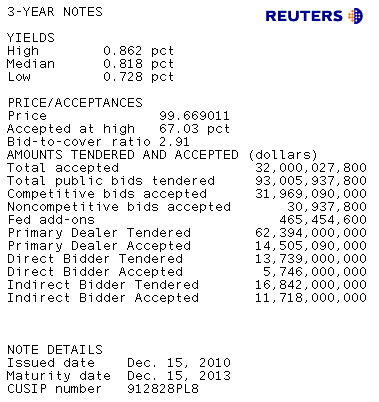

Treasury just sold $32 billion 3-year notes.

The bid to cover ratio, a measure of auction demand, was 2.91 bids submitted for every 1 accepted by Treasury. This is the weakest btc ratio in the last eleven 3-year note auctions. 67.03% of the competitive was bid was allotted at the high yield of 0.862%. This is slightly above the 1pm "when issued yield" which is basically the market's forward pricing mechanism for TSY debt issuance and is another indication that bargain buying sentiments were not strong.

Dealers were awarded 45.4% of the competitive bid. This is below their five auction average and worse than their participation in the previous two 3-year note auctions (51.1% and 59.1%). In terms of taking down what they bid on, the street was awarded 23.3% or $14.5 of the $62.4 billion they bid on. That is the second highest hit rate for dealers in the last nineteen auctions.

Direct bidders (bond funds like PIMCO and Vanguard) added $13.7 in new inventory or 17.9% of the competitive bid. This is an above average award. Like dealers, directs saw a greater percentage of their bids accepted than usual with an above average 17.9% hit rate on the supply they bid on.

Indirects, often seen as a gauge of overseas central bank demand, took home 36.7% of the competitive bid or $16.8 billion in new 3-year note inventory. Like dealers and directs, saw a greater percentage of their bids accepted than usual with an above average 68.7% hit rate.

Plain and Simple: The auction wasn't all that bad. Buyers were willing to bid but not aggressively. High hit rates combined with a weak btc ratio and modest tail vs. the 1pm WI (even after concessions) are indicative of stop outs being hit aka the market set a level where they would bid and made Treasury come to it. You could say the market was well-offered and bidders were in no rush to buy, which forced asking prices lower and yields higher. On the bright side, indirect participation did not decline noticeably, which soothes concerns that overseas accounts are shunning U.S. TSY debt. Yes they are selling but not totally liquidating, not yet at least.

Market Reaction...

The pain trade is getting more and more painful. 10s are up to 3.13% and mortgages seem to be one of the sources of excessive weakness in the bond market. Duration shedding is obvious as "rate sheet influential" MBS prices are over 1 point in the red and yield spreads are widening. Lower and wider = liquidation. Reprices for the worse are possible. MG will post more charts shortly.