Fannie Mae says it expect economic growth will improve on its anemic performance in the first half of 2016 in the second half of the year, rising to 2.4 percent from 1.1 percent. This estimate in the company's October Economic Developments Commentary is a slightly slower pace of growth than its economic and strategic research team had predicted earlier. Their full year forecast remains at 1.8 percent.

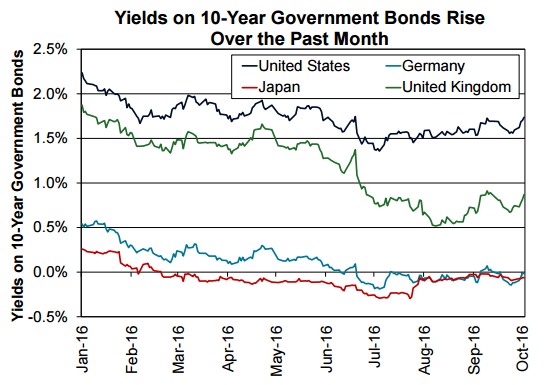

Treasury yields have moved higher recently along with long-term sovereign yields in other developed markets as investors perceive the global central banks such as the European Central Bank and the Bank of Japan are tapering their quantitative easing programs. Financial markets also remain convinced that the Federal Reserve will increase the target rate this year, something supported by the Fed Funds futures which put the odds at 65 percent. Because a lot of data including two jobs reports are due before the next Federal Open Market Committee meeting however, Fannie Mae is continuing to predict there will be no rate hike this year.

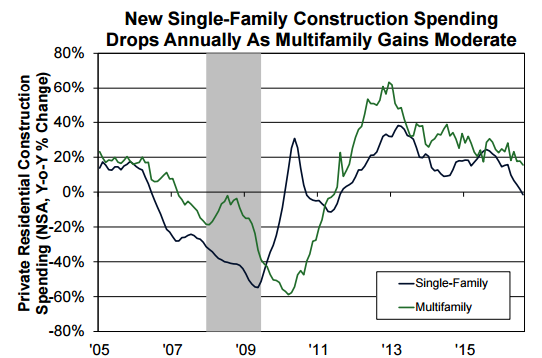

Fannie Mae calls private residential construction "lackluster," driven by the ongoing decline in new single-family construction spending which was down in August for the sixth consecutive month and fell below year-earlier figures for the first time in five years. Spending on multi-family construction is still growing but the annual increase has moderated to the weakest pace since October 2011.

The decrease in residential spending is the result of flat single-family housing starts and a decline in the average cost per single family starts which began late last year. The economists say they had predicted last month that residential investment had fallen in the third quarter but the August construction spending report issued since then suggests that the drop was steeper than expected.

Homeownership demand does seem to have picked up last year. American Community Survey data shows that owner household growth in 2015 exceeded rental household growth for the first time since the 2007-2009 recession started. The same survey showed the homeownership rate for households under age 35 which had "declined substantially and relentlessly" over the previous eight years finally stabilized.

In recent months housing activity has clearly lost momentum. Existing home sales fell in August for the second consecutive month, reaching the lowest level since February and pending home sales dropped in August for the third time in four months to the lowest level since January.

While new home sales were fell in August they were down off of the best month in the recovery in July. Single family housing starts were also down significantly. Fannie Mae says the recovery in single-family homebuilding has been very gradual, partly because of land and labor constraints.

There is a positive note for young homebuyers, as builders seem to be focusing more on the entry-level market. The typical size of a new single family home, which rose sharply at the end of the recession, stabilized in 2014 and 2015 and the median size has now begun to shrink. "As builders adjust their production in response to rising demand for entry-level homes, typical new home size is likely to trend lower going forward, which should help to sustain the fledgling recovery in homeownership."

Purchase mortgage applications declined in August for the second consecutive month indicating continued weakness in existing home sales in the near term but they did rebound in September even as refinancing applications dropped for the second consecutive month in September after a surge in July.

The inventory of existing homes for sale remains extremely lean, down 10.1 percent in August from a year earlier, the largest annual drop since 2013. The lack of homes for sale is partly attributable to the fact that homeowners are remaining in their homes longer. CoreLogic says the median years a homeowner has owned his home rose from five years in 2007 to 10 years in 2015.

Mobility rates have also been declining, indicting a lower rate of housing turnover and consequently home sales. "This will be challenging for the housing and mortgage market, especially in a rising mortgage rate environment where lenders have to rely more on purchase mortgage originations," the economists say. "Tight supply and rapid price gains in the lower tiers of the home sales market are increasingly hampering first-time home buyer affordability and endangering the budding recovery in young-adult home buying demand.

Fannie's economists have not changed their mortgage rate forecast as they don't think the recent rise in long-term interest rates are sustainable. They are also essentially holding to their September forecast of a 3.6 percent increase in total home sales this year, but the total includes weaker existing home and stronger new home sales.

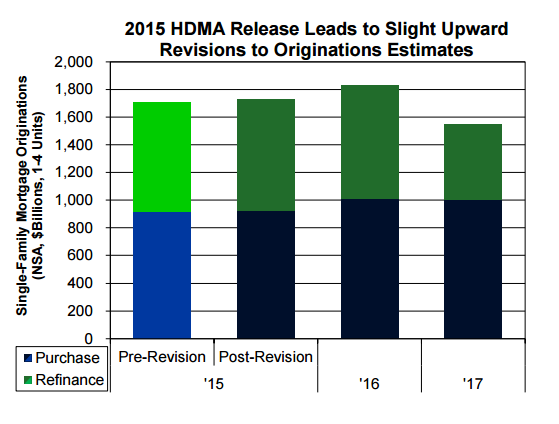

Each October Fannie Mae updates its estimates one-to-four-unit property mortgage originations for the prior year as a result of benchmarking to new Home Mortgage Disclosure Act (HMDA) data. They have revised slightly higher their estimated purchase and refinance originations for 2015 by $6 billion and $13 billion respectively for an originations total of $1.73 trillion. The refinance share rose 1 percentage prior from its prior estimate to 47 percent. The estimate of 2016 originations has increased by $30 billion to $1.83 trillion, an increase of about 6.0 percent. Refinancing accounts for most of the upgrade. Total originations are expected to decline by about 15 percent in 2017 due to a decline in refinancing.