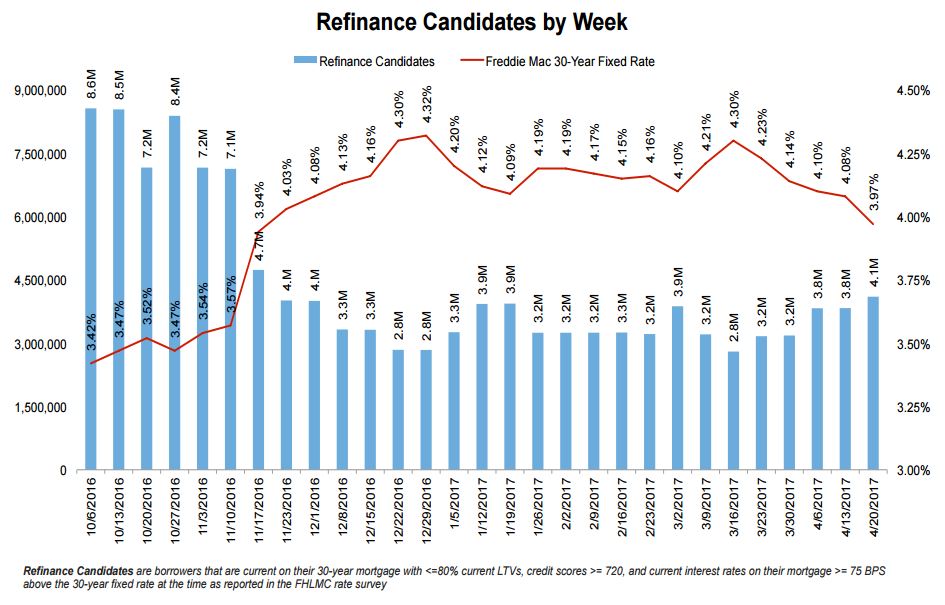

It wouldn't be surprising to find both lenders and consumers suffering from whiplash following the first quarter of 2017. Mortgage rates, which shifted by as much as 30 basis points in either direction during the quarter, took the refinanceable population along for the ride. That population is defined by Black Knight Financial Services in its Mortgage Monitor as homeowners who can both qualify for refinancing and have the motivation to it.

In any given week during the quarter, Black Knight says, "relatively small interest rate movements have increased or decreased the size of the refinanceable population by as much as 20 percent." For example, the 30-year fixed rate mortgage dropped below 4.0 percent on April 20 and that increased the refinance pool to 4.1 million, up 46 percent from the 2.8 million borrowers in the pool in mid-March. Still, that pool was half of its size last October when rates were under 3.5 percent.

Black Knight says continued fluctuations such as those in Q1 will continue to stoke volatility in refinance originations and in prepayment activity.

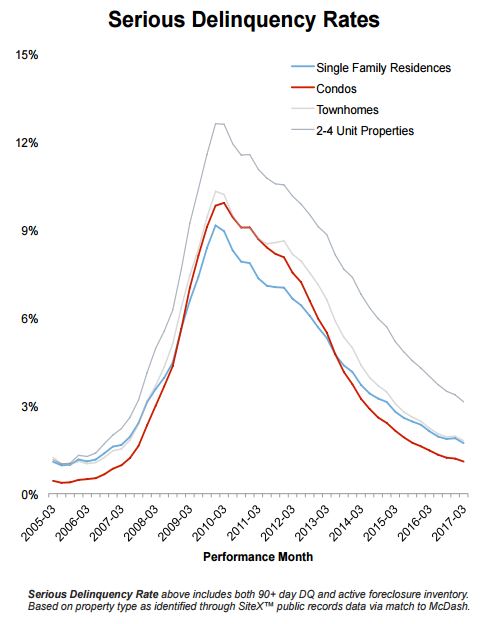

The Monitor took an in-depth look at loan performance by property type, single family, condominiums, townhouses, and two-to-four unit residences. Condominiums were the hardest hit by the 2008 market downturn, but have seen a stronger recovery than single family residences (SFR), with delinquencies falling at a faster pace in every quarter since Q4 of 2011.

Today the rate of serious delinquencies (i.e. more than 90 days past due) among condo loans is 36 percent below that of single-family loans while delinquency rates overall are 44 percent lower. Black Knight points out this is not new. At this same point in 2006, condos had a serious delinquency rate 55 percent lower than that of SFR.

The same distinction exists geographically. Serious delinquencies rates are lower for condos than SFR in all 50 states and in all but three (Sacramento, Las Vegas, and Orlando) of the top 50 metro areas.

