Servicers might have a loyalty problem. Or, more likely, a marketing one.

In its April Mortgage Monitor, much of which we covered earlier this week, Black Knight Financial Services took an in-depth look at servicer retention. This is the rate at which a borrower would remain with the same servicer after refinancing. The company found that servicers are more and more losing customers post-refinance. Of course, picking a servicer is not something a borrower does directly, the servicer comes as a package when a borrower decides on a lender for the refinance.

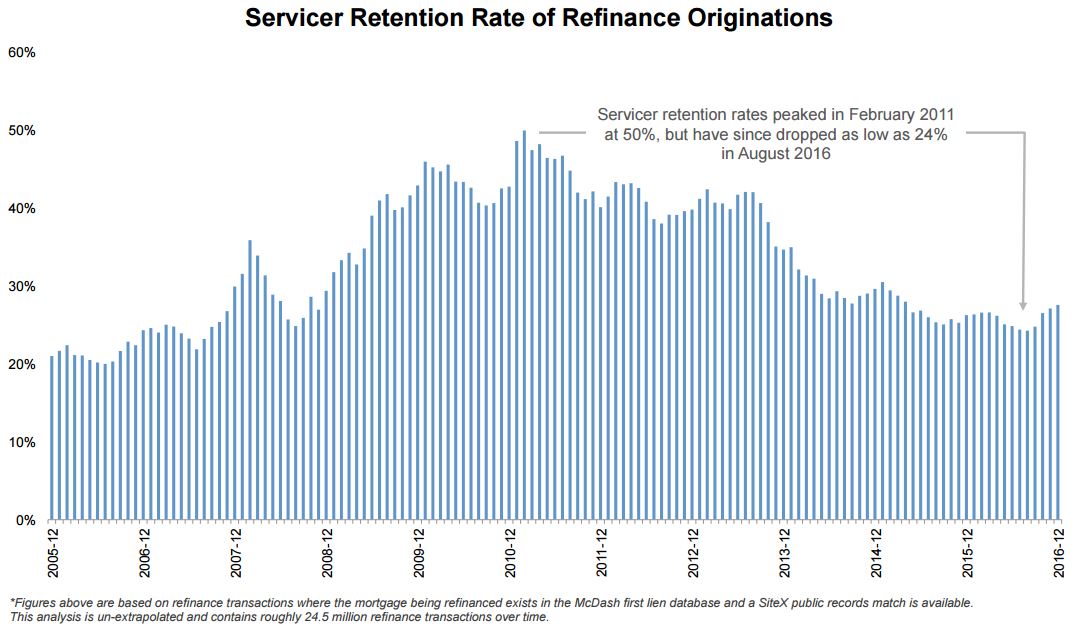

In 2011 about half of refinancing borrowers returned to the same servicer with the new loan. By August 2016 the number had dropped in half, to 24 percent, a nine-year low. The number did tick up slightly in the next quarter as high credit score refinancing was revived by low interest rates. Servicers have a highly uneven retention rate, with the top third of them retaining twice the percentage of their loans as the bottom 33 percent.

The company says the decline is due, in large measure, to increased competition among both lenders and servicers. Large banks had a 50 percent share of mortgage lending in 2011 and 60 percent of the servicing rights. Today those shares have slipped to 50 percent and 27 percent respectively.

