As banks and government tried to stem the flow of foreclosures during the housing crisis there was a lot of debate (and criticism) about what needed to be done and how to do it. The acting director of the Federal Housing Finance Agency, Edward DeMarco fought tooth and nail to prevent Fannie Mae and Freddie Mac (the GSEs) from being forced to reduce the principal balances of their loans. Barrels of ink were consumed criticizing the Home Affordable Modification Program (HAMP). Servicers were penalized for their misfeasance running it. Servicers set up several proprietary programs to modify loans held in mortgage-backed securities and bank portfolios. In addition, there was much criticism of homeowners who, it was alleged in some quarters, were quick to walk away from mortgages they never should have been given in the first place.

In the end, more than nine million homes were foreclosed.

The JPMorgan Chase Institute has now published a report trying to determine what did work during that period, looking specifically at the relative effectiveness of reductions in monthly mortgage payments and long-term mortgage debt on default and consumption. It studied 450,000 borrowers who had received a modification from either HAMP, the GSEs, or a Chase proprietary program between July 2009 and June 2015. A subset of this sample also had other financial affiliations with Chase (credit card, checking account) which allowed an analysis between mortgage modifications, default, credit card spending, and income.

The study revealed the following.

Borrowers who had similar pre-modification mortgage payment to income (PTI) ratios received considerably different payment reductions depending on the type of modification they received. Those with PTIs above 50 percent got more than twice the payment reduction from HAMP than they got from the GSE program - 55 versus 27 percent. However, for those with low PTI ratios the reverse occurred. They got a 25 percent reduction from the GSEs compared to 8 percent from HAMP.

A 10 percent reduction in the monthly payment reduced defaults by 22 percent.

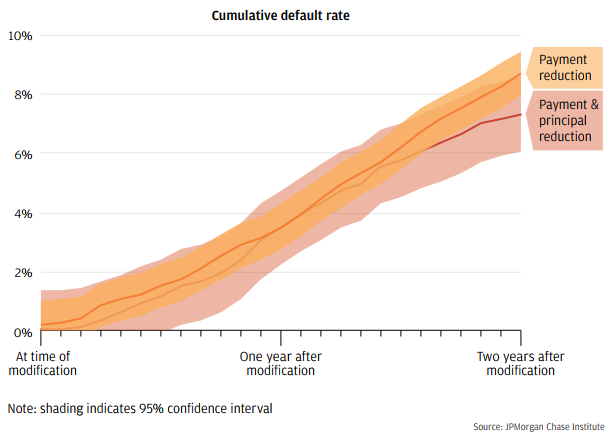

Principal reduction, while expensive, didn't have much impact. The study looked at 2,000 borrowers who received a payment reduction that included a write-off of mortgage balance averaging $112,000 or 32% and 7,000 borrowers who got a reduction in payment through an extended term and/or a lower interest rate but no principal reduction. They was very little difference in the default rate two years later. The institute says this suggests that "strategic default" was not a primary factor in the decisions regarding default. Homeowners were not defaulting simply because they owed I more on their mortgages than the market value of their property.

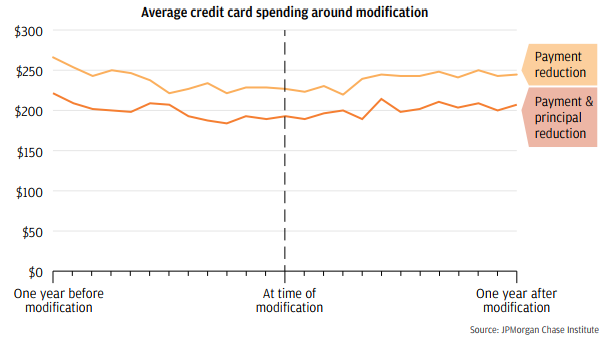

Payment reduction also didn't help boost the economy. There was also no difference in consumption, i.e. credit card spending, between those who received only payment reduction and those who got both types of modification relative to their spending a year before the modification.

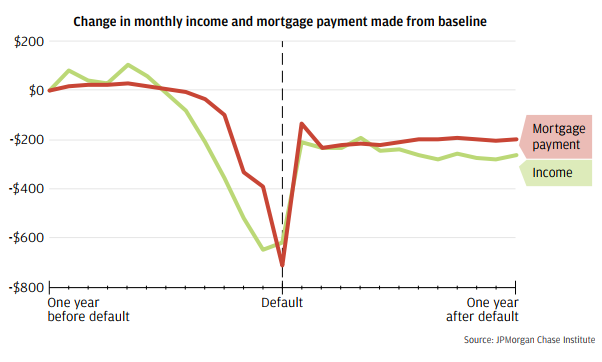

The final finding was a strong correlation between significant income loss and the ultimate default of the borrower. This held true regardless of the PTI or the loan-to-value (LTV) ratio before the modification. This, the report says, mitigates against a high payment burden or negative equity driving the default.

The report draws some conclusions from its findings. First that modification programs designed to achieve substantial payment reductions will be more effective at cutting defaults. "Modification programs designed to reach affordability targets based on debt-to-income measures without regard to payment reduction will be less effective," as will principal-focused debt reduction that targets a specific LTV but leaves the borrower underwater.

If modifications can be considered a re-origination, the study's results may have relevance to underwriting. The correlation of default with income loss suggests that affordability measures such as debt-to-income, while important, probably shouldn't drive underwriting to the extent they do. Policies that help borrowers establish and maintain a suitable cash buffer against income shock or unexpected expenses could be an effective barrier to default.

There should also be greater consideration about options that fall between keeping homeowners in their homes and foreclosure. These would include deeds-in-lieu and short sales which were utilized during the housing crisis, but not in large numbers.

The lack of consumption response to principal reduction on the part of underwater homeowners suggests their marginal propensity to consume out of housing wealth is zero. This inability to translate home equity into liquid resources may constrain the housing wealth effect as a mechanism to transmit changes in monetary policy to household consumption.