"Gig," a term that used to refer mostly to a musician's booking, is now being used to describe a whole sector of the U.S. economy. Fannie Mae defines it, rather narrowly we think, as the on-line, on-demand services such as ride sharing and accommodation, and included questions about it in their Third Quarter National Housing Survey. Fannie Mae says its purpose was to understand the extent to which the gig economy is growing and how it might affect attitudes towards homeownership.

The survey found that 16 percent of American adults have provided a service through the gig economy. Seven percent report providing ride sharing and the same percentage have provided "services," most commonly child sitting or handy-man services. Five percent have provided accommodation sharing (i.e. AirBnB type hosting), 4 percent food delivery, and 2 percent car sharing. As those figures indicate, 34 percent of gig workers reported they have performed more than one type of service.

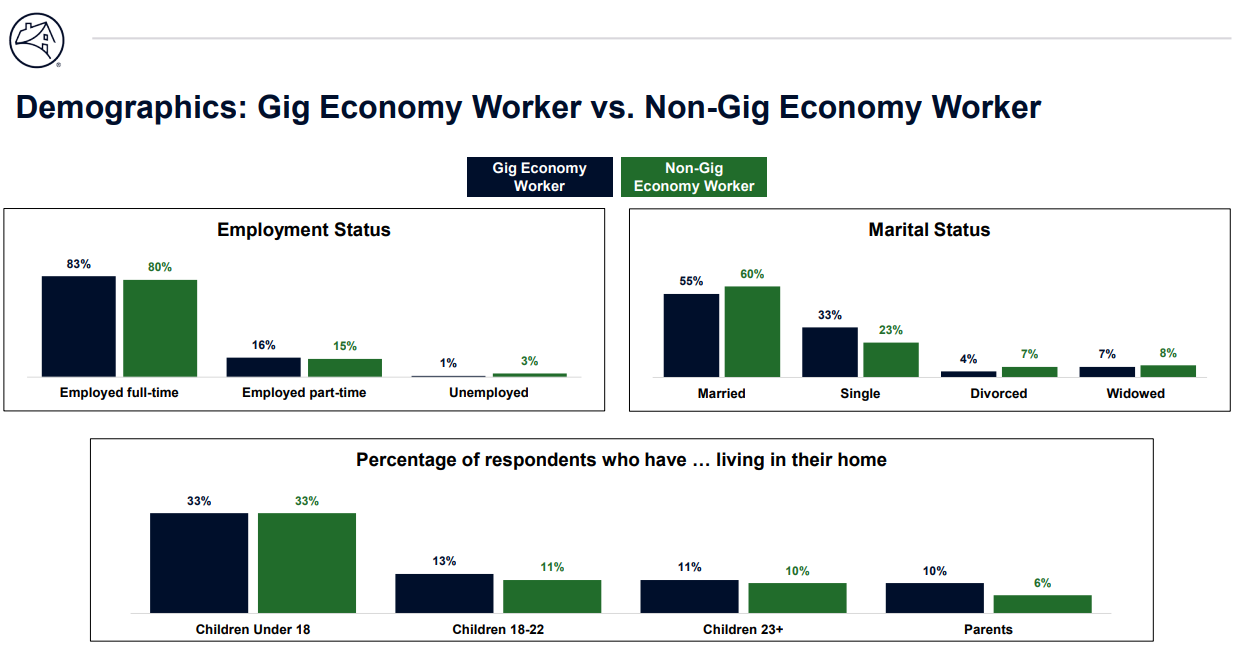

Millennials, persons aged 18 to 34, make up the largest group (44 percent) 0f those working in the gig economy and are also the most likely to report providing more than one service. The 45 to 64 age group was the second largest at 28 percent while those just younger and just older made up 18 percent and 16 percent respectively.

Just over half of workers in this new sector report making more than $50,000 per year and 83 percent are employed full time. For most, the gig is a sideline; 62 percent report it provides less than 20 percent of their income, while only 2 percent say it contributes more than 80 percent.

Fannie Mae says gig workers tend to have a more positive view of their financial condition, both present and future, than other respondents. Thirty-four percent report having higher household income than 12 months earlier compared to 25 percent of others and 56 percent anticipate an improved situation one year from now, 10 percentage points more than non-gig workers.

