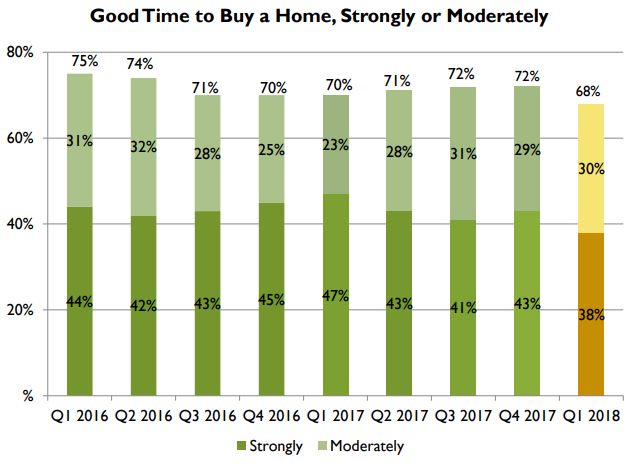

Positive attitudes toward home buying still predominated in the National Association of Realtors® (NAR) most recent Housing Opportunities and Market Experience (HOME) survey, but they are softening. "Yes" responses to the question of whether it is currently a good time to buy dropped from 72 percent in the fourth quarter of 2017 to 68 percent in the first quarter of this year, with 5 percentage points of the decline coming from those who "strongly" felt it was a good time.

Those who were moderate in their responses rose 1 point. NAR said the survey's findings "surprisingly show that while a growing share of households in the first three months of the year feel more confident about the economy and their financial situation, those positive feelings are not translating to positive views that now is a good time to buy a home."

The positive answers were strongest among the older respondents (84 percent among those 55 to 64 and 77 -percent for those older than 65) while only 55 percent of those below the age of 35 i.e. Millennials, concurred. Positive responses rose with income and there were strong regional differences - three regions had responses ranging from 67 to 74 while only 58 percent of those living in the West viewed it as a good time to buy. Rural consumers had a 78 percent positive response rate compared to 69 percent of suburbanites and 59 percent living in cities. Homeowners were much more positive (76 percent) than renters (55 percent) or those living with someone else (60 percent).

NAR Chief Economist Lawrence Yun says extremely challenging market conditions to start the year are chipping away at homebuyer optimism. "The critical shortage of listings in most markets continues to spark a hike in home prices that is not easy for many buyers - and especially first-time buyers - to overcome," he said. "Adding more fuel to the affordability fire is the fact that mortgage rates have shot up to a four-year high in just a few months. Many house hunters are telling Realtors that they are dispirited by the stiff competition for the short number of listings they can afford."

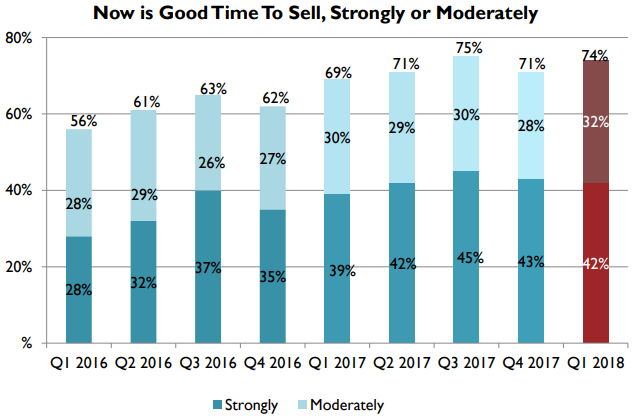

Responses to a similar question about selling a home rose from 71 percent in the previous survey to 74 percent with the increase coming from those who held moderate convictions. Age had little influence - every age group but one, the 55 to 64 group at 80 percent, had 72 percent positive responses. The "yes" response pulled a minimum of 70 percent positive responses across all regions, but was highest, 77 percent, in the West which has also had the highest rate of home price appreciation.

Home prices have grown a cumulative 48 percent since 2011 and are up 5.9 percent through the first two months of this year," said Yun. "Supply conditions would improve measurably, and ultimately lead to more sales, if a growing number of homeowners finally decide that this spring is the time to list their home for sale."

