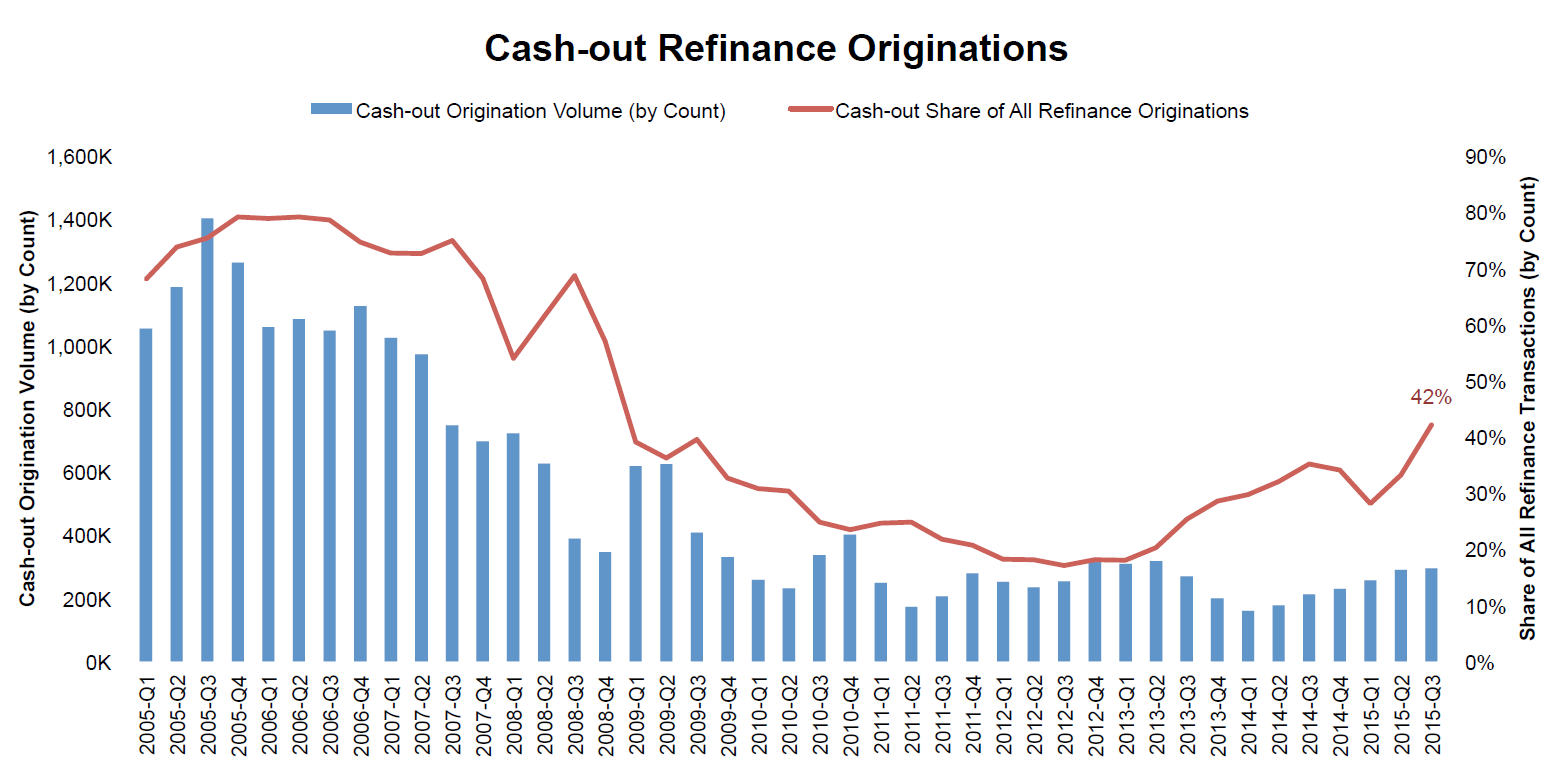

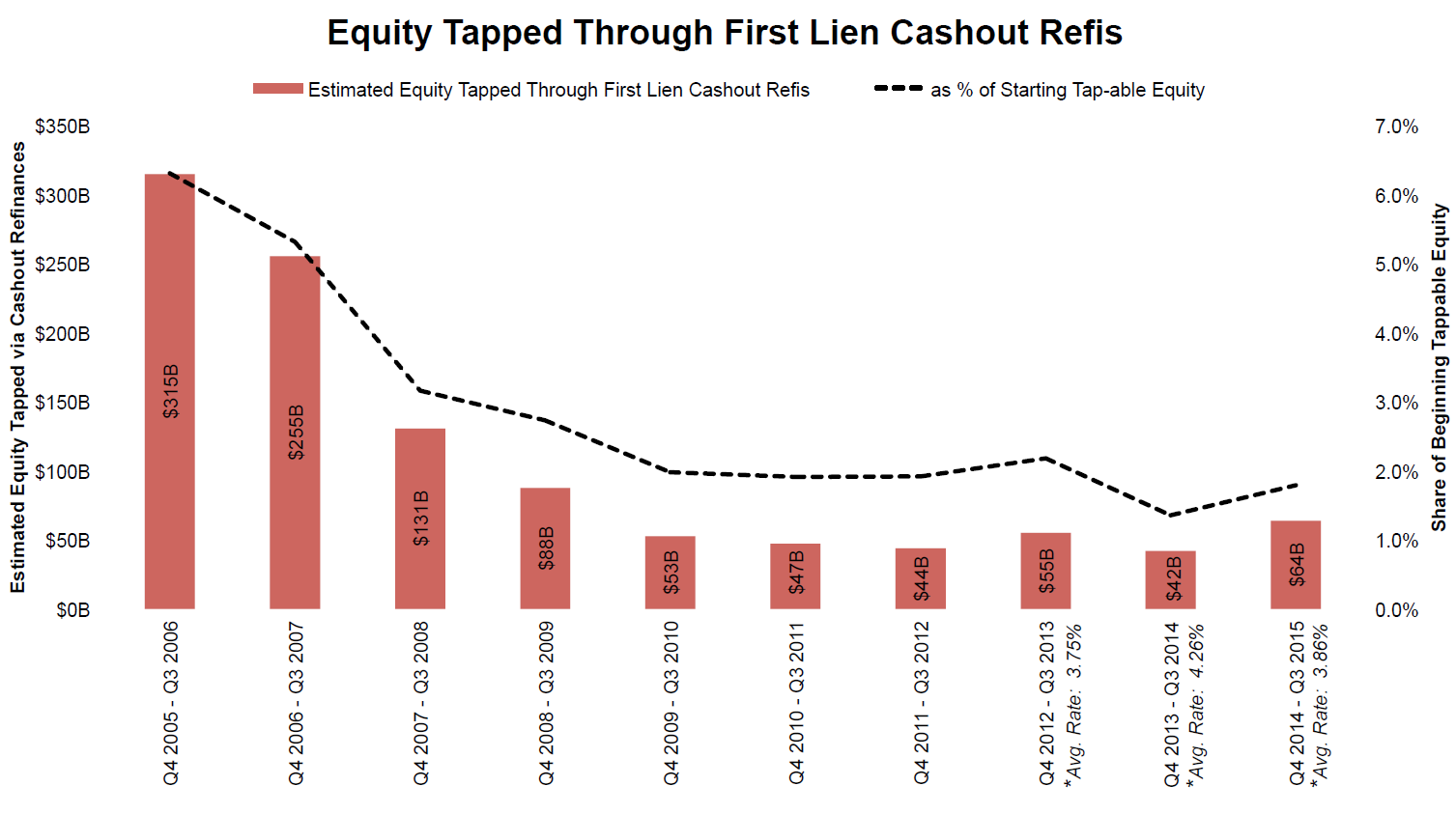

Even though they had touched on it in the January Mortgage Monitor Black Knight returned to the subject of cash-out refinances. There were nearly 300,000 such refis originated in the third quarter of 2015, about 42 percent of all first mortgages refinances, and roughly a million were origination over the most recent 12 month period. Cash-outs have increased for six consecutive quarters.

Likewise the average cash-out amount of over $60,000 is the highest since 2007. The total amount of equity tapped out over the past 12 months was $64 billion, the highest dollar amount for any 12 month period since 2008-2009. Still this is less than 2 percent of the available equity that might be tapped, 80 percent less than the total amount of equity extracted from housing in 2005-2006. The last time interest rates rose by 50 basis points, in late 2013, early 2014, the share of equity tapped dropped to the lowest on record, below 1.5 percent.

As the Monitor pointed out last month, the resulting loan-to-value of these originations is a record low of 67 percent, and the credit score of the borrowers involved is quite high at an average of 748. That score however is still 30 points lower than the average for home equity lines of credit (HELOCs). This, Black Knight says, may entice some potential HELOC borrowers with more moderate credit scores to opt for a refinance even though rates may be slightly higher.