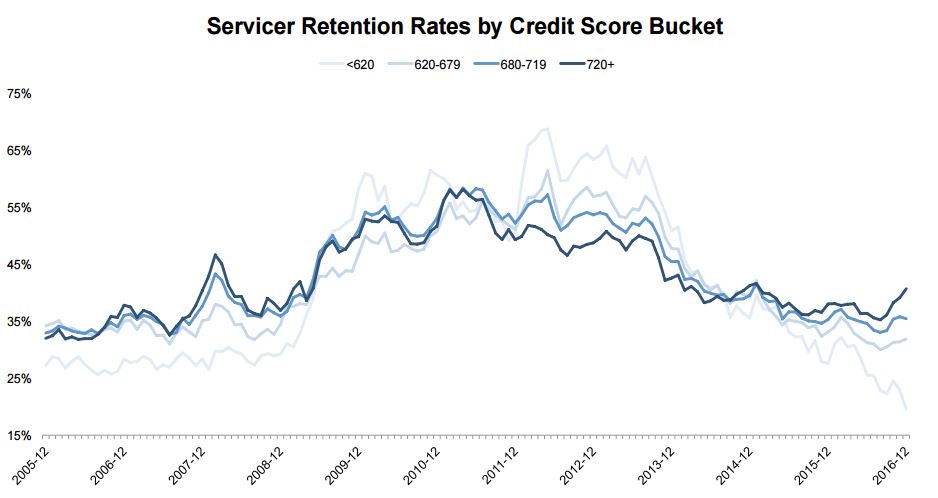

During the housing crisis, retaining customers was less of an issue for servicers. Lower credit score borrowers had limited refinance options and those that did refinance were often aided by HARP originations. Since 2014 however retention rates have dropped within the lower credit score buckets, especially the very low score borrowers while rates have risen for the highest band of credit scores, those above 720.

Around this same time there was an upward shift in the retention of high unpaid balance loans, especially those over $400,000. While lower balance loans drifted along in the low- to mid-20 percent retention rate range, the higher balance loans peaked near 40 percent in 2015.

Servicers also seem to have more success in retaining low loan-to-value (LTV) ratio loans as well. Over the past six months, loans with LTVs under 80 percent have roughly twice the retention rate of those with ratios of 91 percent or higher.

As with any business, keeping existing customers is more cost-effective than recruiting new ones and, in the case of servicing, this becomes even more important as the refinancing share of the market recedes. Black Knight points out that new originations could have more longevity as rates rise.

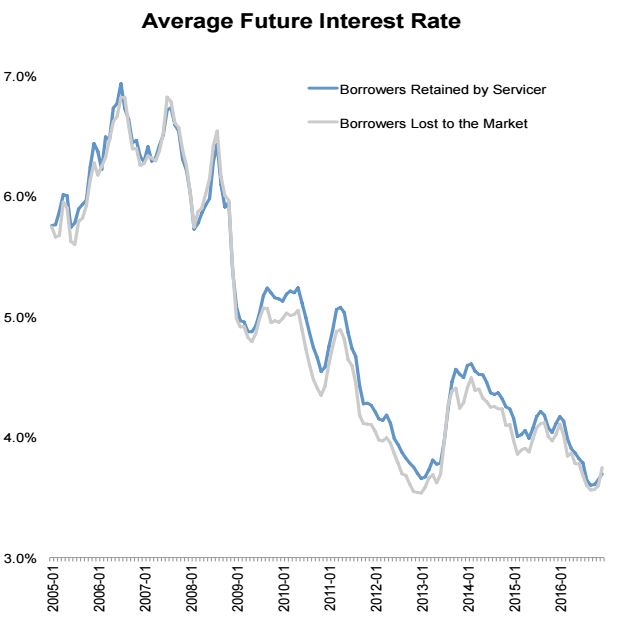

The Mortgage Monitor data indicates that the interest rates offered to refinancing borrowers, at least in some market segments, seem to be a factor in retention. The company did a simple comparison of the interest rate received by borrowers who stayed with the same servicer within one market segment versus those who went elsewhere.