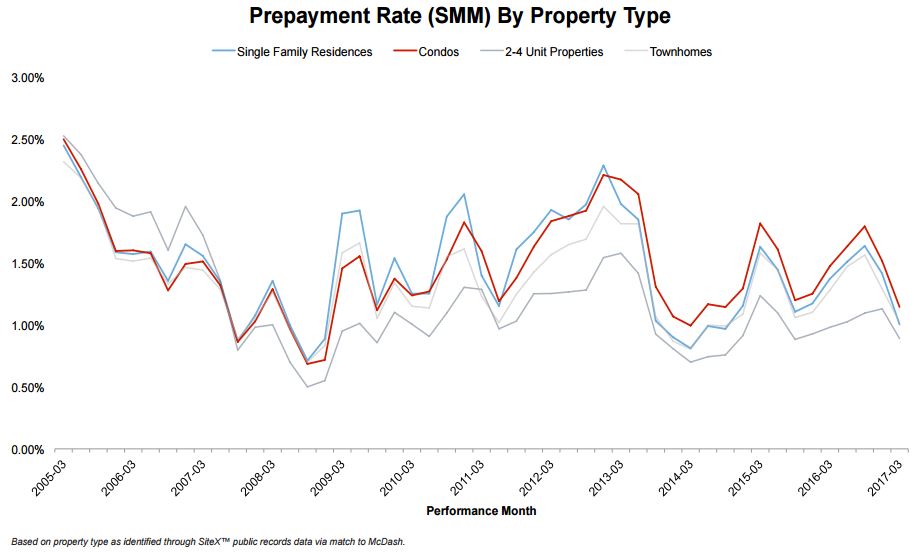

Single Month Mortality (SMM) rates, or prepayments have demonstrated a similar pattern since the beginning of the financial crisis. From 2005 to 2008 there was little difference in prepayment speeds among SFRs, condos and townhouses, but from 2008 to 2010, as interest rates declined and refinancing began to boom, SFR refis began to outpace condos. That shifted again and since early 2013 condo SMM has outstripped that of SFRs by at least 10 percent. Black Knight says this divide becomes more pronounced as interest rates rise. When rates went up in late 2013 and early 2014 the speed of prepayments on condos was 18 to 27 percent faster than for SFRs.

However, refinancing isn't the only thing driving the differences in prepayment speeds. Housing turnover has historically been a bigger component of condo prepayments than of the SFR rate. The differential fell to as little as 28 percent more for condos than SFRs during the housing crisis but, on average, over the last ten years the turnover-driven rate has been 50 percent higher. The difference was down to 42 percent in the fourth quarter of 2016, but as rates increase and refinancing ebbs, turnover will gain a greater importance in SMM and the gap between condos and SFR prepayment speeds will probably widen again.

Another driver of SMM is market distress and during the financial crisis the condo market suffered a higher rate of delinquencies and foreclosures than the single-family market and thus a higher rate of distress driven SMM.

A fourth driver is curtailments - additional payments on principal to shorten amortization. These have begun outpacing defaults as the third most prevalent driver of SMM for both condos and SFR. Curtailments on condos has consistently been 10 to 20 percent higher than for SFRs over the last ten years.

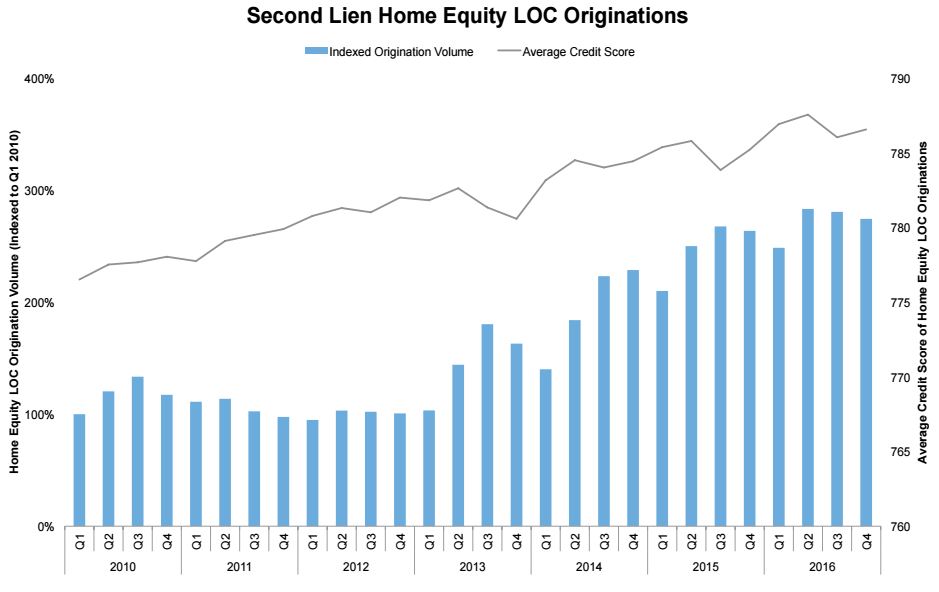

Finally, Black Knight looks again at home equity lines of credit (HELOCs) and their popularity. HELOC originations were up 10 percent in 2016 to hit an eight-year high although they slowed during the last two quarters of the year as interest rates declined and borrowers shifted back to first lien refinances. Even though homeowners are sitting on equity that is only 5 percent lower than in 2006-2007, equity lending is well below what it was then.

