The use of Automated Valuation Models (AVM) is expected to expand following the announced plans of the Fannie Mae and Freddie Mac to waive the requirement for a professional appraisal on qualified purchase loans where the loan-to-value (LTV) ratio is at or below 80 percent. Fannie Mae had previously allowed this waiver only for refinancing, while Freddie will now allow automated evaluation tools for both purchase and refinancing loans when working with its Loan Advisor Suite.

CoreLogic's Principal Economists Yanling Mayer, writing in the company's Insights Blog, says these changes come as the industry is hearing of shortages of certified and licensed appraisers, especially in rural areas. But there is still controversy. The Appraisal Institute has raised safety and soundness concerns over eliminating the appraisal requirement and is seeking a legislative rollback and federal banking regulations for real estate transactions generally treat automated appraisal methods as a due diligence tool rather than as the primary valuation.

Mayer says, from the perspective of economics, a clash between proponents of the two methods seems inevitable, "as advanced analytics and big data technology have expanded collateral evaluation capabilities. These alternatives today are often powered by large databases that can capture information on a given property as well as transaction records in and around the property in consideration.

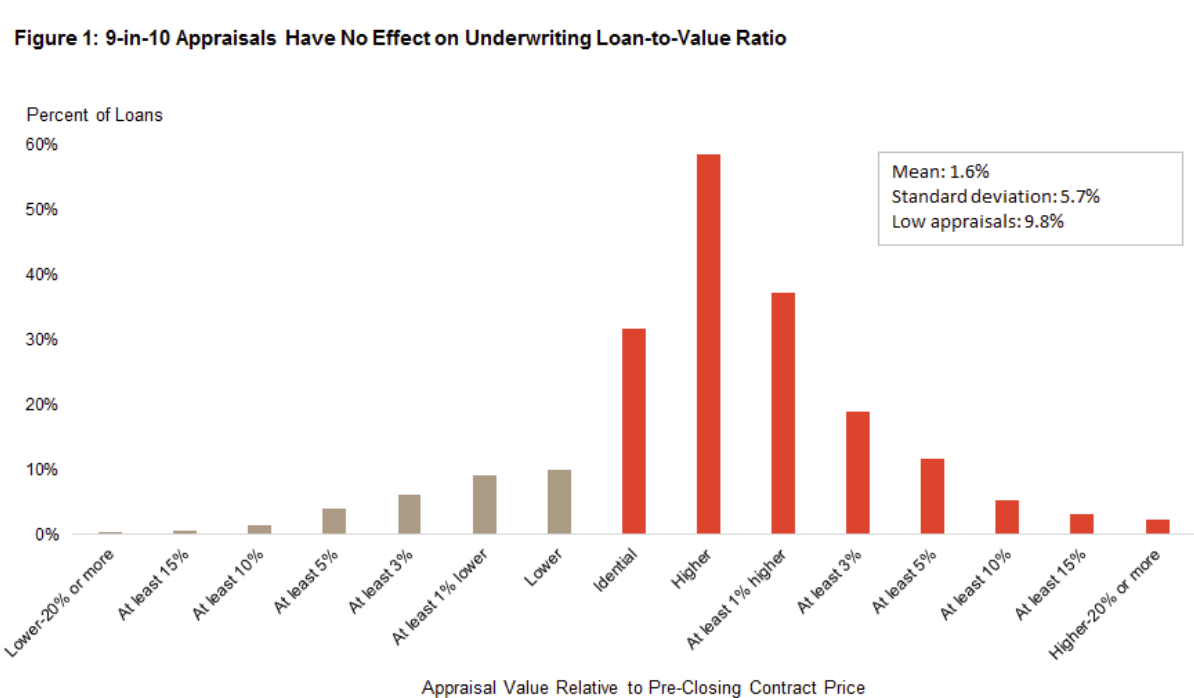

While not attempting any conclusions about the accuracy of the valuations, CoreLogic looked at the impact of automated evaluation on the LTV ratios of purchase loans. These ratios are determined by the lower of contract purchase price or the appraised value.