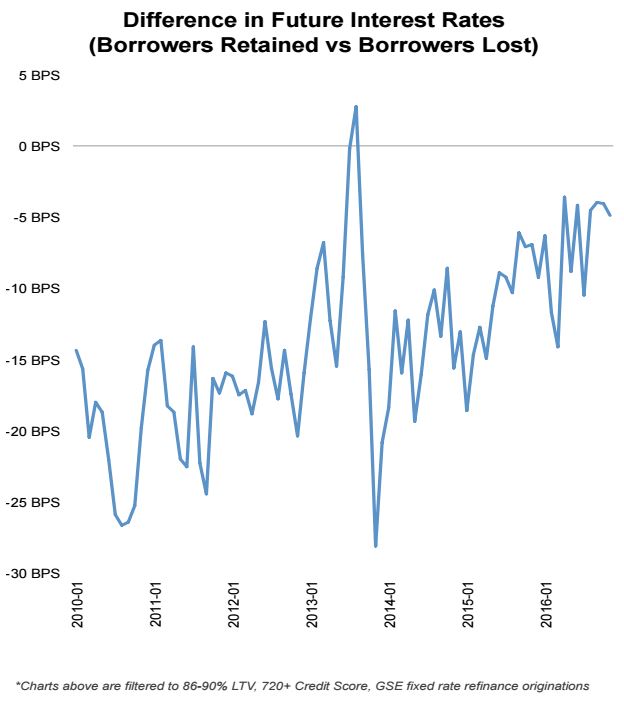

The chart below shows the delta in rates between those two universes. At the bottom of the market those who left the servicer received a rate 20 to 25 basis points lower than those who stayed. Today that difference is as little as 5 basis points. This, the analysis states, illustrates the critical importance of accurate risk-based pricing "as lenders may be able to retain customers with even marginal reductions in interest rate offerings."

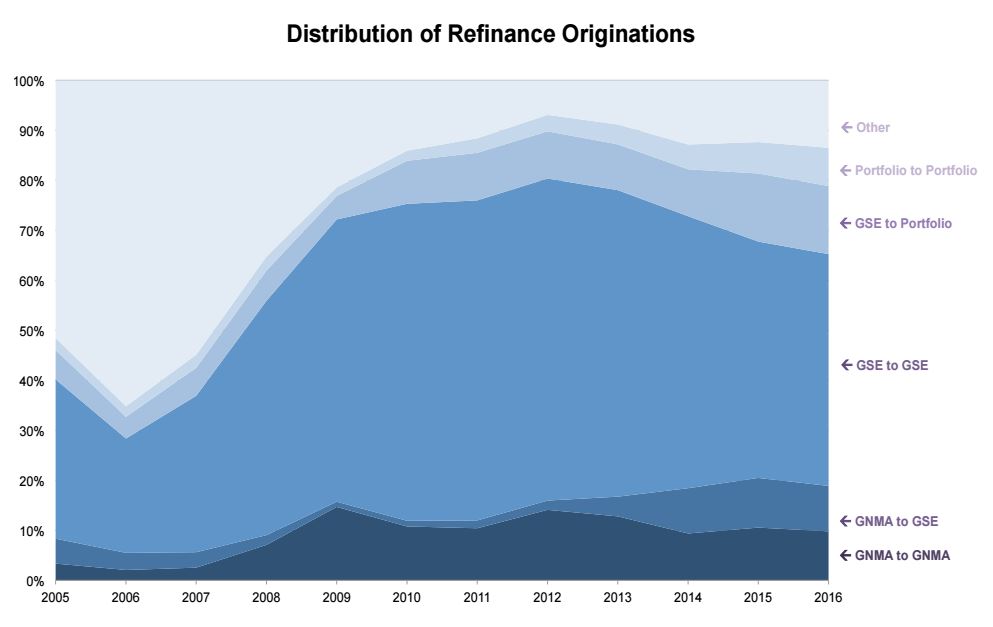

The Mortgage Monitor also looked at where refinancing moves borrowers from one type of loan to another, resulting in a servicer change. Current refinancing among Fannie Mae and Freddie Mac (the GSEs) borrowers are declining as a share of the refinancing universe. A lower share of GNMA loan borrowers are transitioning into a new GNMA loan while an increasing share are moving to GSE or Portfolio loans, probably to eliminate FHA mortgage insurance premiums which now endure for the life of the loan.

Refinancing from one portfolio to another was also up 2016, due partly to low rates and partly to jumbo refinancing. The "Other" category on the chart was driven from 2005 to 2007 primarily by PLS activity. There is now an increase in borrowers refinancing out of PLS, probably as they rebuild both equity and their credit.