Sixty-three percent believe that prices have gone up within their communities in the last 12 months, which is consistent with Q4 2017 and an increase from 50 percent in Q1 2016. Thirty-one percent believe prices have stayed the same and six percent believe prices have gone down.

Forty-two percent of consumers believe that prices in their local area will stay the same over the next six months while 53 percent expect further increases. Only 6 percent think prices will decline. Those who are in the West, live in urban areas, or are renters are most likely to expect price increases.

Among those who currently do not own a home, about a third believe they would have a great deal of difficulty qualifying for a mortgage, up from 27 percent in the first quarter of 2017, and another 30 percent think it would be somewhat difficult. Among those with less than $50,000 in household income 76 percent said they would have at least some difficulty.

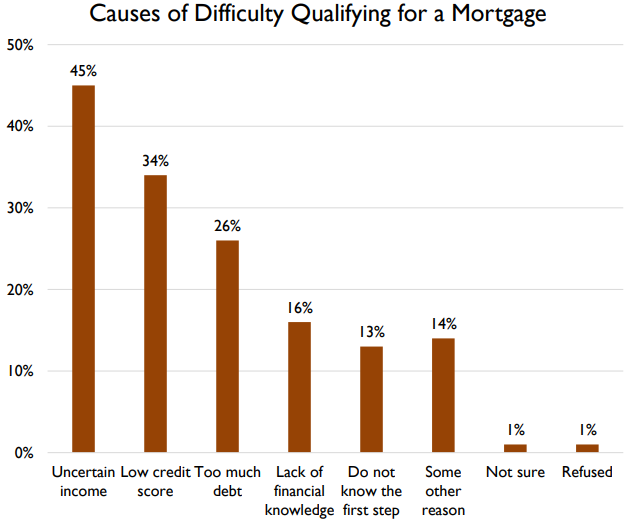

At 45 percent, uncertain income was the most frequent reason cited for a perceived difficulty in qualifying. Credit problems were second at 34 percent.

When asked what factors were preventing them from saving for a downpayment, 47 percent of non-homeowners cited limited income, 30 percent said student loan debt, 28 percent rising rents, and 19 percent said health and medical expenses.

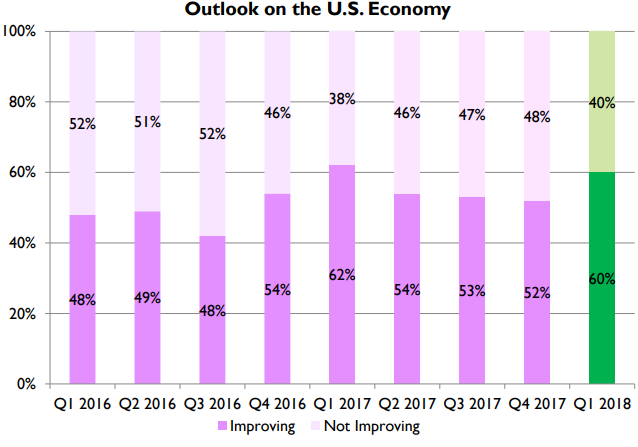

Sixty percent of people believe the U.S. economy is improving, up from 52 percent the fourth quarter of last year. Those living in rural areas, in the South, or with the highest incomes were the most positive as were those 55 to 64 years of age.

NAR said stronger economic confidence has led to households having improved feelings about their financial situation. The HOME survey's monthly Personal Financial Outlook Index showing respondents' confidence that their financial situation will be better in six months, rose from 59.1 in December to 62.0 in March. A year ago, the index was slightly higher (62.6).

"The jump in optimism to start the year can be attributed to the robust job creation in most of the country, as well as the larger paychecks households are enjoying because of faster wage growth and the recent tax cuts," said Yun. "These three positives should further ignite buyer demand. However, several metro areas with the healthiest labor markets also have the most severe supply and affordability pressures. This troublesome reality is what's dampening moods and keeping many would-be buyers at bay."

The HOME survey was conducted from January through early March with a sample of households selected via random digit dialing. Approximately 900 qualified households responded in each month, for a total of 2,701 households in the first quarter.