The survey found little difference between gig and non-gig workers who currently rent, as 40 percent of them do, in their attitudes toward homeownership and renting. Slightly more than two-thirds of both groups agreed with the statement that homeownership makes financial sense "because you're protected against rent increases and owning is a good investment over the long term." The remainder agreed that, "Renting makes more sense because it protects you against house price declines and is actually a better deal than owning." There was less agreement regarding homeownership as a lifestyle choice. Only 54 percent of gig workers agreed that owning makes more sense because you have more control over where you live and a better sense of privacy and security" compared to 60 percent of others.

Gig workers are also less likely than other renters to think it is a good time to purchase a home (40 percent vs 49 percent) and were 19 percentage points more likely to say they will rent when they next move. Fannie Mae says however that 75 percent of the 69 percent that will remain renters do plan on homeownership at some point.

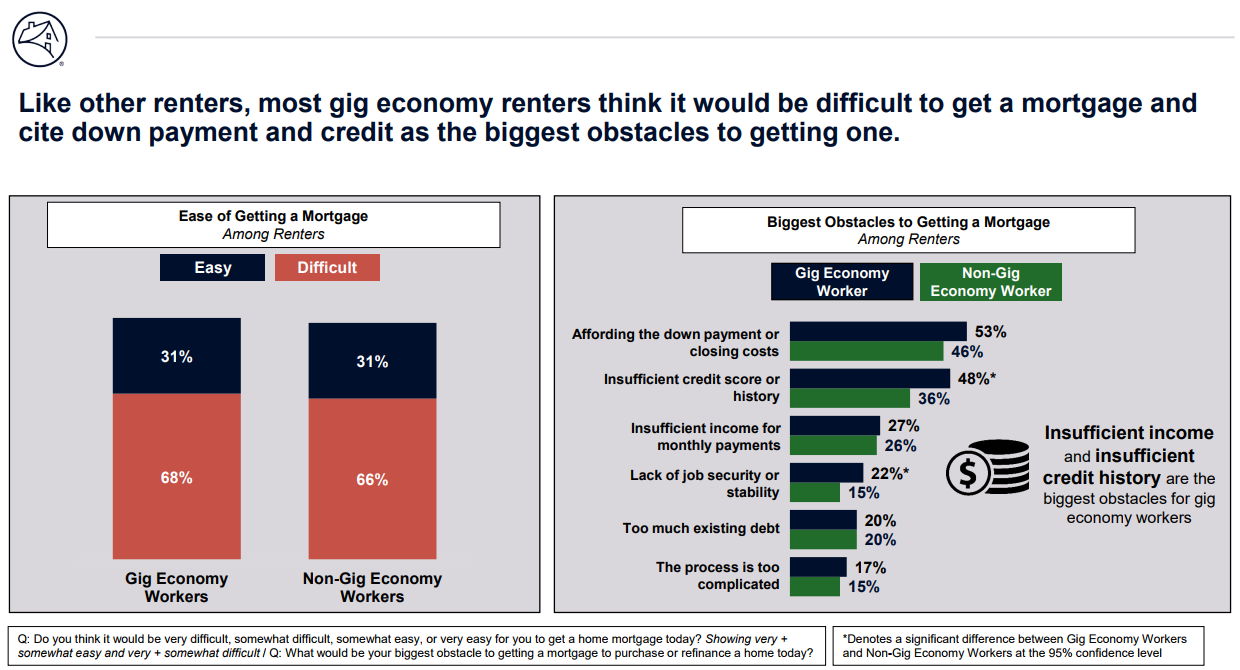

The two groups of renters differed only slightly in their opinion about how difficult it might be for them to get a mortgage (over two-thirds thought not), but gig workers did cite more concern than others about some of the barriers they might confront. Higher percentages cited perceived problems because of an insufficient downpayment, credit score, or job history/stability than the rest. Their concerns about debt levels, income, and the complexity of the process didn't differ much between the two groups.

Based on the responses, Fannie Mae concludes that "One area for further research is to determine to what extent current underwriting standards sufficiently account for the potential of gig economy income to supplement other full-time income sources. And the salience of this research question will grow if gig economy participation continues to grow."