Traditional appraisals rarely come in below the contracted price, she puts the incidence at about 10 percent of loan applications and a Fannie Mae study put it at less than 4 percent of funded loans. Consequently, LTV is typically unaffected by the appraisal.

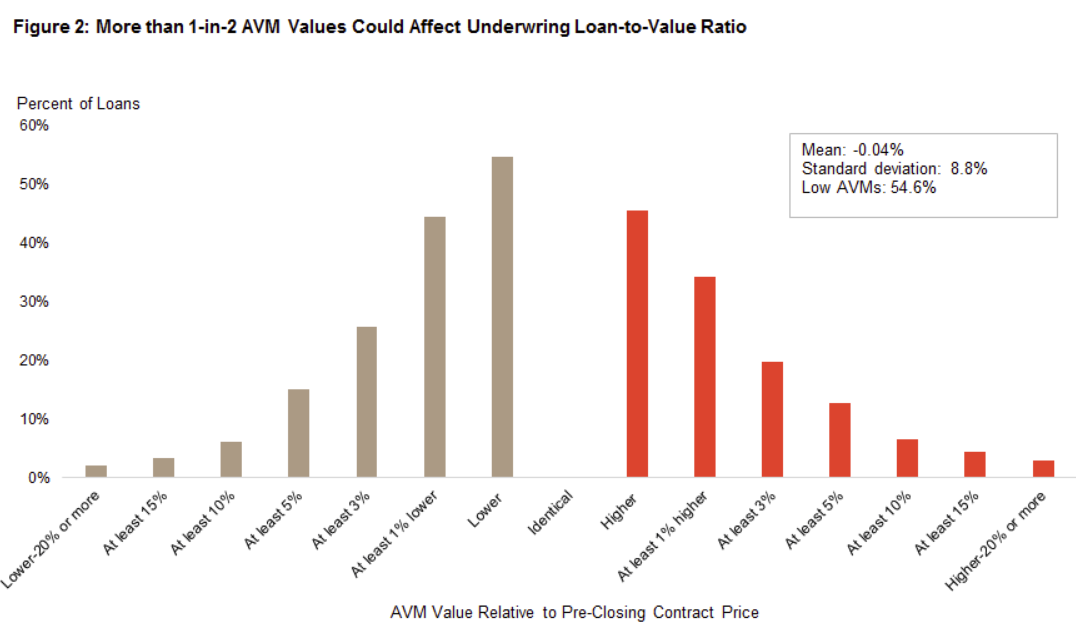

Quite the opposite is the case with AVMs. CoreLogic analyzed a 190,000-unit sample of single family homes financed between July 2016 and June 2017 with a traditional appraisal but for which a CoreLogic AVM value was also available. The date of the AVM was not identical to that of the appraisal, but did not vary by more than 3.5 months.

Figure 1 shows 31.6 percent of the appraisal values were exactly at the contract price while 58.6 percent were slightly higher. This left only 10 percent of the properties appraised below the proposed purchase price. Thus, for the majority of the homes, the purchase price effectively determined the origination LTV.

In Figure 2, the AVM values are also shown relative to the purchase price. Those values were lower in 54.6 percent of the cases and higher only 45.4 percent of the time. The AVM were more symmetrically distributed around the purchase price, but with "thicker tails" (larger percentages as outliers from the contract price, especially on the low end), and thus greater uncertainty in the valuation. For the five out of nine properties with an AVM value below the purchase price, the LTV ratios for these loans would be higher had the AVM valuations been used instead of a traditional appraisal.

Mayer concludes that since an AVM has odds of 55 to 45 of coming in lower than the purchase price, while the odds of this happening for a traditional appraisal is 10 to 90. Therefore, increased AVM usage will increase the underwriting LTV on a greater number of loans. The "fatter tail" of the distribution below the contract price also means that upward adjustment will more often be larger than for a traditional appraisal.

May says that while the debate will probably go on about the relative accuracy of the two valuation methods as well as their usefulness in predicting default risk and loan performance, everyone has to agree that reliable information is needed about collateral risk in both loans and portfolios in order to make informed underwriting and investment decisions.