The average HELOC originated in the 4th quarter of 2016 had an approved line over $120,000, only slightly below the all-time high set in Q1, but utilization rates remain low. Borrowers were drawing only about one-third of their available line of credit at origination, less than half of what was seen in HELOCs originated in 2005 and 2006. Black Knight says that both the low utilization rates and the extremely high credit scores (an average of 787), indicate both borrowers and lenders are exercising significant restraint with these loans.

When it comes to older vintages of HELOCS, 2017 will set a record for the percentage of active loans (19 percent) that will reset, although the number of borrowers, about 1.5 million, facing reset is down by 100,000 from 2016. The loans represent just under $100 billion in outstanding unpaid principal balances, with an average of $62,500 per loan.

The loans resetting this year and next represent the last of the bubble-era vintages that have been worrying the industry for several years. A loan that resets means an increase, and sometimes a large one, in the monthly payment borrowers must meet. On average, payments on loans resetting this year will increase about $250 per month, doubling their previous payments.

Black Knight Executive Vice President Ben Graboske said, "One thing that's working in the 2007 vintage HELOCs' favor has been the equity and interest rate environment of the last year. Rising home prices and low interest rates throughout 2016 have allowed borrowers to be much more proactive than in years past in terms of paying off or refinancing their lines to avoid increased monthly payments. For those still facing resets, however, equity continues to be a struggle. One-third of borrowers whose HELOCs will reset in 2017 have less than 20 percent equity in their home, making refinancing problematic. One in five have less than 10 percent, and one in 10 are actually underwater. Even that reflects improvement in home prices, though; last year 45 percent of borrowers facing reset had less than 20 percent equity and nearly 20 percent were underwater."

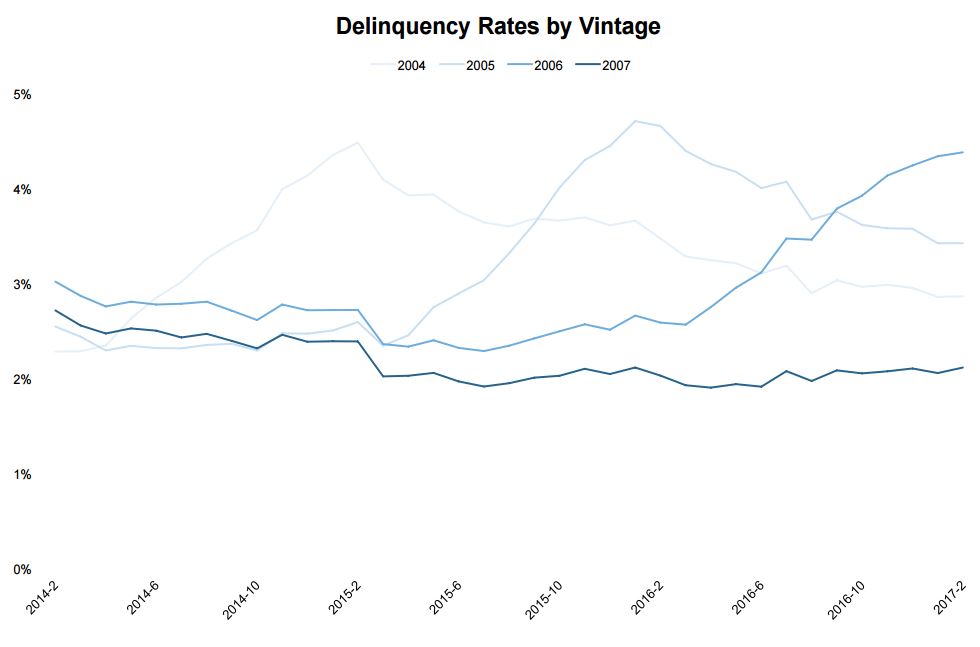

Delinquency rates of the 2006 vintage that reset last year surged by 74 percent. This was marginally better than the 2004 to 2005 vintages which saw delinquency rates rise by 90 and 88 percent respectively.

After the 2018 resets there will be a lull of several years before those loans originated during the current resurgence of HELOC originations reach the reset point. That will begin in 2023.