While recently passed Tax Cuts and Jobs Act will benefit the take-home pay of most Americans, and allow them to save up to buy a home if they wish, other factors will offset that benefit. This will make renting look more attractive than homeownership to many.

Two analysts, Laurie Goodman and Edward Golding, writing for the Urban Institute (UI) looked at the potential impact of the new law and constructed a matrix showing how changes will affect families in various income groups. Their calculations take into account that the increased standard deduction will mean fewer taxpayers will itemize and the lower rate will mean smaller benefits for those who do.

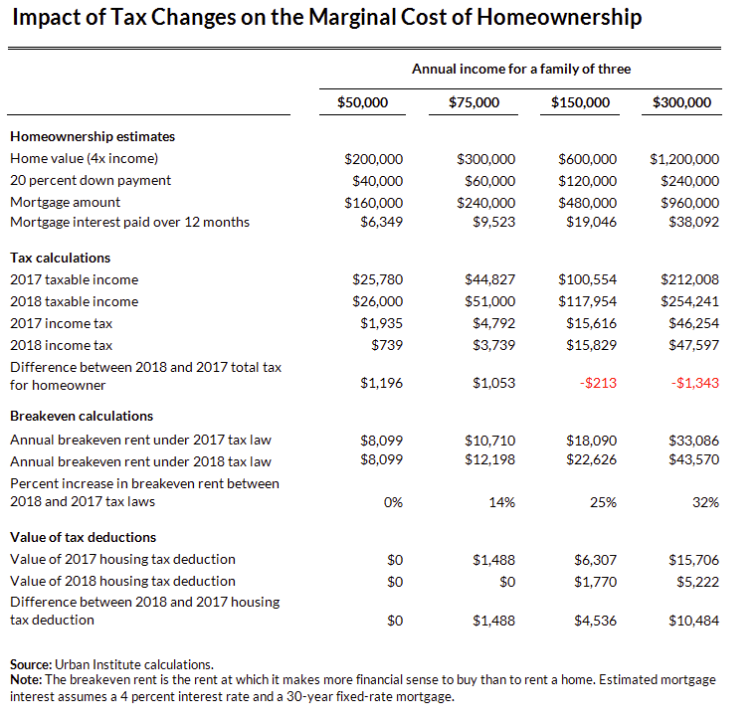

UI profiled four families, each with three members, and earning $50,000, $75,000, $150,000, and $300,000 a year. Each buys a home valued at four times their annual income, putting down 20 percent and obtaining a mortgage at 4.0 percent. UI made the following additional assumptions.

- Property taxes are 1.5 percent, repairs and maintenance 1.5 percent, and homeowners' insurance 0.375 percent of home value

- Expected appreciation is 3 percent of home value

- Families who rent must have rental insurance

UI then looked at the total tax bill under the old and new laws with similar assumptions about state taxes and charitable giving, and factoring in the differences in tax advantages for owner occupants under each tax code. They also computed the rent that results in the same all-in cost of housing. In effect, they compute the user cost of owner-occupied single-family housing.

UI Notes the following outcomes.

The family in the lowest income tier takes the standard deduction under both plans but its taxable income changes very little, from $26,000 to $25,780, in 2018 as the family gains the higher standard deduction but loses the $4,050-per-person standard deduction.

The bottom line is a tax bill that shrinks by $1,196 due to the lower effective tax rate and a doubling of the child care tax credit to $2,000. Using the standard deduction eliminates any impact on the homeowner versus rental decision.

The family with $75,000 in annual income would have itemized under the old tax bill but not under the new one because of the increased standard deduction. This raises their taxable income from $44,827 to $51,000 because of the loss of the personal exemption but their tax bill is $1,053 lower due to the lower marginal tax rates and higher child credit.

Although the tax savings could be put toward a down payment on a home, the savings from owning a home have been reduced by $1,488 for the year ($124 per month). The family is not itemizing so cannot claim the mortgage interest deduction (MID) or deduct property taxes.

For this family, the breakout rent, the point where rents rise to a lever where it is preferable to buy, goes up by 14 percent. Under the 2017 tax code, that point is reached at $892 per month ($10,710 per year) The 2018 law raises it to $1,017 monthly or $12,198.

The family with $150,000 in income would itemize under both tax codes, but that would result in a much larger taxable income in 2018, $117,954 versus $100,554. They lose the personal exemptions and face a cap on the deductibility of state and local taxes. But the total tax bill rises only slightly (by $213), as the higher taxable amount is largely offset by the reduction in the tax rates and the increase in the child credit.

There is, however, a big difference in the rent or buy decision. The tax savings from homeownership are much smaller, or $4,536 less per year, or $378 per month. This reduction is because of the larger standard deduction, the cap on state and local taxes, and the cuts in the marginal tax rates.

Under the 2017 tax code, this family would prefer to own once rents hit $18,090 per year or $1,507 per month. But under the 2018 code, the rental breakeven point is $22,626 per year or $1,885 per month, or a 25 percent increase.

The family with $300,000 in annual income would also have much higher taxable income under the new code, $254,241 versus $212,008. They lose the personal exemption and face a cap on their state and local taxes. Their income was too high in 2017 to qualify for the child care tax credit in 2017, but it is not in 2018. The family pays $1,343 more in taxes because as the lower rates and the benefit from the child care credit do not completely offset the higher taxable income.

But the homeownership picture changes dramatically. The benefits from owning are slashed by $10,484 per year, or $874 per month. Under the 2017 tax code, the family would choose to own once rents hit $33,086 per year ($2,757 per month) or more. The breakeven point in 2018, however, will now be at $43,570 per year ($3,631 per month), a 32 percent increase.

Goodman and Golding conclude, "Do we expect people not to buy because of these changes? At the margin, yes. But because homeownership is generally more affordable than renting, and there are other benefits to homeownership (stability, an inflation hedge, more and different choices in size and location of houses), the impact on homeownership rates will likely be small.

"Nevertheless, the effect of these changes may increase, possibly resulting in a slightly lower homeownership rate as more households choose to rent."